Торговая стратегия AlphaTradingBot

Обзор

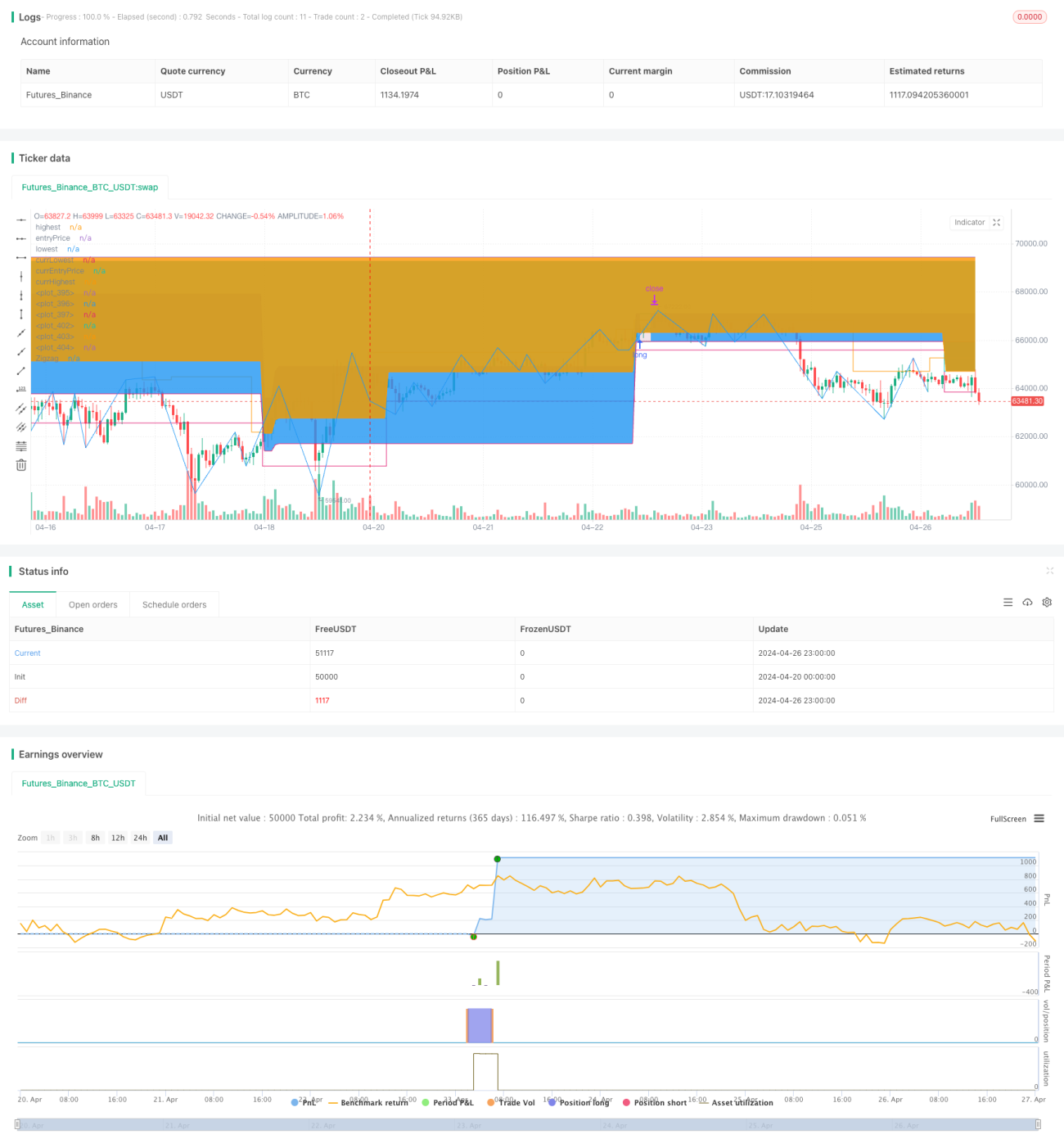

AlphaTradingBot — это внутридневная торговая стратегия, основанная на индикаторе Zigzag и числах Фибоначчи. Стратегия определяет тренд, выявляя максимумы (HH) и минимумы (LL) рынка, и использует уровни коррекции и расширения Фибоначчи для установки точек входа, тейк-профита и стоп-лосса. Стратегия работает только в заданном диапазоне дат, может открывать как длинные, так и короткие позиции, обладает определённой способностью улавливать тренды и контролировать соотношение прибыли и риска.

