AlphaTradingBot Strategi Dagangan

Gambaran Keseluruhan

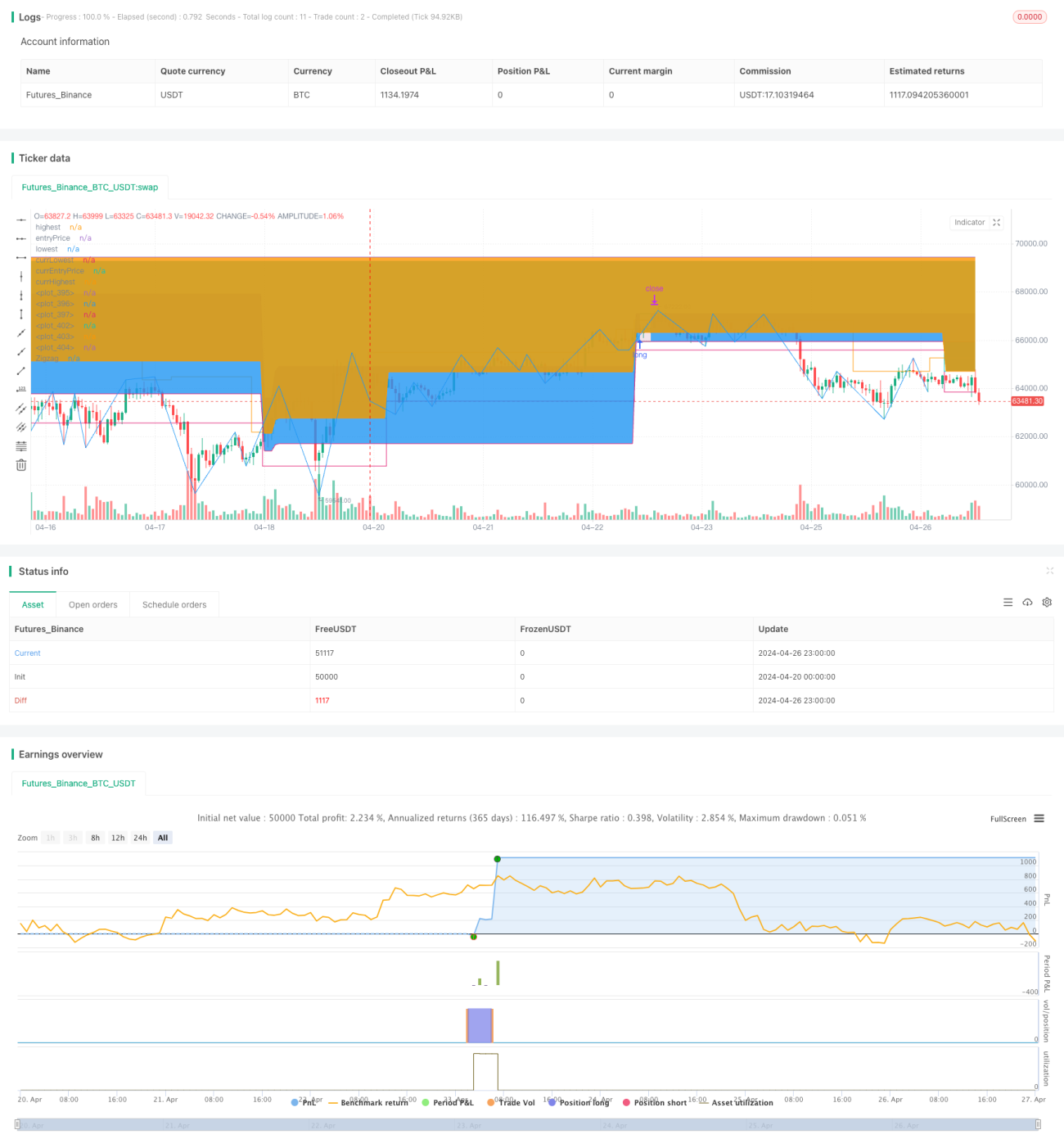

AlphaTradingBot ialah strategi dagangan intra-hari berdasarkan penunjuk Zigzag dan siri Fibonacci. Strategi ini mengenal pasti arah aliran dengan mengesan titik tertinggi (HH) dan titik terendah (LL) pasaran, digabungkan dengan pengembalian semula Fibonacci (Fibonacci retracement) dan pengembangan (Fibonacci expansion) untuk menetapkan titik masuk, ambil untung, dan henti rugi. Strategi ini hanya berjalan dalam julat tarikh yang ditetapkan, boleh mengambil posisi beli (long) dan jual (short) secara berasingan, dan mempunyai keupayaan menangkap arah aliran serta kawalan nisbah untung-rugi yang baik.

Prinsip Strategi

- Kenal pasti titik tertinggi (HH), titik terendah (LL), titik tinggi yang lebih rendah (HL), dan titik rendah yang lebih tinggi (LH) pasaran melalui penunjuk Zigzag.

