クロコディールライン取引システム Python版

作者: リン・ハーン優しさ, 作成日:2020-05-07 14:33:19, 更新日:2023-11-06 19:40:42

概要

金融取引をした人はおそらく経験があるでしょう. 時々価格変動は規則的ですが,より頻繁にランダムなウォークの不安定な状態を示します. 市場のリスクと機会が隠されているのはこの不安定性です. 不安定性は予測不可能なことも意味します. そのため,予測不可能な市場環境で収益をより安定させる方法もすべてのトレーダーにとって問題です. この記事では,すべての人にインスピレーションを与えることを望んで,ワニ取引ルール戦略を紹介します.

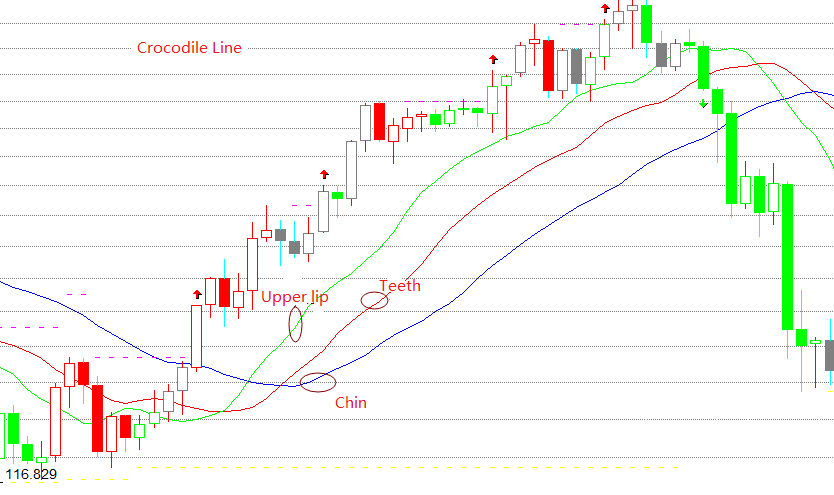

クロコディールラインとは

クロコディール線は,実は3つの特別な移動平均線で,青い線の下巴,赤い線の歯,緑色の線の上唇に対応しています.下巴は13期移動平均線で,未来に8バー移動します.歯は8期移動平均線で,将来に5バー移動します.上唇は5期移動平均線で,将来に3バー移動します.

クロコディールラインの原理

クロコディールラインは,幾何学と非線形動力学に基づいて概括された技術分析方法の集合である. クロコディルの

ワニが眠る時間が長くなるほど,目が覚めたら腹が減るので,目が覚めたら口を大きく開く.上唇が歯の上にあり,歯が

クロコディール線計算式

上唇 = REF ((SMA ((VAR1,5,1),3) 歯 = REF ((SMA ((VAR1,8,1),5) シーン = REF ((SMA ((VAR1,13,1)

クロコジルの戦略組成

ステップ1: 戦略の枠組みを作成する

# Strategy main function

def onTick():

pass

# Program entry

def main ():

while True: # Enter infinite loop mode

onTick() # execute strategy main function

Sleep(1000) # sleep for 1 second

FMZ 投票モードを使用すると,一つは onTick関数で,もう一つはメイン関数で,この onTick関数はメイン関数で無限ループで実行されます.

ステップ2: Python ライブラリをインポートする

import talib

import numpy as np

SMA関数は戦略で使われます. SMAは算術平均値です. タリブライブラリには既に準備済みの SMA関数がありますので,タリブ Python ライブラリを直接インポートして直接呼び出してください. この関数を呼び出すとき,numpy フォーマットパラメータをパスする必要があります. したがって,戦略の初めにこれらの2つの Python ライブラリをインポートするためにインポートを使用する必要があります.

ステップ3:K線配列データを変換する

# Convert the K-line array into an array of highest price, lowest price, and closing price, for conversion to numpy.array

def get_data(bars):

arr = []

for i in bars:

arr.append(i['Close'])

return arr

ここでは get_data 関数を作成しました.この関数の目的は,通常の K 線配列を numpy 形式のデータに処理することです.入力パラメータは K 線配列で,出力結果は numpy 形式の処理データです.

ステップ4:位置データを取得

# Get the number of positions

def get_position ():

# Get position

position = 0 # The number of assigned positions is 0

position_arr = _C (exchange.GetPosition) # Get array of positions

if len (position_arr)> 0: # If the position array length is greater than 0

for i in position_arr:

if i ['ContractType'] == 'rb000': # If the position symbol is equal to the subscription symbol

if i ['Type']% 2 == 0: # If it is long position

position = i ['Amount'] # Assigning a positive number of positions

else:

position = -i ['Amount'] # Assigning a negative number of positions

return position

ポジションステータスには戦略論理が含まれます.最初の10レッスンでは常に仮想ポジションを使用していますが,実際の取引環境では,ポジション方向,ポジション利益と損失,ポジション数などを含む実際のポジション情報を得るためにGetPosition関数を使用することが最善です.

ステップ5:データを取得

exchange.SetContractType('rb000') # Subscribe the futures varieties

bars_arr = exchange.GetRecords() # Get K line array

if len(bars_arr) < 22: # If the number of K lines is less than 22

return

データを取得する前に,まず SetContractType 関数を使用して関連する先物種にサブスクリプトする必要があります. FMZ はすべての中国の商品先物種をサポートします.先物符号にサブスクリプトした後,GetRecords 関数を使用してK線データを取得できます.この関数は配列を返します.

