Estratégia de ordem pendente equilibrada (estratégia de ensino)

Autora:Lydia., Criado: 2022-12-19 17:19:44, Atualizado: 2023-09-20 10:01:27

Estratégia de ordem pendente equilibrada (estratégia de ensino)

A essência da estratégia descrita neste artigo é uma estratégia de balanço dinâmico, ou seja, o valor da moeda do saldo é sempre igual ao valor da moeda de avaliação.

-

Encapsulamento lógico da estratégia Encapsular a lógica da estratégia com alguns dados e variáveis de tag no tempo de execução (encapsulado como objetos).

-

Código para inicialização do processamento de estratégias A informação inicial da conta é registrada na execução inicial para o cálculo de lucro.

-

Código para o processamento de interações de estratégia É concebido um simples processamento interativo de pausa e retomada.

-

Código para o cálculo do lucro da estratégia O método de cálculo padrão de moeda é utilizado para calcular o lucro.

-

Mecanismo de persistência dos dados chave na estratégia Projeto de mecanismos de recuperação de dados.

-

Código para exibição das informações de processamento da estratégia Exibição de dados da barra de estado.

Código de estratégia

var Shannon = {

// member

e : exchanges[0],

arrPlanOrders : [],

distance : BalanceDistance,

account : null,

ticker : null,

initAccount : null,

isAskPending : false,

isBidPending : false,

// function

CancelAllOrders : function (e) {

while(true) {

var orders = _C(e.GetOrders)

if(orders.length == 0) {

return

}

Sleep(500)

for(var i = 0; i < orders.length; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

},

Balance : function () {

if (this.arrPlanOrders.length == 0) {

this.CancelAllOrders(this.e)

var acc = _C(this.e.GetAccount)

this.account = acc

var askPendingPrice = (this.distance + acc.Balance) / acc.Stocks

var bidPendingPrice = (acc.Balance - this.distance) / acc.Stocks

var askPendingAmount = this.distance / 2 / askPendingPrice

var bidPendingAmount = this.distance / 2 / bidPendingPrice

this.arrPlanOrders.push({tradeType : "ask", price : askPendingPrice, amount : askPendingAmount})

this.arrPlanOrders.push({tradeType : "bid", price : bidPendingPrice, amount : bidPendingAmount})

} else if(this.isAskPending == false && this.isBidPending == false) {

for(var i = 0; i < this.arrPlanOrders.length; i++) {

var tradeFun = this.arrPlanOrders[i].tradeType == "ask" ? this.e.Sell : this.e.Buy

var id = tradeFun(this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount)

if(id) {

this.isAskPending = this.arrPlanOrders[i].tradeType == "ask" ? true : this.isAskPending

this.isBidPending = this.arrPlanOrders[i].tradeType == "bid" ? true : this.isBidPending

} else {

Log("Pending order failed, clear!")

this.CancelAllOrders(this.e)

return

}

}

}

if(this.isBidPending || this.isAskPending) {

var orders = _C(this.e.GetOrders)

Sleep(1000)

var ticker = _C(this.e.GetTicker)

this.ticker = ticker

if(this.isAskPending) {

var isFoundAsk = false

for (var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_SELL) {

isFoundAsk = true

}

}

if(!isFoundAsk) {

Log("Selling order filled, cancel the order, reset")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

if(this.isBidPending) {

var isFoundBid = false

for(var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_BUY) {

isFoundBid = true

}

}

if(!isFoundBid) {

Log("Buying order filled, cancel the order, reset")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

}

},

ShowTab : function() {

var tblPlanOrders = {

type : "table",

title : "Plan pending orders",

cols : ["direction", "price", "amount"],

rows : []

}

for(var i = 0; i < this.arrPlanOrders.length; i++) {

tblPlanOrders.rows.push([this.arrPlanOrders[i].tradeType, this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount])

}

var tblAcc = {

type : "table",

title : "Account information",

cols : ["type", "Stocks", "FrozenStocks", "Balance", "FrozenBalance"],

rows : []

}

tblAcc.rows.push(["Initial", this.initAccount.Stocks, this.initAccount.FrozenStocks, this.initAccount.Balance, this.initAccount.FrozenBalance])

tblAcc.rows.push(["This", this.account.Stocks, this.account.FrozenStocks, this.account.Balance, this.account.FrozenBalance])

return "Time:" + _D() + "\n `" + JSON.stringify([tblPlanOrders, tblAcc]) + "`" + "\n" + "ticker:" + JSON.stringify(this.ticker)

},

CalcProfit : function(ticker) {

var acc = _C(this.e.GetAccount)

this.account = acc

return (this.account.Balance - this.initAccount.Balance) + (this.account.Stocks - this.initAccount.Stocks) * ticker.Last

},

Init : function() {

this.initAccount = _C(this.e.GetAccount)

if(IsReset) {

var acc = _G("account")

if(acc) {

this.initAccount = acc

} else {

Log("Failed to restore initial account information! Running in initial state!")

