더 나은 도구는 더 좋은 일을 합니다. 거래 원칙을 분석하기 위해 연구 환경을 사용하는 법을 배우세요.

저자:리디아, 창작: 2022-12-27 16:33:51, 업데이트: 2023-09-20 09:17:27

더 나은 도구는 좋은 일을 만듭니다. 거래 원칙을 분석하기 위해 연구 환경을 사용하는 법을 배우십시오.

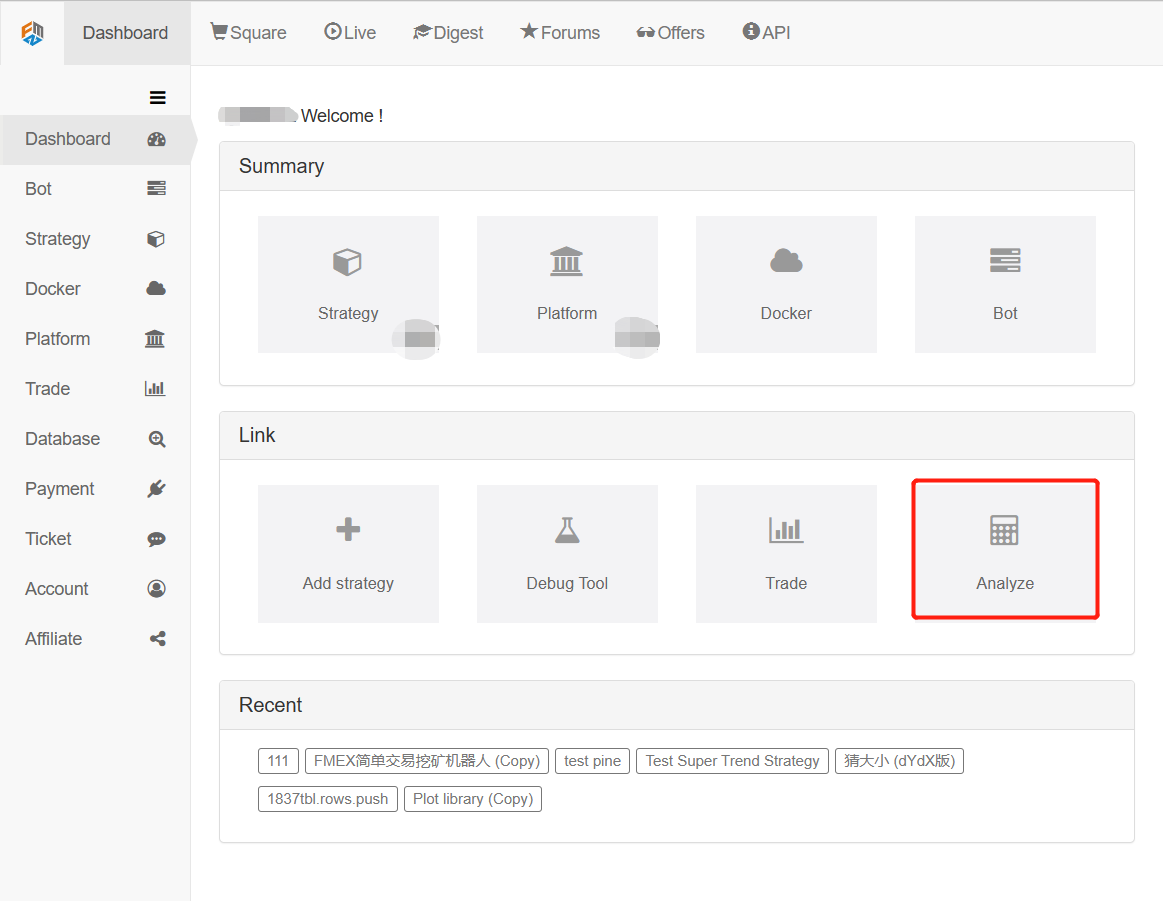

FMZ 퀀트 플랫폼의 대시보드에서

여기서 분석 파일을 직접 업로드합니다.

