多重均衡価格トレンド追従と逆張り取引戦略

1

Follow

1802

Followers

戦略概要

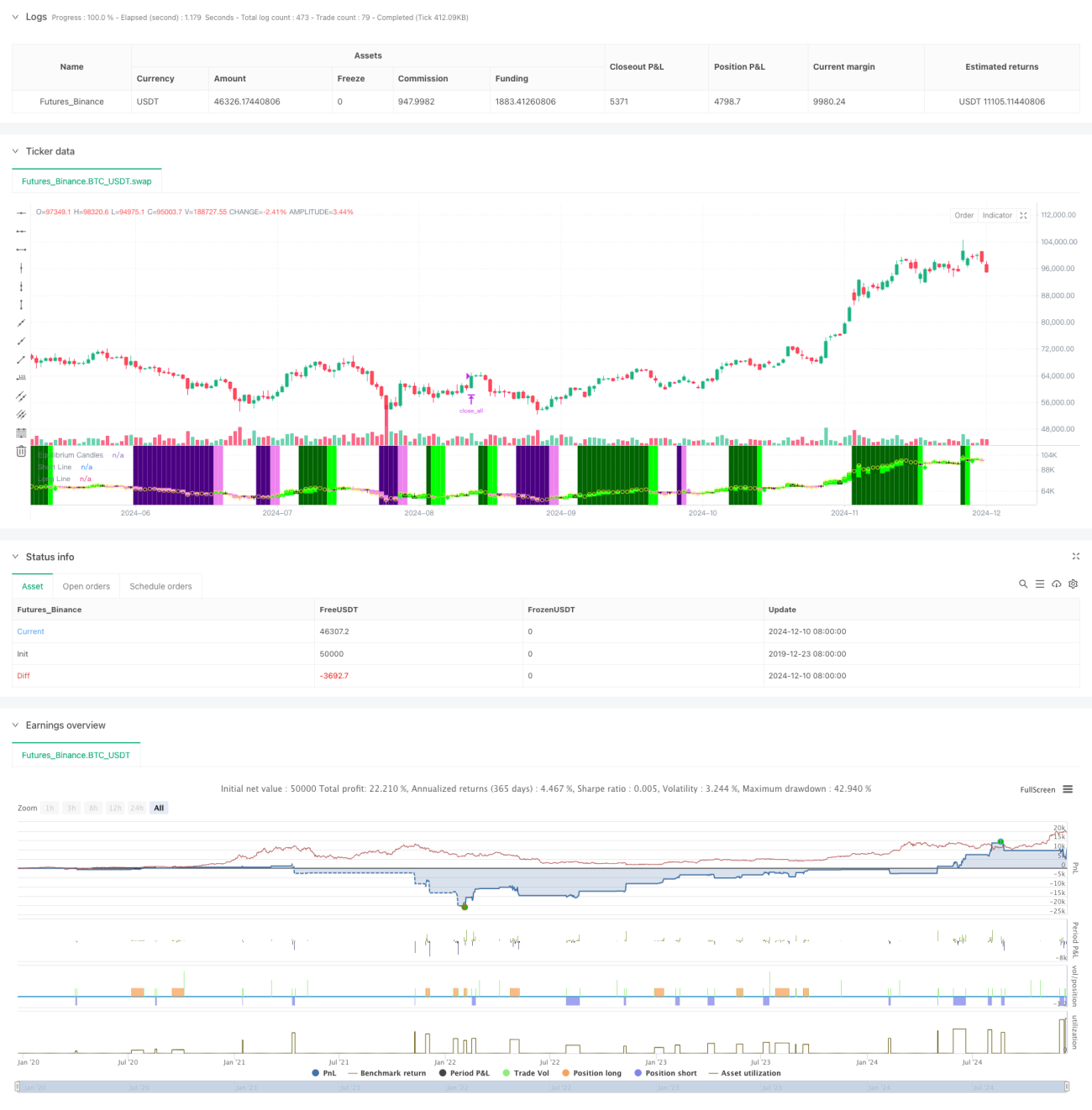

本戦略は、価格均衡点に基づくトレンドフォローおよびリバーサル取引システムです。過去X本のローソク足の最高値と最安値の中間値を計算して均衡価格を決定し、均衡価格に対する終値の位置でトレンド方向を判断します。価格が均衡価格の片側に連続して設定されたロウソク足数だけ維持されると、システムはトレンドが成立したとみなします。最初の押し目(価格が均衡価格をブレイクした時点)でエントリー機会を探します。この戦略は、設定によりトレンドフォローモードまたはリバーサル取引モードを選択できます。

戦略の原理

- 均衡価格の計算: 過去X本のローソク足の最高値と最安値の中間点を均衡価格とします。これは一目均衡図の基準線と同じ計算方法です。

- トレンド判断: 価格が均衡価格の同じ側に連続してX本のローソク足(デフォルト7本)維持された場合、トレンドが成立したと判定します。

- エントリーシグナル: トレンドが確定した後の最初の押し目(価格が均衡価格をブレイクした時点)でエントリーシグナルが発生します。

- 損切り・利確: ATRの60%分位点を使用して、ストップロスと利確の距離を動的に調整し、リスク管理の柔軟性を提供します。

- 大幅変動保護: 均衡点からの価格の乖離が設定されたATR倍率を超えた場合、システムは自動的にポジションをクローズし、大きなドローダウンを防止します。

戦略のメリット

- 適応性が高い: 市場の特性に応じて、トレンドフォローとリバーサル取引モードを柔軟に切り替えられます。

- リスク管理が充実: 動的ATRストップロスを採用し、大幅変動保護メカニズムも備えています。

- 操作が明確: 取引シグナルが明確で、複雑なテクニカル指標の組み合わせに依存しません。

- 視覚効果が良好: カラーのローソク足と背景により、直感的な市場状態の表示を提供します。

- 自動化対応: MT5などの取引プラットフォームと容易に連携でき、自動取引が可能です。

戦略のリスク

- レンジ相場リスク: 横ばいのレンジ相場では、頻繁な偽シグナルが発生する可能性があります。

- スリッページの影響: 激しい変動時には大きなスリッページが生じる恐れがあります。

- パラメータ感応度: 均衡期間やトレンド判断周期などのコアパラメータは、市場ごとに丁寧に最適化する必要があります。

- 市場変動リスク: トレンドからレンジへの転換期には大きなドローダウンが発生する可能性があります。

戦略の最適化方向

- 市場環境認識: 市場環境判断モジュールを追加し、異なる市場条件下で戦略パラメータを動的に調整します。

- シグナルフィルタリング: 出来高やボラティリティなどの補助指標を追加し、偽シグナルをフィルタリングすることを検討します。

- ポジション管理: ボラティリティに基づく動的調整など、より複雑なポジション管理メカニズムを導入します。

- 複数時間枠: 複数の時間枠のシグナルを統合し、取引の精度を向上させます。

- 取引コスト最適化: 取引対象ごとのコスト特性に応じて、エントリー・エグジットのタイミングを最適化します。

まとめ

これは合理的に設計されたトレンド取引システムであり、均衡価格という中核的概念によって明確な取引ロジックを提供します。本戦略の最大の特徴は柔軟性の高さで、トレンドフォローにもリバーサル取引にも使用でき、かつ充実したリスク管理メカニズムを備えています。特定の市場条件下では課題に直面する可能性もありますが、継続的な最適化と柔軟な調整により、多様な市場環境下で安定したパフォーマンスを維持することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1