یوٹیوب ویٹرنز کی جانب سے "جادوئی ڈبل ای ایم اے حکمت عملی"

مصنف:لیدیہ, تخلیق: 2022-11-07 12:02:31, تازہ کاری: 2023-09-15 20:51:23

یوٹیوب کے سابق فوجیوں کی جادوئی ڈبل ای ایم اے حکمت عملی

اس شمارے میں ، ہم یوٹیوب سے

حکمت عملی میں استعمال ہونے والے اشارے

- ای ایم اے اشارے

ڈیزائن سادگی کی خاطر، ہم ویڈیو میں درج چلتی اوسط exponential استعمال نہیں کریں گے، ہم اس کی بجائے ٹریڈنگ نقطہ نظر کے بلٹ میں ta.ema استعمال کریں گے (یہ اصل میں ایک ہی ہے).

- VuManChu سوئنگ فری اشارے

یہ ٹریڈنگ ویو پر ایک اشارے ہے، ہم ٹریڈنگ ویو پر جانے اور ماخذ کوڈ لینے کی ضرورت ہے.

VuManChu سوئنگ فری کا کوڈ:

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Credits to the original Script - Range Filter DonovanWall https://www.tradingview.com/script/lut7sBgG-Range-Filter-DW/

// This version is the old version of the Range Filter with less settings to tinker with

//@version=4

study(title="Range Filter - B&S Signals", shorttitle="RF - B&S Signals", overlay=true)

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Functions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Size Function

rng_size(x, qty, n)=>

// AC = Cond_EMA(abs(x - x[1]), 1, n)

wper = (n*2) - 1

avrng = ema(abs(x - x[1]), n)

AC = ema(avrng, wper)*qty

rng_size = AC

//Range Filter Function

rng_filt(x, rng_, n)=>

r = rng_

var rfilt = array.new_float(2, x)

array.set(rfilt, 1, array.get(rfilt, 0))

if x - r > array.get(rfilt, 1)

array.set(rfilt, 0, x - r)

if x + r < array.get(rfilt, 1)

array.set(rfilt, 0, x + r)

rng_filt1 = array.get(rfilt, 0)

hi_band = rng_filt1 + r

lo_band = rng_filt1 - r

rng_filt = rng_filt1

[hi_band, lo_band, rng_filt]

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Inputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Source

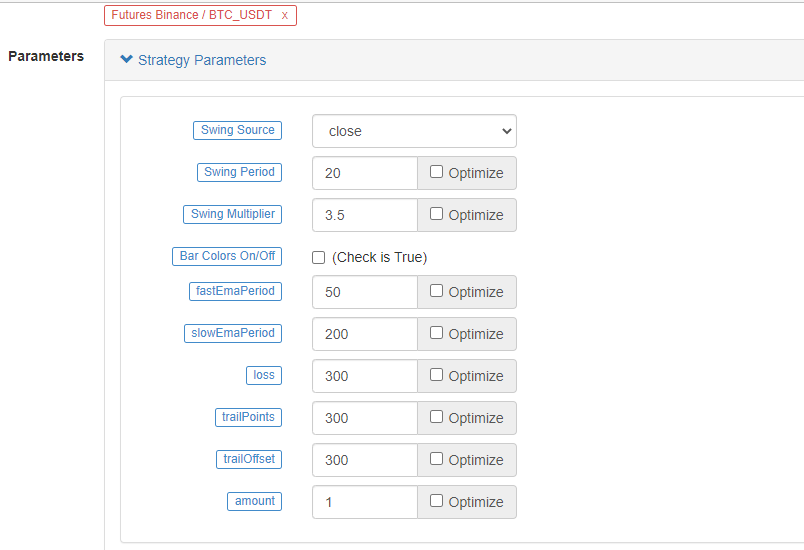

rng_src = input(defval=close, type=input.source, title="Swing Source")

//Range Period

rng_per = input(defval=20, minval=1, title="Swing Period")

//Range Size Inputs

rng_qty = input(defval=3.5, minval=0.0000001, title="Swing Multiplier")

//Bar Colors

use_barcolor = input(defval=false, type=input.bool, title="Bar Colors On/Off")

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Definitions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Filter Values

[h_band, l_band, filt] = rng_filt(rng_src, rng_size(rng_src, rng_qty, rng_per), rng_per)

//Direction Conditions

var fdir = 0.0

fdir := filt > filt[1] ? 1 : filt < filt[1] ? -1 : fdir

upward = fdir==1 ? 1 : 0

downward = fdir==-1 ? 1 : 0

//Trading Condition

longCond = rng_src > filt and rng_src > rng_src[1] and upward > 0 or rng_src > filt and rng_src < rng_src[1] and upward > 0

shortCond = rng_src < filt and rng_src < rng_src[1] and downward > 0 or rng_src < filt and rng_src > rng_src[1] and downward > 0

