Contoh reka bentuk strategi dYdX

Penulis:Lydia, Dicipta: 2022-11-07 10:59:29, Dikemas kini: 2023-09-15 21:03:43

Sebagai tindak balas kepada permintaan ramai pengguna, platform FMZ telah mengakses dYdX baru-baru ini, pertukaran terdesentralisasi. Seseorang yang mempunyai strategi boleh menikmati proses memperoleh mata wang digital dYdX. Saya hanya mahu menulis strategi perdagangan stokastik untuk masa yang lama, tidak kira sama ada ia membuat keuntungan. Jadi seterusnya kita datang bersama untuk merancang strategi pertukaran stokastik, tidak kira strategi berfungsi dengan baik atau tidak, kita hanya belajar reka bentuk strategi.

Reka bentuk strategi dagangan stokastik

Mari kita bertukar fikiran! Ia dirancang untuk merancang strategi meletakkan pesanan secara rawak dengan penunjuk rawak dan harga. Menempatkan pesanan tidak lebih daripada pergi panjang atau pergi pendek, hanya bertaruh pada kebarangkalian. Kemudian kita akan menggunakan nombor rawak 1 ~ 100 untuk menentukan sama ada untuk pergi panjang atau pergi pendek.

Syarat untuk pergi panjang: nombor rawak 1 ~ 50. Syarat untuk pergi pendek: nombor rawak 51 ~ 100.

Oleh itu, kedua-dua pergi panjang dan pergi pendek adalah 50 nombor. Seterusnya, mari kita fikirkan bagaimana untuk menutup kedudukan, kerana ia adalah pertaruhan, maka mesti ada kriteria untuk menang atau kalah. Kami menetapkan kriteria untuk keuntungan berhenti tetap dan kerugian dalam urus niaga. Hentikan keuntungan untuk menang, hentikan kerugian untuk kehilangan. Mengenai jumlah keuntungan berhenti dan kerugian, ia sebenarnya kesan nisbah keuntungan dan kerugian, oh ya! Ia juga mempengaruhi kadar kemenangan! (Adakah reka bentuk strategi ini berkesan? Bolehkah ia dijamin sebagai jangkaan matematik positif? Lakukan terlebih dahulu! (Selepas itu, hanya untuk pembelajaran, penyelidikan!)

Perdagangan tidak bebas kos, terdapat cukup slippage, yuran, dan lain-lain untuk menarik kadar kemenangan perdagangan stokastik kami ke arah bahagian kurang daripada 50%. Jadi bagaimana untuk merancangnya secara berterusan? Bagaimana dengan merancang pengganda untuk meningkatkan kedudukan? Oleh kerana ia adalah pertaruhan, maka kebarangkalian kehilangan selama 8 ~ 10 kali dalam satu barisan perdagangan rawak harus rendah. Jadi transaksi pertama direka untuk meletakkan sejumlah kecil pesanan, sekecil mungkin. Kemudian jika saya kalah, saya akan meningkatkan jumlah pesanan dan terus meletakkan pesanan secara rawak.

OK, strategi ini direka dengan mudah.

Kod sumber direka:

var openPrice = 0

var ratio = 1

var totalEq = null

var nowEq = null

function cancelAll() {

while (1) {

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

break

}

for (var i = 0 ; i < orders.length ; i++) {

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

Sleep(500)

}

}

function main() {

if (isReset) {

_G(null)

LogReset(1)

LogProfitReset()

LogVacuum()

Log("reset all data", "#FF0000")

}

exchange.SetContractType(ct)

var initPos = _C(exchange.GetPosition)

if (initPos.length != 0) {

throw "Strategy starts with a position!"

}

exchange.SetPrecision(pricePrecision, amountPrecision)

Log("set the pricePrecision", pricePrecision, amountPrecision)

if (!IsVirtual()) {

var recoverTotalEq = _G("totalEq")

if (!recoverTotalEq) {

var currTotalEq = _C(exchange.GetAccount).Balance // equity

if (currTotalEq) {

totalEq = currTotalEq

_G("totalEq", currTotalEq)

} else {

throw "failed to obtain initial interest"

}

} else {

totalEq = recoverTotalEq

}

} else {

totalEq = _C(exchange.GetAccount).Balance

}

while (1) {

if (openPrice == 0) {

// Update account information and calculate profits

var nowAcc = _C(exchange.GetAccount)

nowEq = IsVirtual() ? nowAcc.Balance : nowAcc.Balance // equity

LogProfit(nowEq - totalEq, nowAcc)

var direction = Math.floor((Math.random()*100)+1) // 1~50 , 51~100

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

if (direction > 50) {

// long

openPrice = depth.Bids[1].Price

exchange.SetDirection("buy")

exchange.Buy(Math.abs(openPrice) + slidePrice, amount * ratio)

} else {

// short

openPrice = -depth.Asks[1].Price

exchange.SetDirection("sell")

exchange.Sell(Math.abs(openPrice) - slidePrice, amount * ratio)

