유튜브 베테랑들의 "마법적인 이중 EMA 전략"

저자:리디아, 창작: 2022-11-07 12:02:31, 업데이트: 2023-09-15 20:51:23

유튜브 베테랑의 마법의 이중 EMA 전략

이 쟁점에서는 유튜브의

전략에서 사용하는 지표

- EMA 지표

디자인의 단순성을 위해, 우리는 비디오에 나열된 이동 평균 지수치를 사용하지 않을 것입니다. 대신 거래 뷰의 내장 된 ta.ema를 사용할 것입니다. (실제로 동일합니다.)

- VuManChu 스윙 프리 표시기

이것은 트레이딩 뷰의 지표입니다. 트레이딩 뷰로 가서 소스 코드를 가져가야 합니다.

VuManChu Swing Free의 코드:

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Credits to the original Script - Range Filter DonovanWall https://www.tradingview.com/script/lut7sBgG-Range-Filter-DW/

// This version is the old version of the Range Filter with less settings to tinker with

//@version=4

study(title="Range Filter - B&S Signals", shorttitle="RF - B&S Signals", overlay=true)

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Functions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Size Function

rng_size(x, qty, n)=>

// AC = Cond_EMA(abs(x - x[1]), 1, n)

wper = (n*2) - 1

avrng = ema(abs(x - x[1]), n)

AC = ema(avrng, wper)*qty

rng_size = AC

//Range Filter Function

rng_filt(x, rng_, n)=>

r = rng_

var rfilt = array.new_float(2, x)

array.set(rfilt, 1, array.get(rfilt, 0))

if x - r > array.get(rfilt, 1)

array.set(rfilt, 0, x - r)

if x + r < array.get(rfilt, 1)

array.set(rfilt, 0, x + r)

rng_filt1 = array.get(rfilt, 0)

hi_band = rng_filt1 + r

lo_band = rng_filt1 - r

rng_filt = rng_filt1

[hi_band, lo_band, rng_filt]

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Inputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Source

rng_src = input(defval=close, type=input.source, title="Swing Source")

//Range Period

rng_per = input(defval=20, minval=1, title="Swing Period")

//Range Size Inputs

rng_qty = input(defval=3.5, minval=0.0000001, title="Swing Multiplier")

//Bar Colors

use_barcolor = input(defval=false, type=input.bool, title="Bar Colors On/Off")

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Definitions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Filter Values

[h_band, l_band, filt] = rng_filt(rng_src, rng_size(rng_src, rng_qty, rng_per), rng_per)

//Direction Conditions

var fdir = 0.0

fdir := filt > filt[1] ? 1 : filt < filt[1] ? -1 : fdir

upward = fdir==1 ? 1 : 0

downward = fdir==-1 ? 1 : 0

//Trading Condition

longCond = rng_src > filt and rng_src > rng_src[1] and upward > 0 or rng_src > filt and rng_src < rng_src[1] and upward > 0

shortCond = rng_src < filt and rng_src < rng_src[1] and downward > 0 or rng_src < filt and rng_src > rng_src[1] and downward > 0

CondIni = 0

CondIni := longCond ? 1 : shortCond ? -1 : CondIni[1]

longCondition = longCond and CondIni[1] == -1

shortCondition = shortCond and CondIni[1] == 1

//Colors

filt_color = upward ? #05ff9b : downward ? #ff0583 : #cccccc

bar_color = upward and (rng_src > filt) ? (rng_src > rng_src[1] ? #05ff9b : #00b36b) :

downward and (rng_src < filt) ? (rng_src < rng_src[1] ? #ff0583 : #b8005d) : #cccccc

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Outputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Plot

filt_plot = plot(filt, color=filt_color, transp=67, linewidth=3, title="Filter")

//Band Plots

h_band_plot = plot(h_band, color=color.new(#05ff9b, 100), title="High Band")

l_band_plot = plot(l_band, color=color.new(#ff0583, 100), title="Low Band")

//Band Fills

fill(h_band_plot, filt_plot, color=color.new(#00b36b, 92), title="High Band Fill")

fill(l_band_plot, filt_plot, color=color.new(#b8005d, 92), title="Low Band Fill")

