Negociação Quantitativa de Criptomoedas para iniciantes - Levá-lo mais perto da Criptomoeda Quantitativa (5)

Autora:Lydia., Criado: 2022-08-03 16:08:50, Atualizado: 2023-09-21 21:07:02

No artigo anterior, explicamos a análise lógica de negociação de uma estratégia de grade simples.

-

Análise da lógica de negociação Como mencionamos no artigo anterior, você pode desencadear uma ação comercial atravessando cada linha da grade e julgando a passagem do preço atual acima ou abaixo.

O primeiro detalhe que temos que considerar é o projeto da grade infinita.

createNetEsta função gera uma estrutura de dados de grade com um número finito de linhas de grade. Então, e se o preço vai além dos limites desta estrutura de dados de grade (além da linha de grade superior onde o preço é o mais alto, e a linha de grade inferior onde o preço é o mais baixo) quando a estratégia está sendo executada? Então precisamos adicionar um mecanismo de extensão à estrutura de dados da grade primeiro.Vamos começar a escrever a função principal da estratégia, que é o código onde a estratégia começa a ser executada

var diff = 50 // Global variables and grid spacing can be designed as parameters for easy explanation. We write this parameter into the code. function main() { // After the real bot starts running, execute the strategy code from here var ticker = _C(exchange.GetTicker) // To get the latest market data ticker, please refer to the FMZ API documentation for the structure of the ticker data: https://www.fmz.com/api#ticker var net = createNet(ticker.Last, diff) // The function we designed in the previous article to construct the grid data structure initially, here we construct a grid data structure net while (true) { // Then the program logic enters this while infinite loop, and the strategy execution will continue to execute the code within the {} symbol here. ticker = _C(exchange.GetTicker) // The first line of the infinite loop code section, get the latest market data and update it to the ticker variable // Check the grid range while (ticker.Last >= net[net.length - 1].price) { net.push({ buy : false, sell : false, price : net[net.length - 1].price + diff, }) } while (ticker.Last <= net[0].price) { var price = net[0].price - diff if (price <= 0) { break } net.unshift({ buy : false, sell : false, price : price, }) } // There are other codes... } }Para tornar a estrutura de dados de rede extensivel, é necessário este código (extraído do código acima):

// Check the grid range while (ticker.Last >= net[net.length - 1].price) { // If the price exceeds the grid line of the highest price of the grid net.push({ // Just add a new grid line after the grid line with the highest price of the grid buy : false, // Initialize sell marker sell : false, // Initialize buy marker price : net[net.length - 1].price + diff, // dd a grid spacing to the previous highest price }) } while (ticker.Last <= net[0].price) { // If the price is lower than the grid line of the lowest price of the grid var price = net[0].price - diff // Different from adding upwards, it should be noted that the price of adding new grid lines downwards cannot be less than or equal to 0, so it is necessary to judge here if (price <= 0) { // Less than or equal to 0 will not be added, jump out of this loop break } net.unshift({ // Add a new grid line just before the grid line with the lowest price of the grid buy : false, sell : false, price : price, }) }O próximo passo é considerar como implementar especificamente o gatilho de negociação.

