Мультиравновесная стратегия следования за трендом и разворота цен

Обзор стратегии

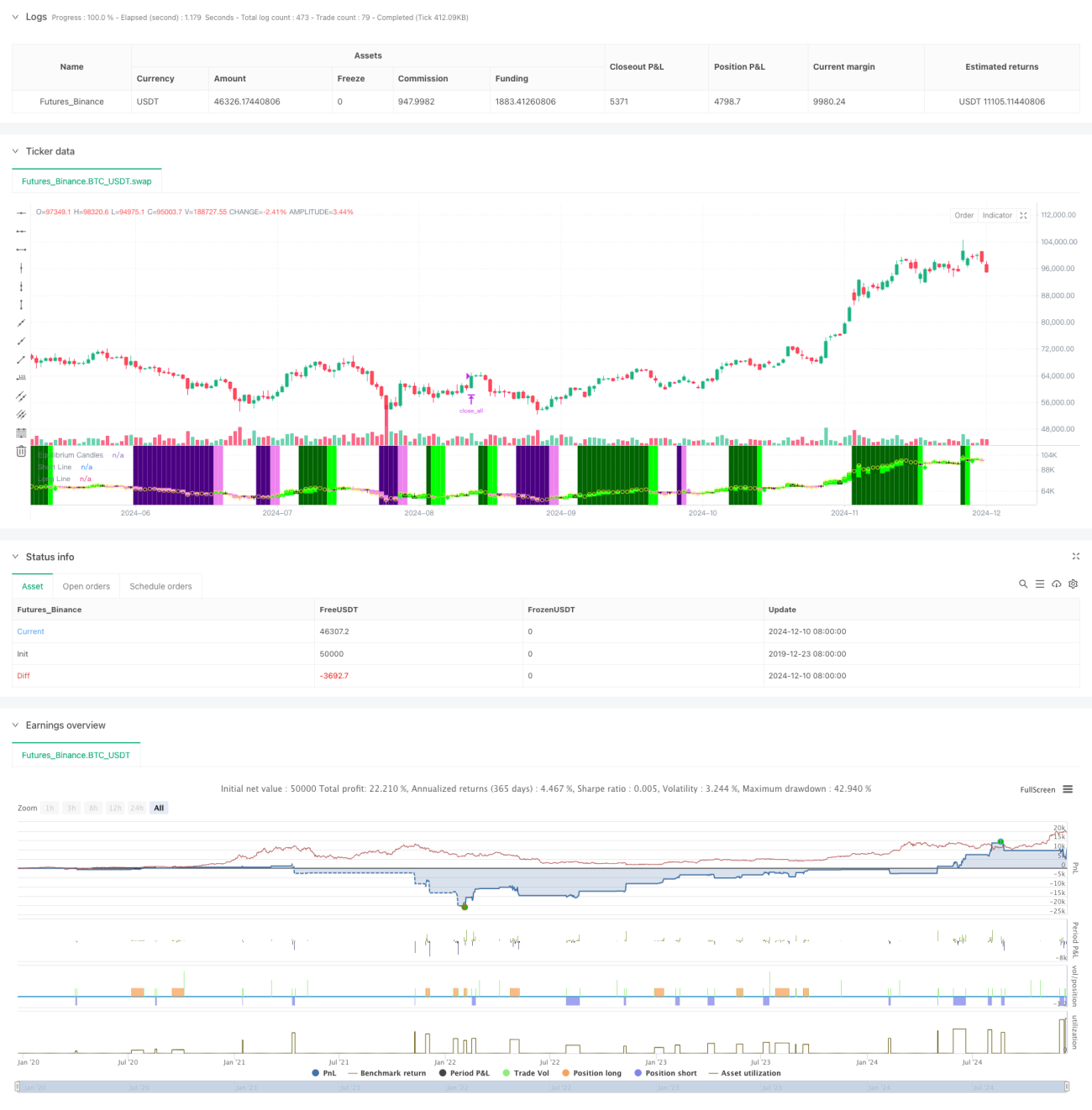

Данная стратегия представляет собой систему следящего за трендом и разворотной торговли, основанную на точке ценового равновесия. Она определяет равновесную цену как среднее значение между максимумом и минимумом за последние X свечей, а направление тренда оценивается по положению цены закрытия относительно равновесной цены. Если цена последовательно удерживается на одной стороне равновесной цены в течение заданного количества свечей, система фиксирует формирование тренда. При первом откате (пробое равновесной цены) система ищет точку входа. Стратегия может быть настроена на режим следования за трендом или разворотной торговли.

Принцип работы стратегии

- Расчёт равновесной цены: используется средняя точка между максимумом и минимумом за последние X свечей – аналогично расчёту линии базы в графике Ишимоку.

- Определение тренда: если цена находится на одной стороне равновесной цены непрерывно X свечей (по умолчанию 7), тренд считается сформированным.

- Сигнал на вход: формируется при первом откате после установления тренда (пробой равновесной цены).

- Стоп-лосс и тейк-профит: используются 60% квантиль ATR для динамической корректировки расстояний до стоп-лосса и тейк-профита, что обеспечивает гибкость контроля риска.

- Защита от сильных колебаний: когда цена отклоняется от равновесной точки более чем на заданный множитель ATR, система автоматически закрывает позицию, чтобы предотвратить сильную просадку.

Преимущества стратегии

- Высокая адаптивность: позволяет гибко переключаться между режимами следования за трендом и разворотной торговли в зависимости от рыночных условий.

- Надёжный контроль рисков: используются динамический стоп-лосс на основе ATR и механизм защиты от сильных колебаний.

- Чёткие сигналы: торговые сигналы понятны и не требуют комбинации сложных технических индикаторов.

- Хорошая визуализация: цветные свечи и фон обеспечивают наглядное представление состояния рынка.

- Удобство автоматизации: легко интегрируется с торговыми платформами, такими как MT5, для автоматической торговли.

Риски стратегии

- Риск боковика: в условиях бокового рынка может генерировать частые ложные сигналы.

- Влияние проскальзывания: при резких колебаниях возможно значительное проскальзывание.

- Чувствительность к параметрам: ключевые параметры, такие как период расчёта равновесия и период определения тренда, требуют тщательной оптимизации для разных рынков.

- Риск смены режима: период перехода рынка от трендового к боковому может привести к крупным просадкам.

Направления оптимизации стратегии

- Определение рыночных условий: добавить модуль оценки рыночной среды для динамической настройки параметров стратегии в разных условиях.

- Фильтрация сигналов: рассмотреть возможность включения вспомогательных индикаторов, таких как объём и волатильность, для фильтрации ложных сигналов.

- Управление позицией: внедрить более сложные механизмы управления позицией, например, динамическую корректировку на основе волатильности.

- Множественные таймфреймы: объединить сигналы с нескольких таймфреймов для повышения точности торговли.

- Оптимизация торговых издержек: адаптировать моменты входа и выхода с учётом стоимости торговли для разных инструментов.

Заключение

Это хорошо продуманная трендовая торговая система, предлагающая чёткую торговую логику на основе ключевой концепции равновесной цены. Главная особенность стратегии – высокая гибкость: она может применяться как для следования за трендом, так и для разворотной торговли, при этом обладает надёжным механизмом контроля рисков. Хотя в определённых рыночных условиях она может сталкиваться с трудностями, благодаря постоянной оптимизации и гибкой настройке стратегия способна демонстрировать стабильную эффективность в различных рыночных средах.

- 1