//Bar Color

barcolor(use_barcolor ? bar_color : na)

//Plot Buy and Sell Labels

plotshape(longCondition, title = "Buy Signal", text ="BUY", textcolor = color.white, style=shape.labelup, size = size.normal, location=location.belowbar, color = color.new(color.green, 0))

plotshape(shortCondition, title = "Sell Signal", text ="SELL", textcolor = color.white, style=shape.labeldown, size = size.normal, location=location.abovebar, color = color.new(color.red, 0))

//Alerts

alertcondition(longCondition, title="Buy Alert", message = "BUY")

alertcondition(shortCondition, title="Sell Alert", message = "SELL")

전략 논리

EMA 지표: 전략은 두 개의 EMA를 사용합니다. 하나는 빠른 라인 (작은 기간 매개 변수) 이며 다른 하나는 느린 라인 (큰 기간 매개 변수) 입니다. 이중 EMA 이동 평균의 목적은 주로 시장 트렌드의 방향을 결정하는 데 도움이됩니다.

-

긴 포지션 계약 빠른 선은 느린 선 위에 있습니다.

-

단기 포지션 계약 빠른 선은 느린 선 아래에 있습니다.

VuManChu Swing Free 인디케이터: VuManChu Swing Free 인디케이터는 신호를 보내고 다른 조건과 결합하여 주문을 할 것인지 판단하는 데 사용됩니다. VuManChu Swing Free 인디케이터 소스 코드에서 longCondition 변수가 구매 신호를 나타내고 shortCondition 변수가 판매 신호를 나타낸다는 것을 알 수 있습니다. 이 두 변수는 주문 조건의 후속 작성에 사용됩니다.

이제 트레이딩 신호의 특정 트리거 조건에 대해 이야기 해 봅시다.

-

롱 포지션에 들어가는 규칙: 긍정적인 K-라인의 폐쇄 가격은 EMA의 빠른 라인의 위에 있어야 하며, 두 EMA는 긴 포지션 (슬로우 라인의 위의 빠른 라인) 이어야 하며, VuManChu Swing Free 지표는 구매 신호를 표시해야 합니다 (longCondition true). 세 가지 조건이 충족되면 이 K-라인은 긴 포지션의 진입을 위한 핵심 K-라인이며, 이 K-라인의 폐쇄 가격은 진입 포지션입니다.

-

짧은 포지션에 들어가는 규칙 (장한 포지션과 달리): 마이너스 K 라인의 폐쇄 가격은 EMA의 빠른 라인의 아래에 있어야 하며, 두 EMA는 짧은 위치 (슬로우 라인의 빠른 라인) 이어야 하며, VuManChu Swing Free 지표는 판매 신호를 표시해야 합니다 (shortCondition is true). 세 가지 조건이 충족되면 K 라인의 폐쇄 가격은 짧은 입점 위치입니다.

거래 논리는 매우 간단합니까? 원본 비디오는 수익 중지 및 손실 중지를 지정하지 않기 때문에, 나는 중간 수익 중지 및 손실 중지 방법을 자유롭게 사용할 것입니다.

코드 설계

VuManChu Swing Free 지표의 코드는, 우리는 어떤 변화도 없이 우리의 전략 코드에 직접 넣었습니다.

그 직후, 우리는 파인 언어 코드 조각을 작성하여 거래 기능을 구현합니다.