}

Log("place", direction > 50 ? "buying order" : "selling order", ", price:", Math.abs(openPrice))

continue

}

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

var pos = _C(exchange.GetPosition)

if (pos.length == 0) {

openPrice = 0

continue

}

// Test for closing the position

while (1) {

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

var stopLossPrice = openPrice > 0 ? Math.abs(openPrice) - stopLoss : Math.abs(openPrice) + stopLoss

var stopProfitPrice = openPrice > 0 ? Math.abs(openPrice) + stopProfit : Math.abs(openPrice) - stopProfit

var winOrLoss = 0 // 1 win , -1 loss

// drawing the line

$.PlotLine("bid", depth.Bids[0].Price)

$.PlotLine("ask", depth.Asks[0].Price)

// stop loss

if (openPrice > 0 && depth.Bids[0].Price < stopLossPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = -1

} else if (openPrice < 0 && depth.Asks[0].Price > stopLossPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = -1

}

// stop profit

if (openPrice > 0 && depth.Bids[0].Price > stopProfitPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = 1

} else if (openPrice < 0 && depth.Asks[0].Price < stopProfitPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = 1

}

// Test the pending orders

Sleep(2000)

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

pos = _C(exchange.GetPosition)

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

} else {

// cancel pending orders

cancelAll()

Sleep(2000)

pos = _C(exchange.GetPosition)

// update the position after cancellation, and check it again

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

}

var tbl = {

"type" : "table",

"title" : "info",

"cols" : ["totalEq", "nowEq", "openPrice", "bid1Price", "ask1Price", "ratio", "pos.length"],

"rows" : [],

}

tbl.rows.push([totalEq, nowEq, Math.abs(openPrice), depth.Bids[0].Price, depth.Asks[0].Price, ratio, pos.length])

tbl.rows.push(["pos", "type", "amount", "price", "--", "--", "--"])

for (var j = 0 ; j < pos.length ; j++) {

tbl.rows.push([j, pos[j].Type, pos[j].Amount, pos[j].Price, "--", "--", "--"])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

}

} else {

// cancel the pending orders

// reset openPrice

cancelAll()

openPrice = 0

}

Sleep(1000)

}

}

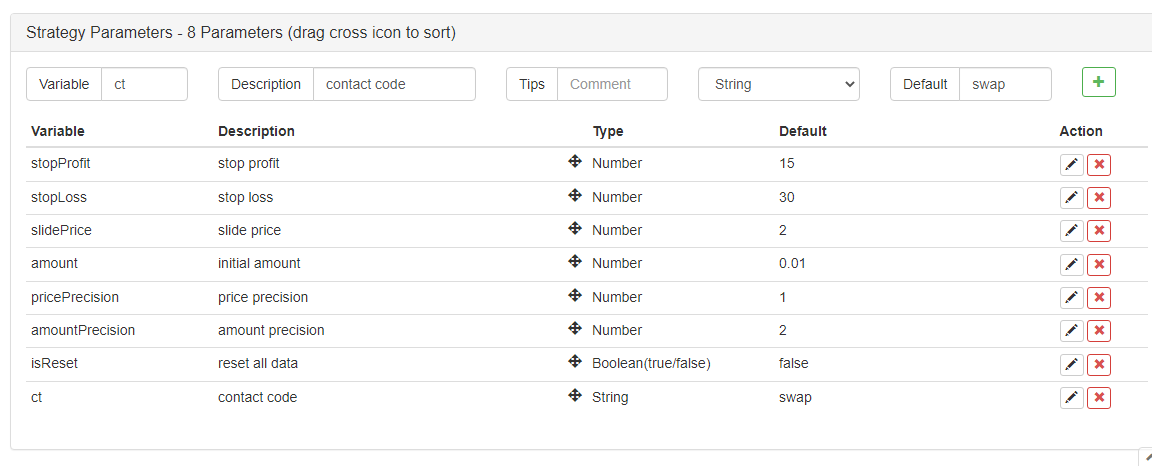

Parameter strategi:

Oh ya! Strategi ini memerlukan nama, mari kita panggil

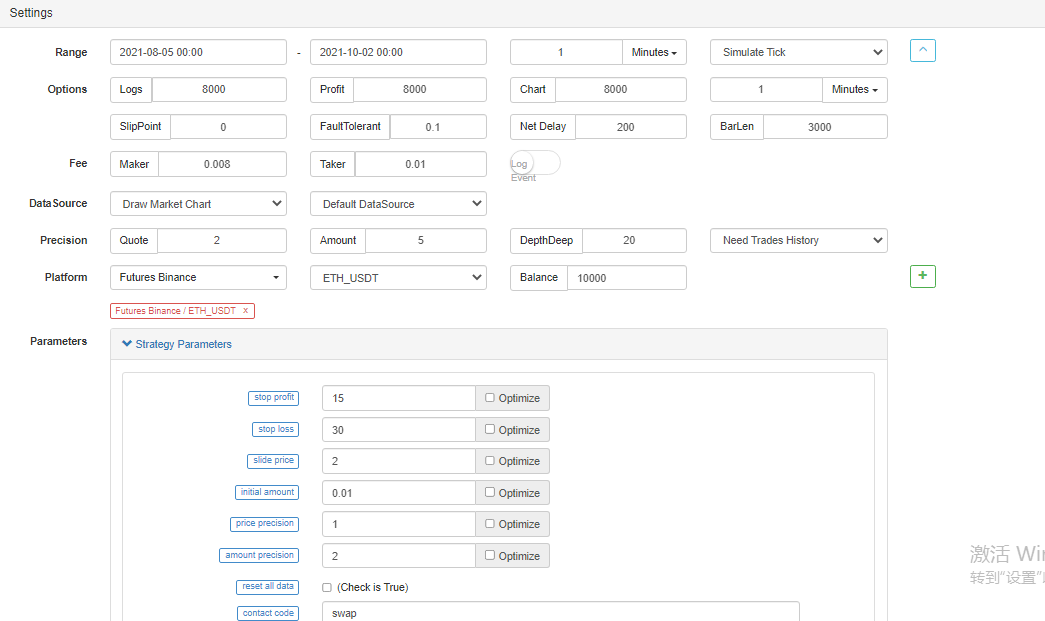

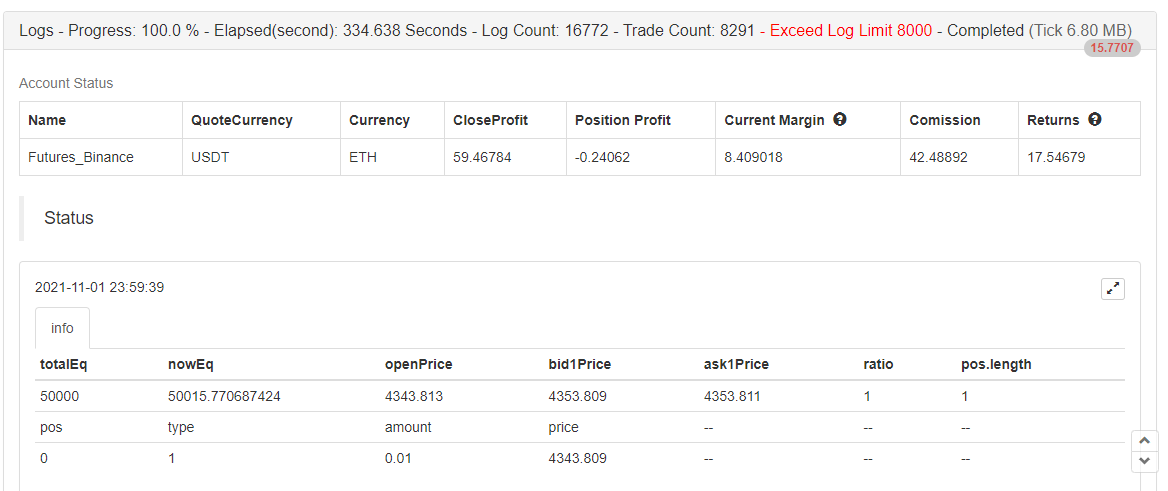

Ujian belakang

Backtesting adalah untuk rujukan sahaja, >_

Ujian belakang telah selesai, tidak ada bug.

Strategi ini digunakan untuk pembelajaran dan rujukan sahaja, jangan menggunakannya dalam bot sebenar!

- Mengukur Analisis Dasar di Pasaran Cryptocurrency: Biarkan Data Bercakap Sendiri!

- Perbincangan mengenai kajian kuantitatif asas dalam lingkaran mata wang - jangan mempercayai guru-guru sihir yang bodoh, data adalah objektif!

- Alat penting dalam bidang transaksi kuantitatif - Pencipta modul pencarian data kuantitatif

- Menguasai Semuanya - Pengenalan kepada FMZ Versi Baru Terminal Dagangan (dengan Kod Sumber Arbitraj TRB)

- Menguasai segala-galanya FMZ versi baru terminal perdagangan pengenalan (tambahan kod sumber TRB suite)

- FMZ Quant: Analisis Contoh Reka Bentuk Keperluan Umum di Pasaran Cryptocurrency (II)

- Bagaimana untuk mengeksploitasi bot jualan tanpa otak dengan strategi frekuensi tinggi dalam 80 baris kod

- FMZ Kuantitatif: Penyelesaian contoh reka bentuk permintaan biasa di pasaran mata wang kripto (II)

- Bagaimana untuk mengeksploitasi robot tanpa otak yang dijual dengan strategi frekuensi tinggi 80 baris kod

- FMZ Quant: Analisis Contoh Reka Bentuk Keperluan Umum di Pasaran Cryptocurrency (I)

- FMZ Kuantitatif: Penyelesaian contoh reka bentuk permintaan biasa di pasaran mata wang kripto