Strategi Trading AlphaTradingBot

Ikhtisar

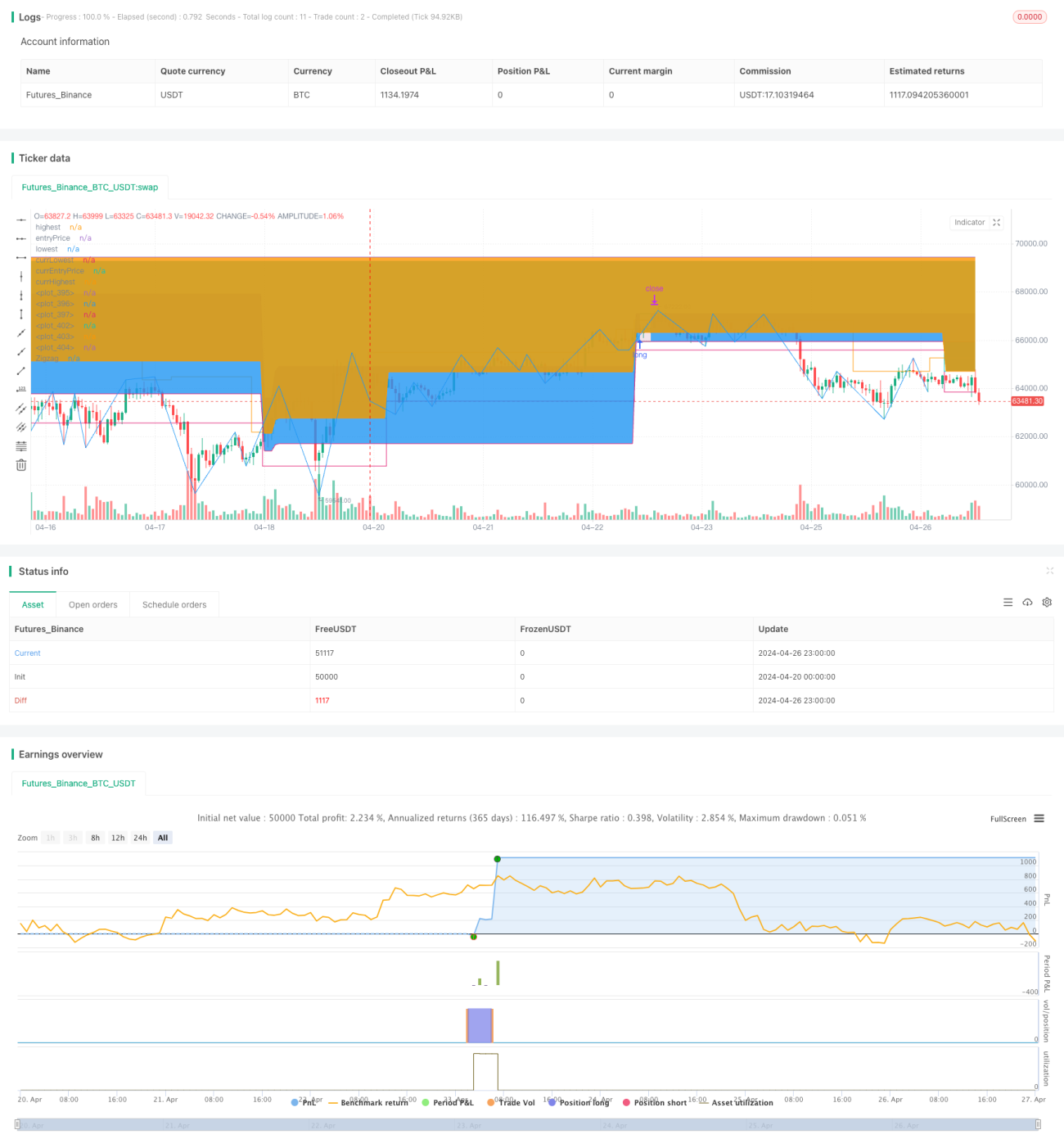

AlphaTradingBot adalah strategi trading intraday berdasarkan indikator Zigzag dan deret Fibonacci. Strategi ini mengidentifikasi tren dengan mengenali titik tertinggi (HH) dan titik terendah (LL) pasar, dan menggabungkan retracement Fibonacci serta ekspansi untuk menetapkan titik masuk, take profit, dan stop loss. Strategi ini hanya berjalan dalam rentang tanggal yang ditentukan, dapat melakukan long dan short secara terpisah, dan memiliki kemampuan penangkapan tren serta pengelolaan rasio risiko-imbalan yang baik.