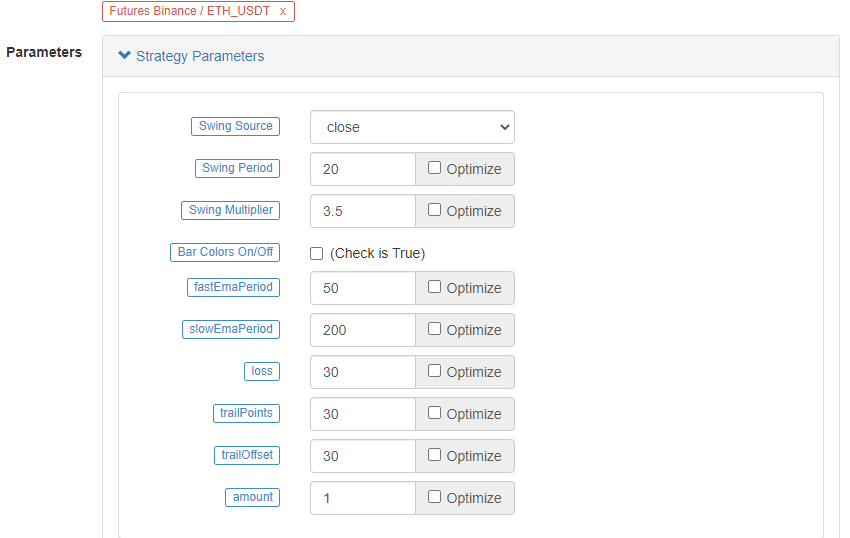

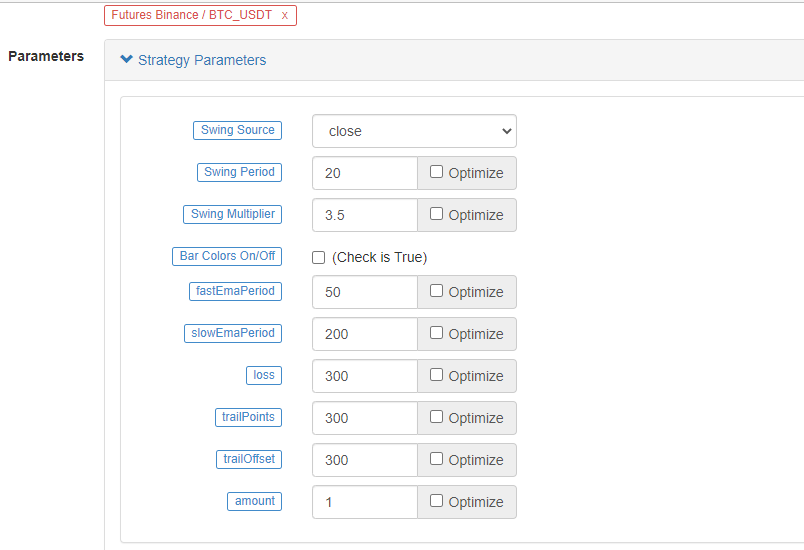

// extend

fastEmaPeriod = input(50, "fastEmaPeriod") // fast line period

slowEmaPeriod = input(200, "slowEmaPeriod") // slow line period

loss = input(30, "loss") // stop loss points

trailPoints = input(30, "trailPoints") // number of trigger points for moving stop loss

trailOffset = input(30, "trailOffset") // moving stop profit offset (points)

amount = input(1, "amount") // order amount

emaFast = ta.ema(close, fastEmaPeriod) // calculate the fast line EMA

emaSlow = ta.ema(close, slowEmaPeriod) // calculate the slow line EMA

buyCondition = longCondition and emaFast > emaSlow and close > open and close > emaFast // entry conditions for long positions

sellCondition = shortCondition and emaFast < emaSlow and close < open and close < emaFast // entry conditions for short positions

if buyCondition and strategy.position_size == 0

strategy.entry("long", strategy.long, amount)

strategy.exit("exit_long", "long", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

if sellCondition and strategy.position_size == 0

strategy.entry("short", strategy.short, amount)

strategy.exit("exit_short", "short", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

A.ItbuyCondition가 true일 때, 즉:

- 변수 longCondition true (VuManChu Swing Free 지표는 긴 위치 신호를 전송합니다.)

- emaFast > emaSlow (EMA 긴 위치 정렬)

- close > open (현행 BAR가 긍정적이라는 것을 의미합니다), close > emaFast (폐기 가격이 EMA 빠른 라인보다 높다는 것을 의미합니다).

3가지 조건은 장기간 유지해야 합니다.

B.sellCondition가 사실이라면, short 포지션을 만드는 세 가지 조건이 유효합니다 (여기에 반복되지 않습니다).

그 다음 우리는 if 조건 판단 신호 트리거의 경우 입점 및 포지션을 열기 위해 전략.입기 기능을 사용 하 여strategy.exit손실을 멈추고 동시에 수익을 추적하는 기능입니다.