CondIni = 0

CondIni := longCond ? 1 : shortCond ? -1 : CondIni[1]

longCondition = longCond and CondIni[1] == -1

shortCondition = shortCond and CondIni[1] == 1

//Colors

filt_color = upward ? #05ff9b : downward ? #ff0583 : #cccccc

bar_color = upward and (rng_src > filt) ? (rng_src > rng_src[1] ? #05ff9b : #00b36b) :

downward and (rng_src < filt) ? (rng_src < rng_src[1] ? #ff0583 : #b8005d) : #cccccc

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Outputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Plot

filt_plot = plot(filt, color=filt_color, transp=67, linewidth=3, title="Filter")

//Band Plots

h_band_plot = plot(h_band, color=color.new(#05ff9b, 100), title="High Band")

l_band_plot = plot(l_band, color=color.new(#ff0583, 100), title="Low Band")

//Band Fills

fill(h_band_plot, filt_plot, color=color.new(#00b36b, 92), title="High Band Fill")

fill(l_band_plot, filt_plot, color=color.new(#b8005d, 92), title="Low Band Fill")

//Bar Color

barcolor(use_barcolor ? bar_color : na)

//Plot Buy and Sell Labels

plotshape(longCondition, title = "Buy Signal", text ="BUY", textcolor = color.white, style=shape.labelup, size = size.normal, location=location.belowbar, color = color.new(color.green, 0))

plotshape(shortCondition, title = "Sell Signal", text ="SELL", textcolor = color.white, style=shape.labeldown, size = size.normal, location=location.abovebar, color = color.new(color.red, 0))

//Alerts

alertcondition(longCondition, title="Buy Alert", message = "BUY")

alertcondition(shortCondition, title="Sell Alert", message = "SELL")

حکمت عملی منطق

ای ایم اے اشارے: حکمت عملی میں دو ای ایم اے استعمال کیے جاتے ہیں ، ایک تیز لائن (چھوٹی مدت کا پیرامیٹر) اور دوسرا سست لائن (بڑی مدت کا پیرامیٹر) ہے۔ ڈبل ای ایم اے چلتی اوسط کا مقصد بنیادی طور پر ہمیں مارکیٹ کے رجحان کی سمت کا تعین کرنے میں مدد فراہم کرنا ہے۔

-

لمبی پوزیشن کا انتظام تیز رفتار لائن سست لائن کے اوپر ہے.

-

مختصر پوزیشن کا انتظام تیز رفتار لائن سست لائن کے نیچے ہے.

VuManChu سوئنگ فری اشارے: VuManChu سوئنگ فری اشارے کا استعمال سگنل بھیجنے اور فیصلہ کرنے کے لئے کیا جاتا ہے کہ آیا کسی آرڈر کو دیگر شرائط کے ساتھ مل کر رکھا جائے۔ یہ VuManChu سوئنگ فری اشارے کے سورس کوڈ سے دیکھا جاسکتا ہے کہ لانگ کنڈیشن متغیر خریدنے کے سگنل کی نمائندگی کرتا ہے اور شارٹ کنڈیشن متغیر فروخت سگنل کی نمائندگی کرتا ہے۔ یہ دونوں متغیرات آرڈر دینے کی شرائط کی بعد میں تحریر کے لئے استعمال ہوں گے۔

اب آئیے ٹریڈنگ سگنل کے مخصوص ٹرگر حالات کے بارے میں بات کرتے ہیں:

-

طویل پوزیشن میں داخل ہونے کے قواعد: مثبت K لائن کی بندش کی قیمت EMA کی تیز لائن سے اوپر ہونی چاہئے ، دونوں EMAs ایک طویل پوزیشن ہونی چاہئے (سست لائن سے اوپر تیز لائن) ، اور VuManChu سوئنگ فری اشارے کو خرید کا اشارہ دکھانا چاہئے (longCondition درست ہے) ۔ اگر تینوں شرائط پوری ہوجاتی ہیں تو ، یہ K لائن طویل پوزیشن میں داخل ہونے کے لئے کلیدی K لائن ہے ، اور اس K لائن کی بندش کی قیمت انٹری پوزیشن ہے۔

-

مختصر پوزیشن میں داخل ہونے کے قواعد (لانگ پوزیشن کے برعکس): منفی K لائن کی بندش کی قیمت EMA کی تیز لائن سے نیچے ہونی چاہئے ، دونوں EMAs ایک مختصر پوزیشن ہونی چاہئے (سست لائن سے نیچے تیز لائن) ، اور VuManChu سوئنگ فری اشارے کو فروخت کا اشارہ دکھانا چاہئے (shortCondition درست ہے) ۔ اگر تینوں شرائط پوری ہو جاتی ہیں تو ، K لائن کی بندش کی قیمت مختصر انٹری پوزیشن ہے۔