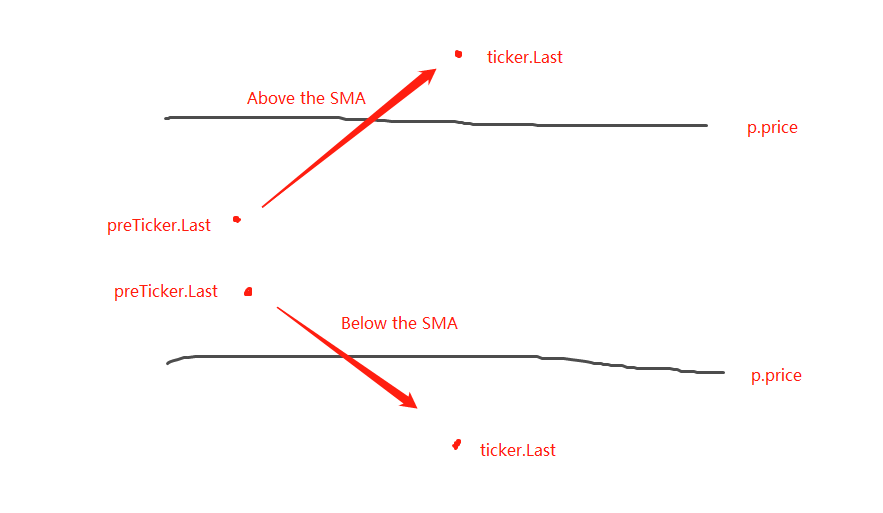

var diff = 50 var amount = 0.002 // Add a global variable, which can also be designed as a parameter. Of course, for the sake of simplicity, we also write it in the strategy code. // This parameter controls the trade volume each time a trade is triggered on the grid line function main() { var ticker = _C(exchange.GetTicker) var net = createNet(ticker.Last, diff) var preTicker = ticker // Before the main loop (fixed loop) starts, set a variable to record the last market data while (true) { ticker = _C(exchange.GetTicker) // Check the grid range while (ticker.Last >= net[net.length - 1].price) { net.push({ buy : false, sell : false, price : net[net.length - 1].price + diff, }) } while (ticker.Last <= net[0].price) { var price = net[0].price - diff if (price <= 0) { break } net.unshift({ buy : false, sell : false, price : price, }) } // Retrieve grid for (var i = 0 ; i < net.length ; i++) { // Iterate over all grid lines in the grid data structure var p = net[i] if (preTicker.Last < p.price && ticker.Last > p.price) { // Above the SMA, sell, the current node has already traded, regardless of SELL BUY, it will no longer be traded if (i != 0) { var downP = net[i - 1] if (downP.buy) { exchange.Sell(-1, amount, ticker) downP.buy = false p.sell = false continue } } if (!p.sell && !p.buy) { exchange.Sell(-1, amount, ticker) p.sell = true } } else if (preTicker.Last > p.price && ticker.Last < p.price) { // Below the SMA, buy if (i != net.length - 1) { var upP = net[i + 1] if (upP.sell) { exchange.Buy(-1, amount * ticker.Last, ticker) upP.sell = false p.buy = false continue } } if (!p.buy && !p.sell) { exchange.Buy(-1, amount * ticker.Last, ticker) p.buy = true } } } preTicker = ticker // Record the current market data in preTicker, and in the next cycle, use it as a comparison between the "previous" market data and the latest one to judge whether to be above the SMA or below the SMA. Sleep(500) } }Pode-se observar que:

- Condição para a travessia acima das linhas da grade:

preTicker.Last < p.price && ticker.Last > p.price - Condição para a travessia abaixo das linhas da grade:

preTicker.Last > p.price && ticker.Last < p.price

Isto é o que dissemos no post anterior:

- Condição para a travessia acima das linhas da grade:

Julgar se deve estar acima ou abaixo da SMA é apenas o primeiro passo para julgar se uma ordem pode ser colocada, e também é necessário julgar as marcas nos dados da linha da rede.

Se estiver acima da SMA, julga-se que o preço é menor do que a linha de rede atual e a marca de compra na linha de rede mais próxima.

Depois de julgar as condições, se não houver gatilho, continue a julgar. Se as marcas de compra/venda na linha da grade atual forem ambas falsas, isso significa que a linha da grade atual pode ser negociada. Uma vez que está acima da SMA, realizaremos uma operação de venda aqui. Após a execução, marque a marca de venda da linha da grade atual como verdadeira.

A lógica de processamento é a mesma para estar abaixo da SMA (esquerda para os iniciantes a pensar sobre aqui).