전체 코드

/*backtest

start: 2022-01-01 00:00:00

end: 2022-10-08 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

args: [["ZPrecision",0,358374]]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Credits to the original Script - Range Filter DonovanWall https://www.tradingview.com/script/lut7sBgG-Range-Filter-DW/

// This version is the old version of the Range Filter with less settings to tinker with

//@version=4

study(title="Range Filter - B&S Signals", shorttitle="RF - B&S Signals", overlay=true)

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Functions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Size Function

rng_size(x, qty, n)=>

// AC = Cond_EMA(abs(x - x[1]), 1, n)

wper = (n*2) - 1

avrng = ema(abs(x - x[1]), n)

AC = ema(avrng, wper)*qty

rng_size = AC

//Range Filter Function

rng_filt(x, rng_, n)=>

r = rng_

var rfilt = array.new_float(2, x)

array.set(rfilt, 1, array.get(rfilt, 0))

if x - r > array.get(rfilt, 1)

array.set(rfilt, 0, x - r)

if x + r < array.get(rfilt, 1)

array.set(rfilt, 0, x + r)

rng_filt1 = array.get(rfilt, 0)

hi_band = rng_filt1 + r

lo_band = rng_filt1 - r

rng_filt = rng_filt1

[hi_band, lo_band, rng_filt]

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Inputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Source

rng_src = input(defval=close, type=input.source, title="Swing Source")

//Range Period

rng_per = input(defval=20, minval=1, title="Swing Period")

//Range Size Inputs

rng_qty = input(defval=3.5, minval=0.0000001, title="Swing Multiplier")

//Bar Colors

use_barcolor = input(defval=false, type=input.bool, title="Bar Colors On/Off")

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Definitions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Filter Values

[h_band, l_band, filt] = rng_filt(rng_src, rng_size(rng_src, rng_qty, rng_per), rng_per)

//Direction Conditions

var fdir = 0.0

fdir := filt > filt[1] ? 1 : filt < filt[1] ? -1 : fdir

upward = fdir==1 ? 1 : 0

downward = fdir==-1 ? 1 : 0

//Trading Condition

longCond = rng_src > filt and rng_src > rng_src[1] and upward > 0 or rng_src > filt and rng_src < rng_src[1] and upward > 0

shortCond = rng_src < filt and rng_src < rng_src[1] and downward > 0 or rng_src < filt and rng_src > rng_src[1] and downward > 0

CondIni = 0

CondIni := longCond ? 1 : shortCond ? -1 : CondIni[1]

longCondition = longCond and CondIni[1] == -1

shortCondition = shortCond and CondIni[1] == 1

//Colors

filt_color = upward ? #05ff9b : downward ? #ff0583 : #cccccc

bar_color = upward and (rng_src > filt) ? (rng_src > rng_src[1] ? #05ff9b : #00b36b) :

downward and (rng_src < filt) ? (rng_src < rng_src[1] ? #ff0583 : #b8005d) : #cccccc

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Outputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Plot

filt_plot = plot(filt, color=filt_color, transp=67, linewidth=3, title="Filter")

//Band Plots

h_band_plot = plot(h_band, color=color.new(#05ff9b, 100), title="High Band")

l_band_plot = plot(l_band, color=color.new(#ff0583, 100), title="Low Band")

//Band Fills

fill(h_band_plot, filt_plot, color=color.new(#00b36b, 92), title="High Band Fill")

fill(l_band_plot, filt_plot, color=color.new(#b8005d, 92), title="Low Band Fill")

//Bar Color

barcolor(use_barcolor ? bar_color : na)

//Plot Buy and Sell Labels

plotshape(longCondition, title = "Buy Signal", text ="BUY", textcolor = color.white, style=shape.labelup, size = size.normal, location=location.belowbar, color = color.new(color.green, 0))

plotshape(shortCondition, title = "Sell Signal", text ="SELL", textcolor = color.white, style=shape.labeldown, size = size.normal, location=location.abovebar, color = color.new(color.red, 0))

//Alerts

alertcondition(longCondition, title="Buy Alert", message = "BUY")

alertcondition(shortCondition, title="Sell Alert", message = "SELL")