Prinsip Strategi

- Mengidentifikasi titik tertinggi (HH), titik terendah (LL), higher low (HL), dan lower high (LH) pasar menggunakan indikator Zigzag.

- Ketika HH muncul, dianggap sebagai awal tren naik, mulai mencari peluang long; ketika LL muncul, dianggap sebagai awal tren turun, mulai mencari peluang short.

- Dalam tren naik, jika muncul HL, maka interval antara HL dan LL sebelumnya digunakan sebagai zona retracement Fibonacci untuk posisi long. Jika harga menembus high sebelumnya, maka buka posisi long di area retracement antara 23,6% - 38,2% (dapat disetel), stop loss ditempatkan pada retracement 61,8%, dan take profit dihitung berdasarkan nilai RR (dapat disetel).

- Dalam tren turun, jika muncul LH, maka interval antara LH dan HH sebelumnya digunakan sebagai zona retracement Fibonacci untuk posisi short. Jika harga menembus low sebelumnya, maka buka posisi short di area retracement antara 61,8% - 76,4% (dapat disetel), stop loss ditempatkan pada retracement 38,2%, dan take profit dihitung berdasarkan nilai RR (dapat disetel).

- Manajemen order: Hanya satu posisi dibuka per sinyal, hingga posisi tersebut ditutup. Jika kerugian per perdagangan mencapai X% (dapat disetel) dari total akun, strategi akan berhenti berjalan.

Analisis Keunggulan

- Kemampuan mengikuti tren yang kuat. Dengan mengidentifikasi tren secara efektif melalui Zigzag, dapat masuk pada awal tren.

- Logika retracement yang jelas. Menggunakan retracement Fibonacci untuk menetapkan zona masuk, masuk saat retracement tren, dengan tingkat kemenangan yang relatif tinggi.

- Risiko terkendali. Dengan menetapkan rasio kerugian maksimum per perdagangan untuk mengontrol risiko setiap transaksi, serta sistem stop loss yang ketat memastikan total risiko terkendali.

- Rasio risiko-imbalan dapat dioptimalkan. Dapat menyesuaikan nilai RR sesuai dengan karakteristik pasar dan preferensi pribadi untuk mengoptimalkan rasio risiko-imbalan strategi.

Analisis Risiko

- Trading yang sering. Karena sensitivitas Zigzag yang tinggi, sinyal dapat sering muncul, menyebabkan overtrading.

- Penangkapan tren yang tidak akurat. Tren yang dinilai oleh Zigzag mungkin masih menyimpang, menyebabkan waktu masuk yang kurang ideal.

- Kinerja buruk di pasar sideways. Di pasar yang bergejolak (sideways), strategi ini dapat menghasilkan banyak perdagangan yang merugi.

- Periode operasi terbatas. Strategi hanya berjalan dalam rentang tanggal yang ditentukan, mungkin kehilangan beberapa pergerakan pasar.

Arah Optimasi

- Memperkenalkan lebih banyak indikator teknis, seperti MA, MACD, dll., untuk meningkatkan akurasi penilaian tren.

- Mengoptimalkan manajemen posisi, misalnya menyesuaikan posisi secara dinamis berdasarkan indikator seperti ATR.

- Mengoptimalkan logika take profit dan stop loss, misalnya menyesuaikan level stop loss secara dinamis berdasarkan volatilitas pasar.

- Memperkenalkan indikator sentimen pasar, hindari masuk saat optimisme atau pesimisme yang ekstrem.

- Melonggarkan batasan tanggal, meningkatkan generalisabilitas strategi.

Kesimpulan

AlphaTradingBot adalah strategi intraday pelacakan tren berdasarkan indikator Zigzag dan retracement Fibonacci. Ia menilai tren melalui titik tertinggi dan terendah, dan masuk saat retracement tren, untuk mengejar tingkat kemenangan dan rasio risiko-imbalan yang lebih tinggi. Keunggulan strategi ini terletak pada kemampuan penangkapan tren yang kuat, logika retracement yang jelas, risiko yang terukur, tetapi juga memiliki risiko seperti overtrading, penyimpangan penilaian tren, dan kinerja buruk di pasar sideways. Ke depannya, strategi ini dapat dioptimalkan dari aspek indikator teknis, manajemen posisi, take profit/stop loss, sentimen pasar, dll., untuk meningkatkan stabilitas dan profitabilitas strategi.

- 1