_G("account", this.initAccount)

}

} else {

_G("account", this.initAccount)

LogReset(1)

LogProfitReset()

}

},

Exit : function() {

Log("Cancel all pending orders before stopping...")

this.CancelAllOrders(this.e)

}

}

function main() {

// Initialization

Shannon.Init()

// Main loop

while(true) {

Shannon.Balance()

LogStatus(Shannon.ShowTab())

// Interaction

var cmd = GetCommand()

if(cmd) {

if(cmd == "stop") {

while(true) {

LogStatus("Pause", Shannon.ShowTab())

cmd = GetCommand()

if(cmd) {

if(cmd == "continue") {

break

}

}

Sleep(1000)

}

}

}

Sleep(5000)

}

}

function onexit() {

Shannon.Exit()

}

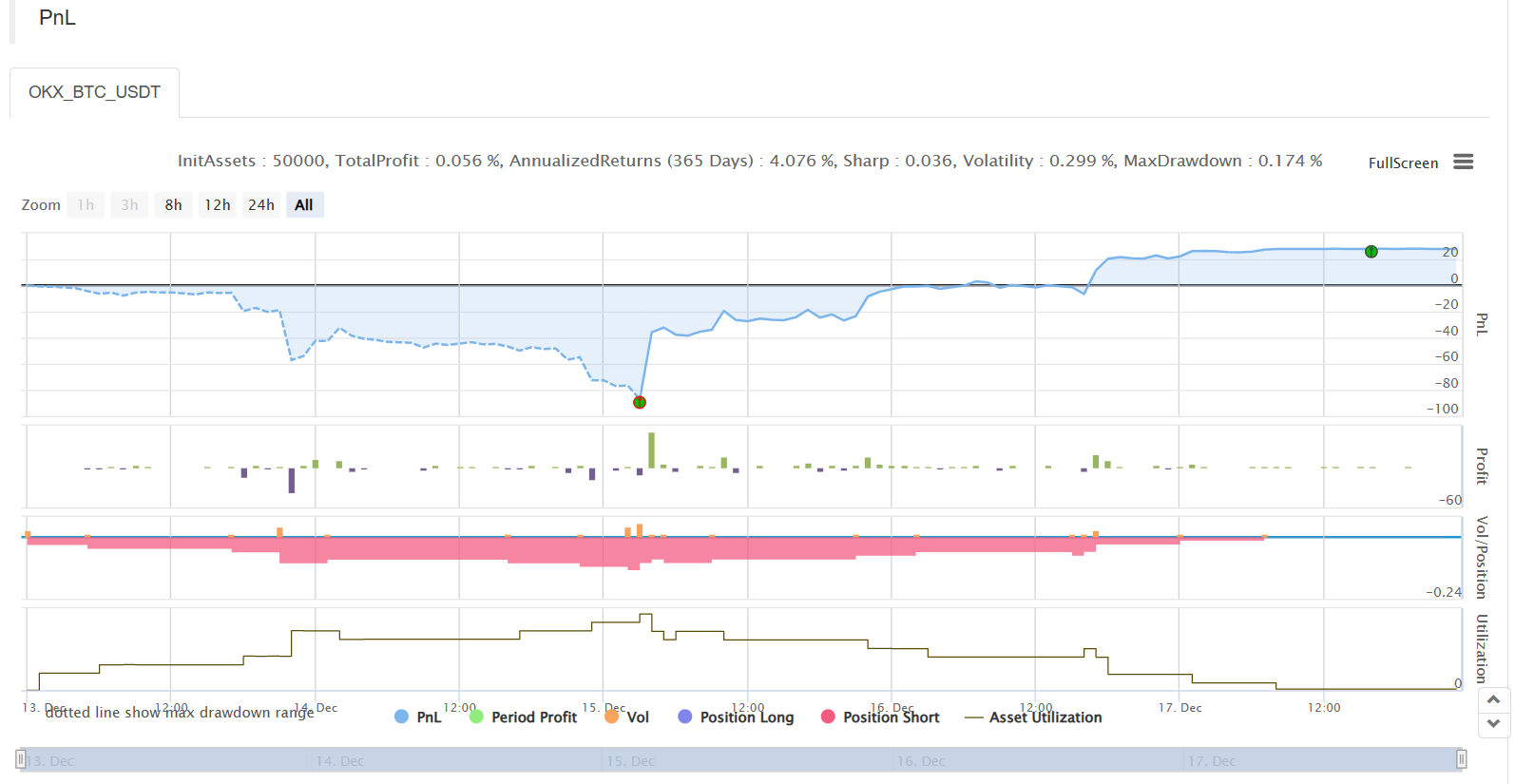

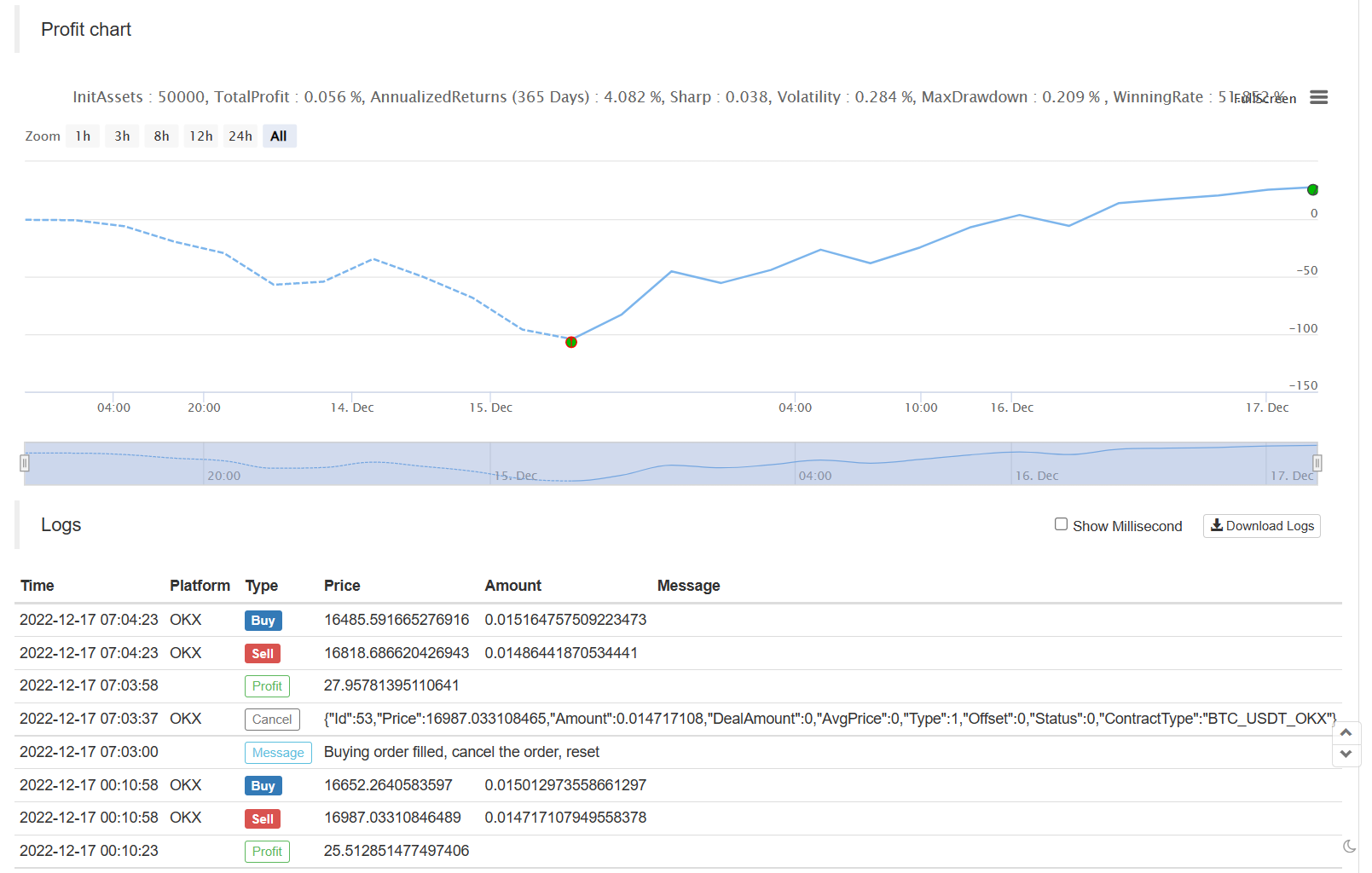

Testes de retrocesso

Optimização e extensão

- Alguns mercados têm preços limitados em ordens pendentes, então a ordem pode não ser efetivamente colocada.

- Adicione a negociação de futuros.

- Expandir uma versão multi-espécie e multi-intercâmbio.

As estratégias são apenas para fins educacionais e devem ser usadas com cautela na negociação de bots reais. Endereço estratégico:https://www.fmz.com/strategy/225746

- Quantificar a análise fundamental no mercado de criptomoedas: deixe os dados falarem por si mesmos!

- A pesquisa quantitativa básica do círculo monetário - deixe de acreditar em todos os professores de matemática loucos, os dados são objetivos!

- Uma ferramenta indispensável no campo da transação quantitativa - inventor do módulo de exploração de dados quantitativos

- Dominar tudo - Introdução ao FMZ Nova versão do Terminal de Negociação (com TRB Arbitrage Source Code)

- Conheça tudo sobre a nova versão do terminal de negociação da FMZ

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (II)

- Como explorar robôs de venda sem cérebro com uma estratégia de alta frequência em 80 linhas de código

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (II)

- Como usar estratégias de 80 linhas de código de alta frequência para explorar robôs sem cérebro para venda

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (I)

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (I)