// extend

fastEmaPeriod = input(50, "fastEmaPeriod")

slowEmaPeriod = input(200, "slowEmaPeriod")

loss = input(30, "loss")

trailPoints = input(30, "trailPoints")

trailOffset = input(30, "trailOffset")

amount = input(1, "amount")

emaFast = ta.ema(close, fastEmaPeriod)

emaSlow = ta.ema(close, slowEmaPeriod)

buyCondition = longCondition and emaFast > emaSlow and close > open and close > emaFast

sellCondition = shortCondition and emaFast < emaSlow and close < open and close < emaFast

if buyCondition and strategy.position_size == 0

strategy.entry("long", strategy.long, amount)

strategy.exit("exit_long", "long", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

if sellCondition and strategy.position_size == 0

strategy.entry("short", strategy.short, amount)

strategy.exit("exit_short", "short", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

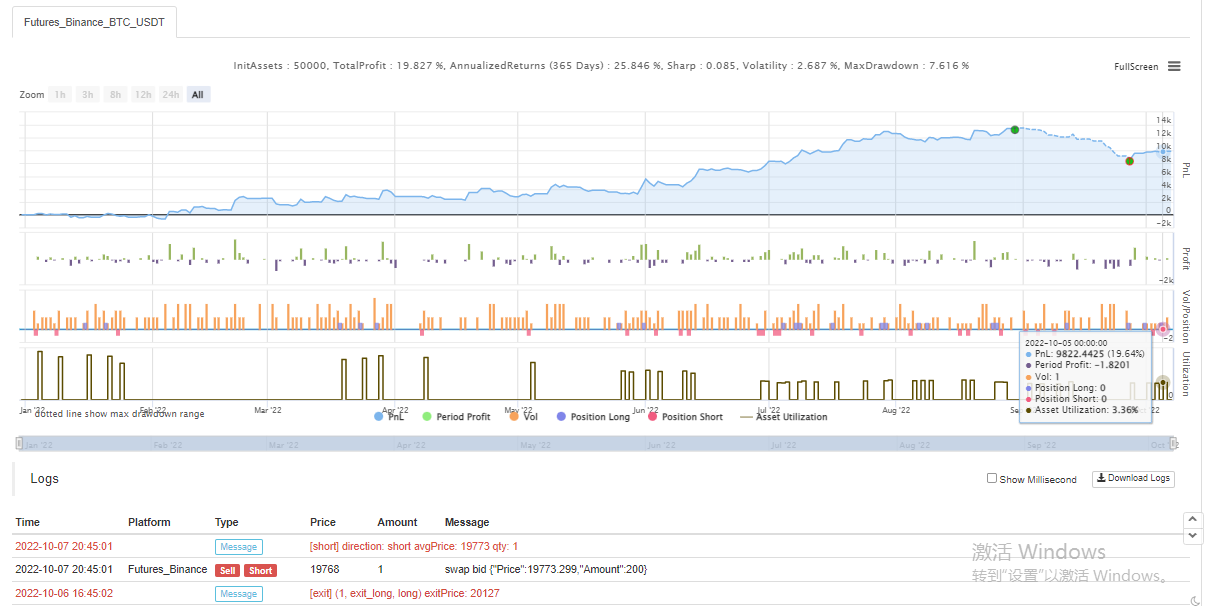

백테스트

백테스트의 시간 범위는 2022년 1월부터 2022년 10월까지이다. K-라인 기간은 15분이며 폐쇄 가격 모델은 백테스트에 사용됩니다. 시장은 바이낸스 ETH_USDT 영구 계약을 선택합니다. 매개 변수는 소스 비디오의 50 기간의 빠른 라인과 200 기간의 느린 라인에 따라 설정됩니다. 다른 매개 변수는 기본적으로 변경되지 않습니다. 나는 스톱 손실 및 추적 스톱 이익 포인트를 주관적으로 30 포인트로 설정합니다.

