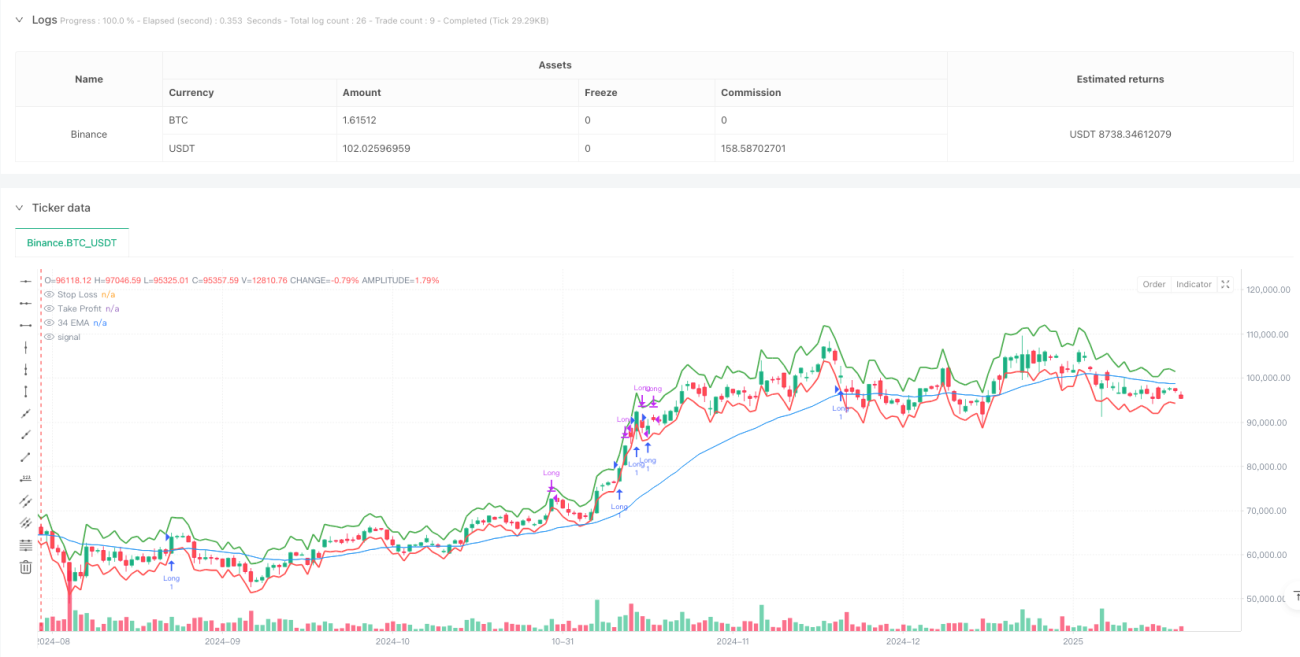

Обзор

Данная стратегия представляет собой торговую систему, сочетающую в себе следование тренду и импульсный разворот. Она основана на определении общего тренда с помощью 34-периодной скользящей средней EMA, выявлении зон перекупленности/перепроданности с помощью индикатора RSI, а также подтверждении торговых сигналов на основе свечных паттернов и объема. Стратегия использует динамический стоп-лосс и тейк-профит на основе ATR, что позволяет адаптировать параметры торговли к рыночной волатильности.

Принцип стратегии

Основная логика стратегии включает следующие ключевые элементы:

- Определение тренда: В качестве основного индикатора тренда используется 34-периодная EMA. Возможности для длинных позиций рассматриваются только при нахождении цены выше EMA.

- Условия входа: Требуется последовательное формирование свечного паттерна «медвежья – бычья – бычья свечи», то есть одна медвежья свеча, за которой следуют две бычьи свечи.

- Подтверждение импульса: Используется RSI для подтверждения импульса. Значение RSI должно быть больше 50, что указывает на восходящий импульс.

- Фильтр объема: Текущий объем должен превышать средний объем за 20 периодов, чтобы обеспечить достаточную рыночную активность.

- Управление рисками: Целевая прибыль устанавливается на уровне 1,5x ATR, а стоп-лосс – на уровне 1x ATR.