Принцип стратегии

- С помощью индикатора Zigzag идентифицируются максимумы (HH), минимумы (LL), более высокие минимумы (HL) и более низкие максимумы (LH) рынка.

- При появлении HH считается, что начинается восходящий тренд, и начинается поиск возможностей для открытия длинных позиций; при появлении LL считается, что начинается нисходящий тренд, и начинается поиск возможностей для открытия коротких позиций.

- В восходящем тренде при появлении HL интервал между HL и предыдущим LL используется как зона коррекции Фибоначчи для длинных позиций. Если цена пробивает предыдущий максимум, то открывается длинная позиция в зоне коррекции 23,6%–38,2% (настраивается), стоп-лосс устанавливается на уровне коррекции 61,8%, тейк-профит рассчитывается на основе значения RR (настраивается).

- В нисходящем тренде при появлении LH интервал между LH и предыдущим HH используется как зона коррекции Фибоначчи для коротких позиций. Если цена пробивает предыдущий минимум, то открывается короткая позиция в зоне коррекции 61,8%–76,4% (настраивается), стоп-лосс устанавливается на уровне коррекции 38,2%, тейк-профит рассчитывается на основе значения RR (настраивается).

- Управление ордерами: на каждый сигнал открывается только одна позиция до её закрытия. Если убыток по одной позиции достигает X% (настраивается) от общего капитала счёта, стратегия прекращает работу.

Анализ преимуществ

- Высокая способность следовать за трендом. Эффективное выявление тренда с помощью Zigzag позволяет входить в него на ранних стадиях.

- Чёткая логика коррекции. Использование уровней коррекции Фибоначчи для установки зон входа позволяет входить во время коррекции тренда, что даёт относительно высокую вероятность успеха.

- Контролируемый риск. Установка максимального процента убытка на одну сделку позволяет контролировать риск каждой сделки, а строгая система стоп-лоссов обеспечивает контроль общего риска.

- Оптимизация соотношения прибыли и риска. В зависимости от рыночных особенностей и личных предпочтений можно корректировать значение RR для оптимизации соотношения прибыли и риска стратегии.

Анализ рисков

- Частая торговля. Из-за высокой чувствительности Zigzag сигналы могут генерироваться часто, что приводит к чрезмерной торговле.

- Неточное определение тренда. Определение тренда с помощью Zigzag может иметь погрешности, что приводит к неидеальным моментам входа.

- Плохая работа в боковом рынке. В условиях бокового рынка стратегия может генерировать много убыточных сделок.

- Ограниченный период работы. Стратегия работает только в заданном диапазоне дат, что может привести к пропуску части движений рынка.

Направления оптимизации

- Внедрение дополнительных технических индикаторов, таких как MA, MACD и др., для повышения точности определения тренда.

- Оптимизация управления позициями, например, динамическая корректировка объёма позиции на основе ATR и других индикаторов.

- Оптимизация логики тейк-профита и стоп-лосса, например, динамическая корректировка стоп-лосса на основе волатильности рынка.

- Внедрение индикаторов рыночных настроений, чтобы избегать входа в периоды крайнего оптимизма или пессимизма.

- Расширение временных ограничений для повышения универсальности стратегии.

Заключение

AlphaTradingBot — это внутридневная трендовая стратегия, основанная на индикаторе Zigzag и уровнях коррекции Фибоначчи. Она определяет тренд по максимумам и минимумам и входит в рынок во время коррекции тренда, стремясь к более высокой вероятности успеха и лучшему соотношению прибыли и риска. Преимущества стратегии: высокая способность улавливать тренд, чёткая логика коррекции, измеримый риск. Однако существуют риски: чрезмерная торговля, ошибки в определении тренда, плохая работа в боковом рынке. В будущем стратегию можно оптимизировать по таким направлениям, как технические индикаторы, управление позициями, тейк-профит и стоп-лосс, рыночные настроения, чтобы повысить её устойчивость и прибыльность.

- 1