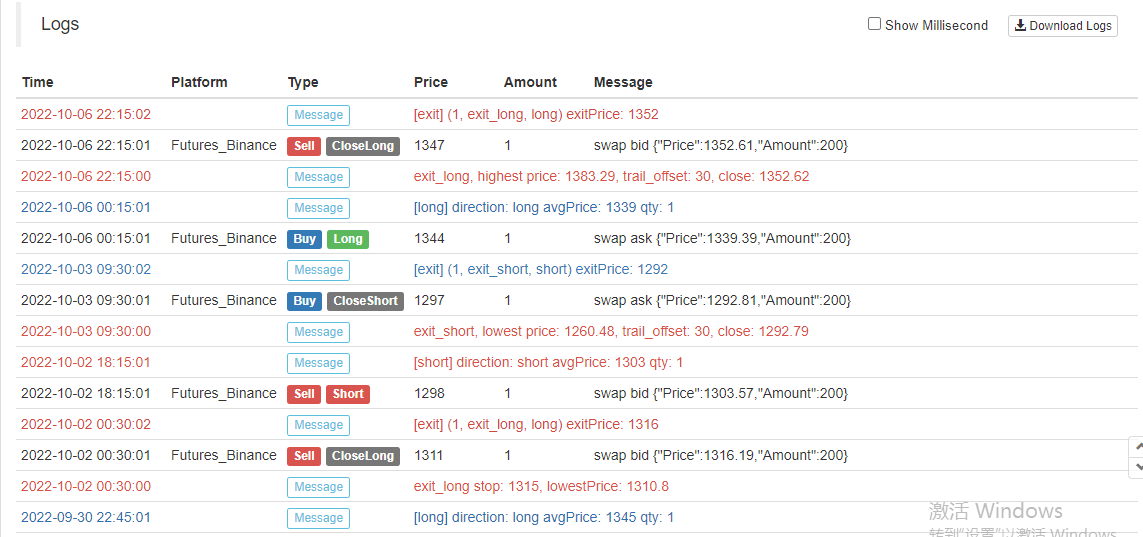

백테스팅의 결과는 평범하며, 스톱-로스 매개 변수는 백테스팅 결과에 어느 정도 영향을 미치는 것 같습니다. 이 측면은 여전히 최적화되고 설계되어야한다고 생각합니다. 그러나 전략 신호가 거래를 유발 한 후에도 승률은 여전히 좋습니다.

다른 BTC_USDT 영구계약을 해보죠:

BTC에 대한 백테스트 결과도 매우 수익성이 높았습니다.

전략:https://www.fmz.com/strategy/385745

트렌드를 파악하기 위해 이 거래 방법은 비교적 신뢰할 수 있는 것으로 보입니다. 이 아이디어에 따라 디자인을 계속 최적화 할 수 있습니다. 이 기사에서 우리는 이중 이동 평균 전략의 아이디어를 알게 될뿐만 아니라 유튜브에서 베테랑의 전략을 처리하고 배우는 방법을 배웠습니다. 좋습니다, 위의 전략 코드는 단지 내 벽돌과 가죽입니다, 백테스트 결과는 특정 실제 봇 결과를 나타내지 않으며 전략 코드, 디자인은 참조만을위한 것입니다. 지원에 감사드립니다, 다음 번에 다시 만나요!

- 암호화폐 시장의 근본 분석을 정량화: 데이터를 스스로 이야기하도록!

- 동전圈의 기초적인 양적 연구 - 더 이상 모든

선생님들을 믿지 말고, 데이터를 객관적으로 이야기하십시오! - 양적 거래의 필수 도구 - 발명자 양적 데이터 탐색 모듈

- 모든 것을 마스터 - FMZ에 대한 소개 트레이딩 터미널의 새로운 버전 (TRB 중재 소스 코드)

- FMZ의 새로운 거래 단말기 소개 (TRB 리비트 소스 추가)

- FMZ 퀀트: 암호화폐 시장에서 공통 요구 사항 설계 예제 분석 (II)

- 80 줄의 코드에서 고주파 전략으로 뇌 없는 판매봇을 이용하는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (II)

- 80줄의 코드의 고주파 전략으로 뇌 없는 로봇을 파는 방법

- FMZ Quant: 암호화폐 시장에서 공통 요구 사항 디자인 예의 분석 (I)

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (1)