- Apabila HH berlaku, ia dianggap permulaan arah aliran menaik, dan mula mencari peluang beli; apabila LL berlaku, ia dianggap permulaan arah aliran menurun, dan mula mencari peluang jual.

- Dalam arah aliran menaik, jika HL berlaku, gunakan selang yang dibentuk oleh HL dan LL sebelumnya sebagai zon pengembalian semula Fibonacci untuk posisi beli. Jika harga menembusi paras tertinggi sebelum ini, buka posisi beli di kawasan antara 23.6% hingga 38.2% (boleh ditetapkan) pengembalian semula, henti rugi diletakkan pada pengembalian 61.8%, dan ambil untung dikira berdasarkan nilai RR (boleh ditetapkan).

- Dalam arah aliran menurun, jika LH berlaku, gunakan selang yang dibentuk oleh LH dan HH sebelumnya sebagai zon pengembalian semula Fibonacci untuk posisi jual. Jika harga menembusi paras terendah sebelum ini, buka posisi jual di kawasan antara 61.8% hingga 76.4% (boleh ditetapkan) pengembalian semula, henti rugi diletakkan pada pengembalian 38.2%, dan ambil untung dikira berdasarkan nilai RR (boleh ditetapkan).

- Pengurusan pesanan: Hanya satu pesanan dibuka setiap isyarat sehingga pesanan tersebut ditutup. Jika satu kerugian dagangan mencapai X% (boleh ditetapkan) daripada jumlah akaun, strategi akan berhenti beroperasi.

Analisis Kelebihan

- Keupayaan mengikuti arah aliran yang kuat. Mengenal pasti arah aliran dengan berkesan melalui Zigzag, membolehkan penglibatan pada peringkat awal arah aliran.

- Logik pengembalian semula yang jelas. Menggunakan pengembalian semula Fibonacci untuk menetapkan zon masuk, dan masuk semasa pengembalian arah aliran, kadar kemenangan agak tinggi.

- Risiko terkawal. Mengawal risiko setiap dagangan dengan menetapkan nisbah kerugian maksimum setiap dagangan, dan sistem henti rugi yang ketat memastikan jumlah risiko terkawal.

- Nisbah untung-rugi boleh dioptimumkan. Boleh melaraskan nilai RR untuk mengoptimumkan nisbah untung-rugi strategi mengikut ciri pasaran dan keutamaan peribadi.

Analisis Risiko

- Dagangan yang kerap. Oleh kerana sensitiviti Zigzag yang tinggi, isyarat mungkin kerap dihasilkan, menyebabkan perdagangan berlebihan.

- Penangkapan arah aliran yang tidak tepat. Arah aliran yang dinilai oleh Zigzag mungkin masih menyimpang, menyebabkan masa masuk yang kurang ideal.

- Prestasi lemah dalam pasaran sideway. Dalam pasaran yang tidak menentu (oscillating), strategi ini mungkin menghasilkan lebih banyak dagangan yang rugi.

- Tempoh operasi terhad. Strategi hanya berjalan dalam julat tarikh yang ditetapkan, mungkin terlepas sebahagian daripada pergerakan pasaran.

Arah Pengoptimuman

- Memperkenalkan lebih banyak penunjuk teknikal, seperti MA, MACD, dan lain-lain, untuk meningkatkan ketepatan penentuan arah aliran.

- Mengoptimumkan pengurusan kedudukan, seperti melaraskan saiz kedudukan secara dinamik berdasarkan ATR dan penunjuk lain.

- Mengoptimumkan logik ambil untung dan henti rugi, seperti melaraskan tahap henti rugi secara dinamik berdasarkan turun naik pasaran.

- Memperkenalkan penunjuk sentimen pasaran, untuk mengelakkan masuk ketika pasaran terlalu optimis atau pesimis.

- Melonggarkan sekatan tarikh untuk meningkatkan kebolehgunaan strategi.

Kesimpulan

AlphaTradingBot ialah strategi intra-hari yang mengikuti arah aliran berdasarkan penunjuk zigzag dan pengembalian semula Fibonacci. Ia menilai arah aliran melalui titik tinggi dan rendah, dan masuk semasa pengembalian semula arah aliran untuk mengejar kadar kemenangan dan nisbah untung-rugi yang lebih tinggi. Kelebihan strategi ini terletak pada keupayaan menangkap arah aliran yang kuat, logik pengembalian semula yang jelas, dan risiko yang boleh diukur, tetapi pada masa yang sama, ia juga mempunyai risiko seperti dagangan berlebihan, penyelewengan dalam penilaian arah aliran, dan prestasi lemah dalam pasaran sideway. Pada masa hadapan, strategi ini boleh dioptimumkan dari segi penunjuk teknikal, pengurusan kedudukan, ambil untung dan henti rugi, sentimen pasaran, dan lain-lain, untuk meningkatkan kestabilan dan keuntungan strategi.

- 1