이 분석 문서는 백테스팅 동안 선물 스팟 헤지 포지션의 개장 및 폐쇄 과정을 분석합니다. 선물 거래소는 OKX 선물이며 계약은quarter거래상 거래는 OKX 통화-화폐 거래이며 거래 쌍은BTC_USDT. 선물 스팟 헤지의 운영 프로세스를 분석하려면 다음의 특정 연구 환경 파일을 볼 수 있습니다. 두 가지 버전으로 작성되었습니다. 파이썬 언어 버전, 자바스크립트 언어 버전.

연구 환경 파이썬 언어 파일

선물 포트 헤지링 원칙에 대한 분석.ipynb [1]에서:

from fmz import *

task = VCtx('''backtest

start: 2019-09-19 00:00:00

end: 2019-09-28 12:00:00

period: 15m

exchanges: [{"eid":"Futures_OKCoin","currency":"BTC_USD", "stocks":1}, {"eid":"OKX","currency":"BTC_USDT","balance":10000,"stocks":0}]

''')

# Create backtesting environment

import matplotlib.pyplot as plt

import numpy as np

# Import the plot library matplotlib and library numpy

[2]에서:

exchanges[0].SetContractType("quarter") # The first exchange object OKX Futures (eid: Futures_OKCoin) calls the function to set the current contract as a quarterly contract

initQuarterAcc = exchanges[0].GetAccount() # The initial account information of OKX Futures Exchange is recorded in the variable initQuarterAcc

initQuarterAcc

외출[2]:

{

[3]에서:

initSpotAcc = exchanges[1].GetAccount() # The initial account information of the OKX Spot Exchange is recorded in the variable initSpotAcc

initSpotAcc

아웃[3]:

{

[4]:

quarterTicker1 = exchanges[0].GetTicker() # Get the futures exchange ticker, recorded in the variable quarterTicker1

quarterTicker1

아웃[4]:

시간: 1568851210000,

[5]에서:

spotTicker1 = exchanges[1].GetTicker() # Get the spot exchange ticker, recorded in the variable spotTicker1

spotTicker1

외출[5]:

시간: 1568851210000,

[6]에서:

quarterTicker1.Buy - spotTicker1.Sell # The price difference between going short on futures and going long on spot.

외출[6]: 284.6499999799999985

[7]에서:

exchanges[0].SetDirection("sell") # Set up a futures exchange and trade in the direction of going short

quarterId1 = exchanges[0].Sell(quarterTicker1.Buy, 10) # Futures go short to place orders. The order quantity is 10 contracts. The returned order ID is recorded in the variable quarterId1.

exchanges[0].GetOrder(quarterId1) # Check the details of the order with futures order ID quarterId1.

아웃[7]:

1번

[8]에서:

spotAmount = 10 * 100 / quarterTicker1.Buy # Calculate the currency equivalent of 10 contracts as the order quantity of the spot.

spotId1 = exchanges[1].Buy(spotTicker1.Sell, spotAmount) # Place orders on the spot exchange

exchanges[1].GetOrder(spotId1) # Check the order details of the spot order ID of spotId1

아웃[8]:

1개

가격: 10156.60000002,

금액: 0.0957

거래 금액: 0.0957,

평균 가격은 10156.60000002입니다.

분기 ID1 및 스팟 ID1 명령이 완전히 채워졌다는 것을 볼 수 있습니다. 즉, 개방된 포지션의 헤딩이 완료되었습니다.

[9]에서:

Sleep(1000 * 60 * 60 * 24 * 7) # Hold the position for a while and wait for the price difference to become smaller to close the position.

대기 시간이 지나면, 포지션을 닫기 위해 준비.quarterTicker2, spotTicker2그리고 그들을 인쇄합니다.

선물 거래 대상의 거래 방향은 짧은 지위를 닫기 위해 설정됩니다.exchanges[0].SetDirection("closesell")포지션을 닫는 명령을 내립니다.

클로저 포지션 오더의 세부 정보를 인쇄하여 클로저 오더가 완료되었다고 표시합니다.

[10]에서:

quarterTicker2 = exchanges[0].GetTicker() # Get the current futures exchange ticker, recorded in the variable quarterTicker2

quarterTicker2

아웃[10]:

시간: 1569456010000,

[11]에서:

spotTicker2 = exchanges[1].GetTicker() # Get the current ticker of the spot exchange, recorded in the variable spotTicker2

spotTicker2

아웃[11]:

시간: 1569456114600

[12]에서:

quarterTicker2.Sell - spotTicker2.Buy # The price difference between closing a short futures position and closing a long spot position.