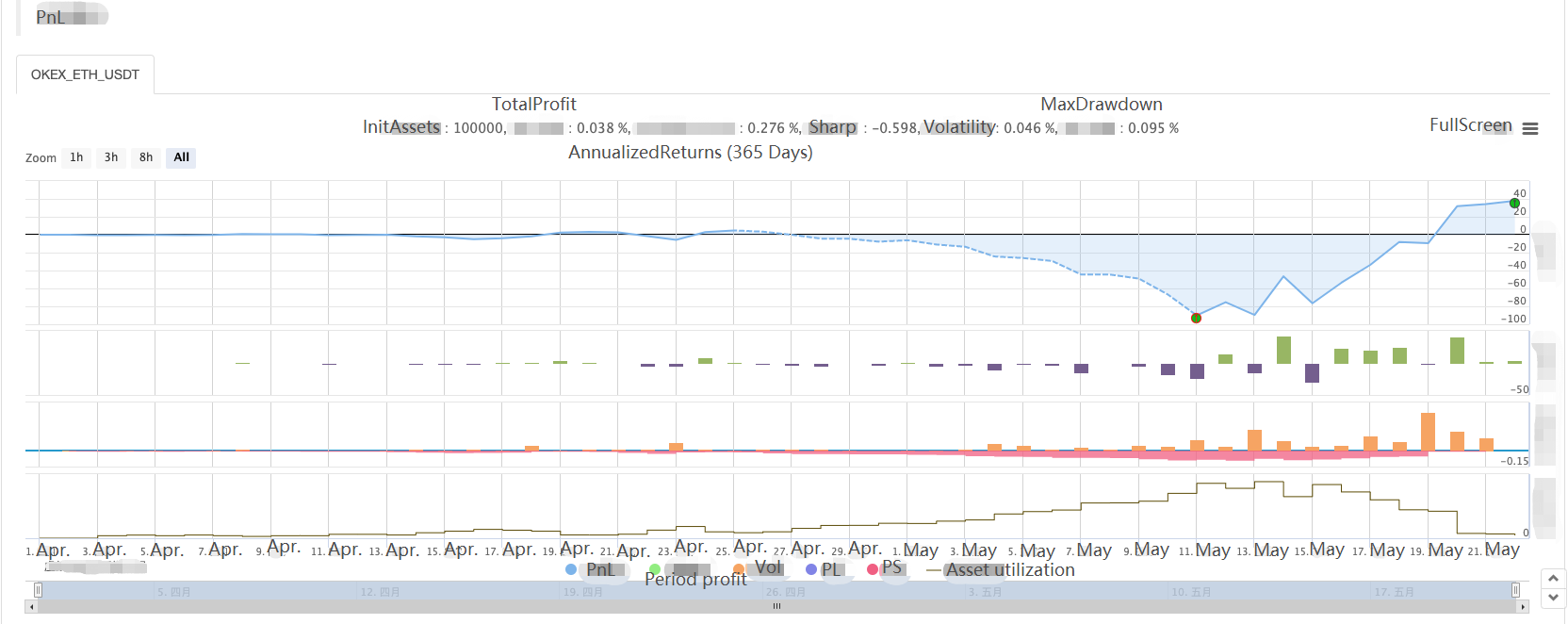

Backtesting da estratégia completa

A fim de ver alguns dados durante backtesting, uma funçãoshowTblé escrito para exibir os dados.

function showTbl(arr) {

var tbl = {

type : "table",

title : "grid",

cols : ["grid information"],

rows : []

}

var arrReverse = arr.slice(0).reverse()

_.each(arrReverse, function(ele) {

var color = ""

if (ele.buy) {

color = "#FF0000"

} else if (ele.sell) {

color = "#00FF00"

}

tbl.rows.push([JSON.stringify(ele) + color])

})

LogStatus(_D(), "\n`" + JSON.stringify(tbl) + "`", "\n account Information:", exchange.GetAccount())

}

Código completo da estratégia:

/*backtest

start: 2021-04-01 22:00:00

end: 2021-05-22 00:00:00

period: 1d

basePeriod: 1m

exchanges: [{"eid":"OKEX","currency":"ETH_USDT","balance":100000}]