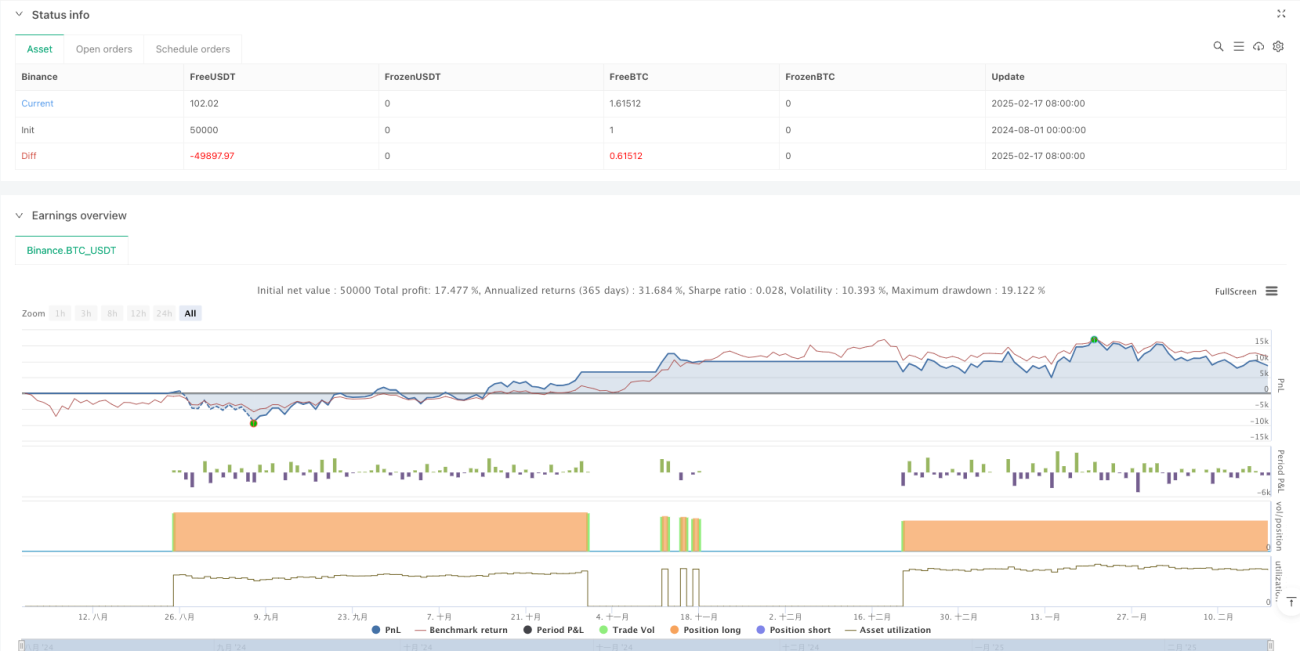

Преимущества стратегии

- Множественное подтверждение сигналов: Комбинация тренда, паттернов, импульса и объема для подтверждения сделок позволяет эффективно снижать количество ложных сигналов.

- Динамическое управление рисками: Стоп-лосс и тейк-профит на основе ATR автоматически корректируются в соответствии с рыночной волатильностью.

- Следование тренду: Использование EMA гарантирует торговлю в направлении основного тренда, повышая вероятность успеха.

- Гибкие настройки параметров: Ключевые параметры, такие как период EMA, пороговые значения RSI, множители ATR, могут быть настроены для адаптации к различным рыночным условиям.

Риски стратегии

- Риск разворота тренда: В точках разворота тренда возможны последовательные убыточные сделки.

- Риск ложного пробоя: Свечные паттерны могут давать ложные пробои, что приводит к ошибочным сигналам.

- Риск рыночной волатильности: В периоды резких колебаний значение ATR может аномально увеличиваться, что влияет на установку стоп-лосса.

- Чувствительность к параметрам: Оптимальные параметры могут существенно различаться в зависимости от рыночных условий.

Направления оптимизации стратегии

- Добавление фильтра силы тренда: Можно внедрить индикатор ADX для измерения силы тренда и совершать сделки только при сильном тренде.

- Улучшение механизма выхода: Можно добавить скользящий стоп-лосс для защиты накопленной прибыли.

- Оптимизация индикатора объема: Рассмотреть использование относительного объема или индикатора пробоя объема.

- Добавление временного фильтра: Можно ввести временные окна для торговли, избегая периодов высокой волатильности.

- Внедрение классификации рыночной среды: Динамическая настройка параметров стратегии в зависимости от различных рыночных условий.

Заключение

Данная стратегия формирует полную торговую систему путем комбинирования нескольких технических индикаторов, что обеспечивает хорошую адаптивность и расширяемость. Основное преимущество стратегии заключается в многомерном подтверждении сигналов и динамическом управлении рисками, однако необходимо также уделять внимание оптимизации параметров и адаптации к рыночным условиям. При постоянной оптимизации и доработке стратегия способна демонстрировать стабильные результаты в различных рыночных условиях.

- 1