아웃[12]: 52.5000200100003

[13]에서:

exchanges[0].SetDirection("closesell") # Set the current trading direction of the futures exchange to close short positions.

quarterId2 = exchanges[0].Buy(quarterTicker2.Sell, 10) # The futures exchange places an order to close a position and records the order ID to the variable quarterId2.

exchanges[0].GetOrder(quarterId2) # Check futures close out order details

아웃[13]:

2명

[14]에서:

spotId2 = exchanges[1].Sell(spotTicker2.Buy, spotAmount) # The spot exchange places an order to close a position and records the order ID, which is recorded to the variable spotId2.

exchanges[1].GetOrder(spotId2) # Check spot close out order details

아웃[14]:

2명

가격: 8444.69999999,

금액: 0.0957

거래 금액: 0.0957

평균 가격: 8444.69999999,

[15]에서:

nowQuarterAcc = exchanges[0].GetAccount() # Get the current futures exchange account information, recorded in the variable nowQuarterAcc.

nowQuarterAcc

외출[15]:

{

[16]에서:

nowSpotAcc = exchanges[1].GetAccount() # Get the current spot exchange account information, recorded in the variable nowSpotAcc.

nowSpotAcc

외출[16]:

초기계산과 courant계산을 비교함으로써 헤지업의 이익과 손실이 계산됩니다.

[17]에서:

diffStocks = abs(nowQuarterAcc.Stocks - initQuarterAcc.Stocks)

diffBalance = nowSpotAcc.Balance - initSpotAcc.Balance

if nowQuarterAcc.Stocks - initQuarterAcc.Stocks > 0 :

print("profits:", diffStocks * spotTicker2.Buy + diffBalance)

else :

print("profits:", diffBalance - diffStocks * spotTicker2.Buy)

아웃[17]: 이익: 18.72350977580652

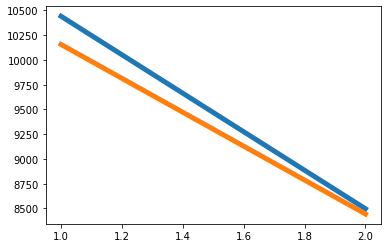

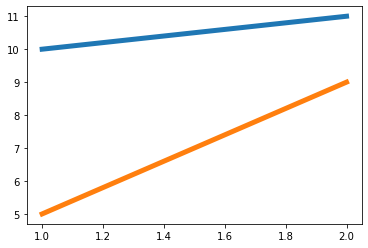

이제 왜 헤딩이 수익성이 있는지 봅시다. 그래프를 그려보겠습니다. 선물 가격은 파란색 선이고 스포트 가격은 오렌지 선입니다. 두 가격 모두 감소하고 있습니다. 선물 가격은 스포트 가격보다 빠르게 감소하고 있습니다.

[18]에서:

xQuarter = [1, 2]

yQuarter = [quarterTicker1.Buy, quarterTicker2.Sell]

xSpot = [1, 2]

ySpot = [spotTicker1.Sell, spotTicker2.Buy]

plt.plot(xQuarter, yQuarter, linewidth=5)

plt.plot(xSpot, ySpot, linewidth=5)

plt.show()

아웃[18]:

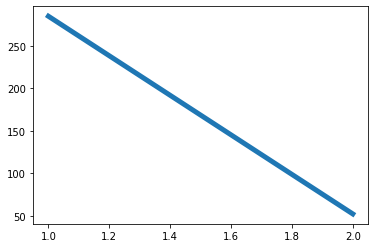

가격 차이의 변화를 살펴보자. 가격 차이는 헤지 개설 지점 (즉, 선물은 짧고 스팟은 길다) 의 284에서 포지션 종료 시점 (퓨처 짧은 지점 폐쇄, 스팟 긴 지점 폐쇄) 의 52까지 다양합니다. 가격 차이는 크기에서 작습니다.