ステップ 6: データ を 計算 する

np_arr = np.array (get_data (bars_arr)) # Convert closing price array

sma13 = talib.SMA (np_arr, 130) [-9] # chin

sma8 = talib.SMA (np_arr, 80) [-6] # teeth

sma5 = talib.SMA (np_arr, 50) [-4] # upper lip

current_price = bars_arr [-1] ['Close'] # latest price

タリブライブラリを使用してSMAを計算する前に,通常のK線配列をnumpyデータに処理するためにnumpyライブラリを使用する必要があります. その後,ワニラインの下巴,歯,上唇を別々に取得します. さらに,注文をするときに価格パラメータを入力する必要があります.

ステップ7 注文する

position = get_position ()

if position == 0: # If there is no position

if current_price> sma5: # If the current price is greater than the upper lip

exchange.SetDirection ("buy") # Set the trading direction and type

exchange.Buy (current_price + 1, 1) # open long position order

if current_price <sma13: # If the current price is less than the chin

exchange.SetDirection ("sell") # Set the trading direction and type

exchange.Sell (current_price-1, 1) # open short position order

if position> 0: # If you have long positions

if current_price <sma8: # If the current price is less than teeth

exchange.SetDirection ("closebuy") # Set the trading direction and type

exchange.Sell (current_price-1, 1) # close long position

if position <0: # If you have short position

if current_price> sma8: # If the current price is greater than the tooth

exchange.SetDirection ("closesell") # Set the trading direction and type

exchange.Buy (current_price + 1, 1) # close short position

オーダーを出す前に,実際のポジションを取得する必要があります.先ほど定義した get_position 関数は実際のポジションの数を返します.現在のポジションが長ければ,正の数を返します.現在のポジションが短ければ,負の数を返します.ポジションがない場合は,0を返します.最後に,上記の取引論理に従って注文を入れるには,買い売り関数を使用しますが,それ以前に,取引方向とタイプも設定する必要があります.

完全な戦略

'' 'backtest

start: 2019-01-01 00:00:00

end: 2020-01-01 00:00:00

period: 1h

exchanges: [{"eid": "Futures_CTP", "currency": "FUTURES"}]

'' '

import talib

import numpy as np

# Convert the K-line array into an array of highest price, lowest price, and closing price, used to convert to numpy.array type data

def get_data (bars):

arr = []

for i in bars:

arr.append (i ['Close'])

return arr

# Get the number of positions

def get_position ():

# Get position

position = 0 # The number of assigned positions is 0

position_arr = _C (exchange.GetPosition) # Get array of positions

if len (position_arr)> 0: # If the position array length is greater than 0

for i in position_arr:

if i ['ContractType'] == 'rb000': # If the position symbol is equal to the subscription symbol

if i ['Type']% 2 == 0: # If it is long

position = i ['Amount'] # Assign a positive number of positions

else:

position = -i ['Amount'] # Assign a negative number of positions

return position

# Strategy main function

def onTick ():

# retrieve data

exchange.SetContractType ('rb000') # Subscribe to futures varieties

bars_arr = exchange.GetRecords () # Get K line array

if len (bars_arr) <22: # If the number of K lines is less than 22

return

# Calculation

np_arr = np.array (get_data (bars_arr)) # Convert closing price array

sma13 = talib.SMA (np_arr, 130) [-9] # chin

sma8 = talib.SMA (np_arr, 80) [-6] # teeth

sma5 = talib.SMA (np_arr, 50) [-4] # upper lip

current_price = bars_arr [-1] ['Close'] # latest price

position = get_position ()

if position == 0: # If there is no position

if current_price> sma5: # If the current price is greater than the upper lip

exchange.SetDirection ("buy") # Set the trading direction and type

exchange.Buy (current_price + 1, 1) # open long position order

if current_price <sma13: # If the current price is less than the chin

exchange.SetDirection ("sell") # Set the trading direction and type

exchange.Sell (current_price-1, 1) # open short position order

if position> 0: # If you have long positions

if current_price <sma8: # If the current price is less than teeth

exchange.SetDirection ("closebuy") # Set the trading direction and type

exchange.Sell (current_price-1, 1) # close long position

if position <0: # If you have short positions

if current_price> sma8: # If the current price is greater than the tooth

exchange.SetDirection ("closesell") # Set the trading direction and type

exchange.Buy (current_price + 1, 1) # close short position

# Program main function

def main ():

while True: # loop

onTick () # execution strategy main function

Sleep (1000) # sleep for 1 second

設定なしで完全な戦略をコピーするには,下記のリンクを直接クリックしてください:https://www.fmz.com/strategy/199025

終わり

クロコディール・トレードルールの最大の役割は,現在の市場価格の変化に関係なく,取引時に市場と同じ方向を維持し,統合市場が現れるまで利益を得続けることを助けることです. クロコディールラインは,他のMACDおよびKDJ指標とうまく使用できます.

- 暗号通貨市場の基本分析を定量化する: データが自分で話せ!

- 通貨圏の基礎的な定量化研究 - 数字を客観的に話すために,あらゆる

教師を信頼しなくていい! - 量化取引の必須ツール - 発明者による量化データ探索モジュール

- すべてをマスターする - FMZの新バージョンの取引ターミナルへの紹介 (TRB仲裁ソースコード)

- FMZの新バージョンの取引端末のご紹介 (TRBの利息ソースコード追加)

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (II)

- 80行のコードで高周波戦略で 脳のない販売ボットを利用する方法

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (II)

- 80行コードの高周波戦略で脳のないロボットを搾取して売る方法

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (I)

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (1)