*/

var diff = 50

var amount = 0.002

function createNet(begin, diff) {

var oneSideNums = 10

var up = []

var down = []

for (var i = 0 ; i < oneSideNums ; i++) {

var upObj = {

buy : false,

sell : false,

price : begin + diff / 2 + i * diff,

}

up.push(upObj)

var j = (oneSideNums - 1) - i

var downObj = {

buy : false,

sell : false,

price : begin - diff / 2 - j * diff,

}

if (downObj.price <= 0) { // The price cannot be less than or equal to 0

continue

}

down.push(downObj)

}

return down.concat(up)

}

function showTbl(arr) {

var tbl = {

type : "table",

title : "grid",

cols : ["grid Information"],

rows : []

}

var arrReverse = arr.slice(0).reverse()

_.each(arrReverse, function(ele) {

var color = ""

if (ele.buy) {

color = "#FF0000"

} else if (ele.sell) {

color = "#00FF00"

}

tbl.rows.push([JSON.stringify(ele) + color])

})

LogStatus(_D(), "\n`" + JSON.stringify(tbl) + "`", "\n account Information:", exchange.GetAccount())

}

function main() {

var ticker = _C(exchange.GetTicker)

var net = createNet(ticker.Last, diff)

var preTicker = ticker

while (true) {

ticker = _C(exchange.GetTicker)

// Check the grid range

while (ticker.Last >= net[net.length - 1].price) {

net.push({

buy : false,

sell : false,

price : net[net.length - 1].price + diff,

})

}

while (ticker.Last <= net[0].price) {

var price = net[0].price - diff

if (price <= 0) {

break

}

net.unshift({

buy : false,

sell : false,

price : price,

})

}

// Retrieve grid

for (var i = 0 ; i < net.length ; i++) {

var p = net[i]

if (preTicker.Last < p.price && ticker.Last > p.price) { // Being above the SMA, sell, the current node has already traded, regardless of SELL BUY, it will no longer be traded

if (i != 0) {

var downP = net[i - 1]

if (downP.buy) {

exchange.Sell(-1, amount, ticker)

downP.buy = false

p.sell = false

continue

}

}

if (!p.sell && !p.buy) {

exchange.Sell(-1, amount, ticker)

p.sell = true

}

} else if (preTicker.Last > p.price && ticker.Last < p.price) { // Being below the SMA, buy

if (i != net.length - 1) {

var upP = net[i + 1]

if (upP.sell) {

exchange.Buy(-1, amount * ticker.Last, ticker)

upP.sell = false

p.buy = false

continue

}

}

if (!p.buy && !p.sell) {

exchange.Buy(-1, amount * ticker.Last, ticker)

p.buy = true

}

}

}

showTbl(net)

preTicker = ticker

Sleep(500)

}

}

Estratégia de backtesting:

Podemos ver as características da estratégia da rede, quando há um mercado em tendência, haverá uma grande perda flutuante, e o lucro vai se recuperar em um mercado volátil.

Por conseguinte, a estratégia de rede não é isenta de risco. A estratégia spot ainda pode ser

- Quantificar a análise fundamental no mercado de criptomoedas: deixe os dados falarem por si mesmos!

- A pesquisa quantitativa básica do círculo monetário - deixe de acreditar em todos os professores de matemática loucos, os dados são objetivos!

- Uma ferramenta indispensável no campo da transação quantitativa - inventor do módulo de exploração de dados quantitativos

- Dominar tudo - Introdução ao FMZ Nova versão do Terminal de Negociação (com TRB Arbitrage Source Code)

- Conheça tudo sobre a nova versão do terminal de negociação da FMZ

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (II)

- Como explorar robôs de venda sem cérebro com uma estratégia de alta frequência em 80 linhas de código

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (II)

- Como usar estratégias de 80 linhas de código de alta frequência para explorar robôs sem cérebro para venda

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (I)

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (I)