[19]에서:

xDiff = [1, 2]

yDiff = [quarterTicker1.Buy - spotTicker1.Sell, quarterTicker2.Sell - spotTicker2.Buy]

plt.plot(xDiff, yDiff, linewidth=5)

plt.show()

아웃[19]:

예를 들어, a1은 시간 1의 선물 가격이고, b1은 시간 1의 스팟 가격이다. A2는 시간 2의 선물 가격이고, b2는 시간 2의 스팟 가격이다.시점 1 (a1-b1) 의 선물 현장 가격 차이는 시점 2 (a2-b2) 의 선물 현장 가격 차이보다 크면 a1 - a2>b1 - b2를 도입할 수 있습니다. 세 가지 상황이 있습니다. (미래상과 현금상의 양은 동일합니다.)

-

a1 - a2는 0보다 크다 b1 - b2는 0보다 크다 a1 - a2는 선물 수익의 가격 차이, 그리고 b1 - b2는 스팟 손실의 가격 차이 (스팟이 길어졌기 때문에 구매 시작 가격은 포지션을 닫는 판매 가격보다 높으므로 돈이 손실됩니다) 를 나타냅니다. 그러나 선물 수익은 스팟 손실보다 크습니다. 따라서 전체적으로 수익성이 있습니다. 이 상황은 단계 [8]의 차트에 해당합니다.

-

a1 - a2는 0보다 크다 b1 - b2는 0보다 작다 a1 - a2는 선물 수익의 가격 차이이고, b1 - b2는 스팟 수익의 가격 차이입니다 (b1 - b2는 0보다 작으며, b2가 b1보다 크다는 것을 나타냅니다. 즉, 포지션 개설 및 구매 가격은 낮고, 판매 및 폐쇄 가격은 높으므로 수익성이 있습니다.)

-

a1 - a2 0 보다 작다 b1 - b2 0 보다 작다 a1 - a2는 선물 손실의 가격 차이이고, b1 - b2는 즉석 이익의 가격 차이입니다. a1 - a2 > b1 - b2이기 때문에, a1 - a2의 절대 값은 b1 - b2의 절대 값보다 작고, 즉석 이익은 선물 손실보다 크습니다. 전체적으로 수익성이 있습니다.

a1 - a2가 0보다 작고 b1 - b2가 0보다 크다는 경우는 없습니다. 왜냐하면 a1 - a2 > b1 - b2가 정의되었기 때문입니다. 마찬가지로, a1 - a2가 0과 같다면, a1 - a2 > b1 - b2가 정의되기 때문에, b1 - b2는 0보다 작아야합니다. 따라서, 짧은 선물과 긴 스팟의 헤지 방식이 a1 - b1 > a2 - b2의 조건을 충족하는 한, 개장 및 폐쇄 포지션 작업은 수익 헤지입니다.

예를 들어, 다음 모델은 다음과 같은 경우 중 하나입니다.

[20]에서:

a1 = 10

b1 = 5

a2 = 11

b2 = 9

# a1 - b1 > a2 - b2 launches: a1 - a2 > b1 - b2

xA = [1, 2]

yA = [a1, a2]

xB = [1, 2]

yB = [b1, b2]

plt.plot(xA, yA, linewidth=5)

plt.plot(xB, yB, linewidth=5)

plt.show()

외출[20]:

검색 환경 자바스크립트 언어 파일

연구 환경은 파이썬뿐만 아니라 자바스크립트도 지원합니다. 자바스크립트 연구 환경의 예를 들어보겠습니다.

선물 포트 헤지링 원칙 분석 (JavaScript).ipynb [1]에서:

// Import the required package, click "Save settings" on the FMZ's "Strategy editing page" to get the string configuration and convert it to an object.

var fmz = require("fmz") // Import the talib, TA, and plot libraries automatically after import

var task = fmz.VCtx({

start: '2019-09-19 00:00:00',

end: '2019-09-28 12:00:00',

period: '15m',

exchanges: [{"eid":"Futures_OKCoin","currency":"BTC_USD","stocks":1},{"eid":"OKX","currency":"BTC_USDT","balance":10000,"stocks":0}]

})

[2]에서:

exchanges[0].SetContractType("quarter") // The first exchange object OKX Futures (eid: Futures_OKCoin) calls the function to set the current contract as a quarterly contract.

var initQuarterAcc = exchanges[0].GetAccount() // The initial account information of OKX Futures Exchange is recorded in the variable initQuarterAcc.

initQuarterAcc

외출[2]: { 재고: 0, 냉동재고: 0}

[3]에서:

var initSpotAcc = exchanges[1].GetAccount() // The initial account information of the OKX Spot Exchange is recorded in the variable initSpotAcc.

initSpotAcc

아웃[3]: { 재고: 10,000, FrozenBalance: 0, 재고: 0, FrozenStocks: 0 }

[4]:

var quarterTicker1 = exchanges[0].GetTicker() // Get the futures exchange ticker, recorded in the variable quarterTicker1.

quarterTicker1

아웃[4]: 시간: 1568851210000, 높은: 10441.25002, 낮은: 10441.25, 판매: 10441.25002, 구매: 10441.25, 마지막: 10441.25001 부: 1772, 오픈인터레스: 0 }

[5]에서:

var spotTicker1 = exchanges[1].GetTicker() // Get the spot exchange ticker, recorded in the variable spotTicker1.

spotTicker1

외출[5]: 시간: 1568851210000, 높은: 10156.60000002, 낮은: 10156.6, 판매: 10156.60000002, 구매: 10156.6, 마지막: 10156.60000001, 부문: 7.4443 오픈인터레스: 0 }

[6]에서:

quarterTicker1.Buy - spotTicker1.Sell // The price difference between going short on futures and going long on spot.

아웃[6]: 284.6499999799999985 [7]에서:

exchanges[0].SetDirection("sell") // Set up a futures exchange and trade in the direction of going short

var quarterId1 = exchanges[0].Sell(quarterTicker1.Buy, 10) // Go short futures to place orders. The order quantity is 10 contracts. The returned order ID is recorded in the variable quarterId1.

exchanges[0].GetOrder(quarterId1) // Check the details of the order with futures order ID quarterId1.

아웃[7]:

{ id: 1,

가격은: 10441.25,

양: 10개

거래 금액: 10,

평균 가격: 10441.25,

종류: 1,

오프셋: 0

상태: 1,

계약 유형:

[8]에서:

var spotAmount = 10 * 100 / quarterTicker1.Buy // Calculate the currency equivalent of 10 contracts as the order quantity of the spot.

var spotId1 = exchanges[1].Buy(spotTicker1.Sell, spotAmount) // Place orders on the spot exchange.

exchanges[1].GetOrder(spotId1) // Check the order details of the spot order ID of spotId1.

아웃[8]:

{ id: 1,

가격: 10156.60000002,

금액: 0.0957

거래 금액: 0.0957

평균 가격: 10156.60000002,

타입: 0

오프셋: 0

상태: 1,

계약 유형:

quarterId1과 spotId1의 명령이 완전히 채워졌다는 것을 볼 수 있습니다. 즉, 개설 포지션의 헤딩이 완료되었습니다.

[9]에서:

Sleep(1000 * 60 * 60 * 24 * 7) // Hold the position for a while and wait for the price difference to become smaller to close the position.

대기 시간이 지나면, 포지션을 닫기 위해 준비.quarterTicker2, spotTicker2그리고 그들을 인쇄합니다.

선물 거래 대상의 거래 방향은 짧은 지위를 닫기 위해 설정됩니다.exchanges[0].SetDirection("closesell")포지션을 닫는 명령을 내립니다.

클로저 포지션 오더의 세부 정보를 인쇄하여 클로저 오더가 완료되었다고 표시합니다.

[10]에서:

var quarterTicker2 = exchanges[0].GetTicker() // Get the current futures exchange ticker, recorded in the variable quarterTicker2.

quarterTicker2

아웃[10]: 시간: 1569456010000, 높은: 8497.20002, 낮은: 8497.2, 판매: 8497.20002, 구매: 8497.2, 마지막: 8497.20001 부문: 4311, 오픈인터레스: 0 }

[11]에서:

var spotTicker2 = exchanges[1].GetTicker() // Get the current ticker of the spot exchange, recorded in the variable spotTicker2.

spotTicker2

아웃[11]: { 시간: 1569456114600, 높은: 8444.70000001, 낮은: 8444.69999999, 판매: 8444.70000001, 구매: 8444.69999999, 마지막: 8444.7 78.6273 부지 오픈인터레스: 0 }

[12]에서:

quarterTicker2.Sell - spotTicker2.Buy // The price difference between closing short position of futures and closing long position of spot.

아웃[12]: 52.5000200100003

[13]에서:

exchanges[0].SetDirection("closesell") // Set the current trading direction of the futures exchange to close short positions.

var quarterId2 = exchanges[0].Buy(quarterTicker2.Sell, 10) // The futures exchange places an order to close the position, and records the order ID to the variable quarterId2.

exchanges[0].GetOrder(quarterId2) // Check futures closing position order details.

아웃[13]:

{ id: 2,

가격: 8497.20002,

양: 10개

거래 금액: 10,

평균 가격: 8493.95335,

타입: 0

오프셋: 1,

상태: 1,

계약 유형:

[14]에서:

var spotId2 = exchanges[1].Sell(spotTicker2.Buy, spotAmount) // The spot exchange places an order to close the position, and records the order ID to the variable spotId2.

exchanges[1].GetOrder(spotId2) // Check spot closing position order details.

아웃[14]:

{ id: 2,

가격은: 8444.69999999,

금액: 0.0957

거래 금액: 0.0957,

평균 가격: 8444.69999999,

종류: 1,

오프셋: 0

상태: 1,

계약 타입:

[15]에서:

var nowQuarterAcc = exchanges[0].GetAccount() // Get the current futures exchange account information, recorded in the variable nowQuarterAcc.

nowQuarterAcc

외출[15]: { 잔액: 0, 얼어붙은 밸런스: 0 물자: 1.021786026184 FrozenStocks: 0

[16]에서:

var nowSpotAcc = exchanges[1].GetAccount() // Get the current spot exchange account information, recorded in the variable nowSpotAcc.

nowSpotAcc

외출[16]: { 잔액: 9834.74705446, 얼어붙은 밸런스: 0 양: 0, FrozenStocks: 0 초기계산과 courant계산을 비교함으로써 헤지업의 이익과 손실이 계산됩니다.

[17]에서:

var diffStocks = Math.abs(nowQuarterAcc.Stocks - initQuarterAcc.Stocks)

var diffBalance = nowSpotAcc.Balance - initSpotAcc.Balance

if (nowQuarterAcc.Stocks - initQuarterAcc.Stocks > 0) {

console.log("profits:", diffStocks * spotTicker2.Buy + diffBalance)

} else {

console.log("profits:", diffBalance - diffStocks * spotTicker2.Buy)

}

아웃[17]: 이익: 18.72350977580652

이제 왜 헤딩이 수익성이 있는지 봅시다. 그래프를 그려보겠습니다. 선물 가격은 파란색 선이고 스포트 가격은 오렌지 선입니다. 두 가격 모두 감소하고 있습니다. 선물 가격은 스포트 가격보다 빠르게 감소하고 있습니다.

[18]에서:

var objQuarter = {

"index" : [1, 2], // The index is 1, that is, the first time, the opening time, and 2 is the closing time.

"arrPrice" : [quarterTicker1.Buy, quarterTicker2.Sell],

}

var objSpot = {

"index" : [1, 2],

"arrPrice" : [spotTicker1.Sell, spotTicker2.Buy],

}

plot([{name: 'quarter', x: objQuarter.index, y: objQuarter.arrPrice}, {name: 'spot', x: objSpot.index, y: objSpot.arrPrice}])

아웃[18]: 가격 차이의 변화를 살펴보자. 가격 차이는 헤지 오픈 포지션 (즉, 선물은 짧고 스팟은 길게) 의 284에서 폐쇄 (예약의 짧은 포지션 폐쇄 및 스팟의 긴 포지션 폐쇄) 의 52까지 다양합니다. 가격 차이는 크기에서 작습니다.

[19]에서:

var arrDiffPrice = [quarterTicker1.Buy - spotTicker1.Sell, quarterTicker2.Sell - spotTicker2.Buy]

plot(arrDiffPrice)

아웃[19]:예를 들어, a1은 시간 1의 선물 가격이고, b1은 시간 1의 스팟 가격이다. A2는 시간 2의 선물 가격이고, b2는 시간 2의 스팟 가격이다.시점 1 (a1-b1) 의 선물 현장 가격 차이는 시점 2 (a2-b2) 의 선물 현장 가격 차이보다 크면 a1 - a2>b1 - b2를 도입할 수 있습니다. 세 가지 상황이 있습니다. (미래상과 현금상의 양은 동일합니다.)

-

a1 - a2는 0보다 크다 b1 - b2는 0보다 크다 a1 - a2는 선물 수익의 가격 차이, 그리고 b1 - b2는 스팟 손실의 가격 차이 (스팟이 길어졌기 때문에 구매 시작 가격은 포지션을 닫는 판매 가격보다 높으므로 돈이 손실됩니다) 를 나타냅니다. 그러나 선물 수익은 스팟 손실보다 크습니다. 따라서 전체적으로 수익성이 있습니다. 이 상황은 단계 [8]의 차트에 해당합니다.

-

a1 - a2는 0보다 크다 b1 - b2는 0보다 작다 a1 - a2는 선물 수익의 가격 차이이고, b1 - b2는 스팟 수익의 가격 차이입니다 (b1 - b2는 0보다 작으며, b2가 b1보다 크다는 것을 나타냅니다. 즉, 포지션 개설 및 구매 가격은 낮고, 판매 및 폐쇄 가격은 높으므로 수익성이 있습니다.)

-

a1 - a2 0 보다 작다 b1 - b2 0 보다 작다 a1 - a2는 선물 손실의 가격 차이이고, b1 - b2는 즉석 이익의 가격 차이입니다. a1 - a2 > b1 - b2이기 때문에, a1 - a2의 절대 값은 b1 - b2의 절대 값보다 작고, 즉석 이익은 선물 손실보다 크습니다. 전체적으로 수익성이 있습니다.

a1 - a2가 0보다 작고 b1 - b2가 0보다 크다는 경우는 없습니다. 왜냐하면 a1 - a2 > b1 - b2가 정의되었기 때문입니다. 마찬가지로, a1 - a2가 0과 같다면, a1 - a2 > b1 - b2가 정의되기 때문에, b1 - b2는 0보다 작아야합니다. 따라서, 짧은 선물과 긴 스팟의 헤지 방식이 a1 - b1 > a2 - b2의 조건을 충족하는 한, 개장 및 폐쇄 포지션 작업은 수익 헤지입니다.

예를 들어, 다음 모델은 다음과 같은 경우 중 하나입니다.

[20]에서:

var a1 = 10

var b1 = 5

var a2 = 11

var b2 = 9

// a1 - b1 > a2 - b2 launches: a1 - a2 > b1 - b2

var objA = {

"index" : [1, 2],

"arrPrice" : [a1, a2],

}

var objB = {

"index" : [1, 2],

"arrPrice" : [b1, b2],

}

plot([{name : "a", x : objA.index, y : objA.arrPrice}, {name : "b", x : objB.index, y : objB.arrPrice}])

외출[20]:

시도해 보세요!

- 암호화폐 시장의 근본 분석을 정량화: 데이터를 스스로 이야기하도록!

- 동전圈의 기초적인 양적 연구 - 더 이상 모든

선생님들을 믿지 말고, 데이터를 객관적으로 이야기하십시오! - 양적 거래의 필수 도구 - 발명자 양적 데이터 탐색 모듈

- 모든 것을 마스터 - FMZ에 대한 소개 트레이딩 터미널의 새로운 버전 (TRB 중재 소스 코드)

- FMZ의 새로운 거래 단말기 소개 (TRB 리비트 소스 추가)

- FMZ 퀀트: 암호화폐 시장에서 공통 요구 사항 설계 예제 분석 (II)

- 80 줄의 코드에서 고주파 전략으로 뇌 없는 판매봇을 이용하는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (II)

- 80줄의 코드의 고주파 전략으로 뇌 없는 로봇을 파는 방법

- FMZ Quant: 암호화폐 시장에서 공통 요구 사항 디자인 예의 분석 (I)

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (1)