کیا تجارتی منطق بہت آسان ہے؟ چونکہ ماخذ ویڈیو میں منافع کی روک تھام اور نقصان کی روک تھام کی وضاحت نہیں کی گئی ہے ، لہذا میں اعتدال پسند منافع کی روک تھام اور نقصان کی روک تھام کا طریقہ آزادانہ طور پر استعمال کروں گا ، نقصان کو روکنے کے لئے فکسڈ پوائنٹس کا استعمال کروں گا ، اور منافع کی روک تھام کو ٹریک کروں گا۔

کوڈ کا ڈیزائن

VuManChu سوئنگ فری اشارے کے لئے کوڈ، ہم کسی بھی تبدیلی کے بغیر براہ راست ہماری حکمت عملی کوڈ میں ڈال دیا.

پھر فوری طور پر اس کے بعد، ہم پائن زبان کا ایک ٹکڑا لکھتے ہیں جو تجارتی فنکشن کو لاگو کرتا ہے:

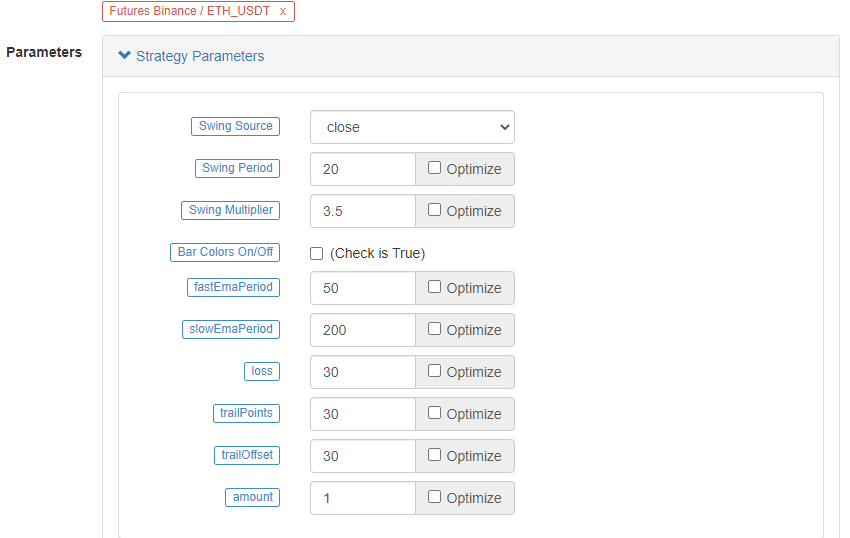

// extend

fastEmaPeriod = input(50, "fastEmaPeriod") // fast line period

slowEmaPeriod = input(200, "slowEmaPeriod") // slow line period

loss = input(30, "loss") // stop loss points

trailPoints = input(30, "trailPoints") // number of trigger points for moving stop loss

trailOffset = input(30, "trailOffset") // moving stop profit offset (points)

amount = input(1, "amount") // order amount

emaFast = ta.ema(close, fastEmaPeriod) // calculate the fast line EMA

emaSlow = ta.ema(close, slowEmaPeriod) // calculate the slow line EMA

buyCondition = longCondition and emaFast > emaSlow and close > open and close > emaFast // entry conditions for long positions

sellCondition = shortCondition and emaFast < emaSlow and close < open and close < emaFast // entry conditions for short positions

if buyCondition and strategy.position_size == 0

strategy.entry("long", strategy.long, amount)

strategy.exit("exit_long", "long", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

if sellCondition and strategy.position_size == 0

strategy.entry("short", strategy.short, amount)

strategy.exit("exit_short", "short", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

A.Itدیکھا جا سکتا ہے کہ جب buyCondition سچ ہے، یعنی:

- متغیر longCondition درست ہے (VuManChu سوئنگ فری اشارے ایک طویل پوزیشن سگنل بھیجتا ہے).

- emaFast > emaSlow (EMA طویل پوزیشن سیدھ) ۔

- close > open (موجودہ BAR مثبت ہے) ، close > emaFast (کلوزنگ قیمت EMA فاسٹ لائن سے اوپر ہے) ۔

طویل عرصے تک جانے کے لیے تین شرائط۔

B.جب sellCondition درست ہے تو ، مختصر پوزیشن بنانے کے لئے تین شرائط برقرار ہیں (یہاں دہرائے نہیں گئے ہیں) ۔

پھر ہم استعمال کرتے ہیں strategy.entry تقریب میں داخل ہونے اور ایک پوزیشن کھولنے کے لئے اگر حالت فیصلے سگنل ٹرگر کی صورت میں، اور مقررstrategy.exitایک ہی وقت میں نقصان کو روکنے اور ٹریل منافع کے لئے تقریب.

مکمل کوڈ

/*backtest

start: 2022-01-01 00:00:00

end: 2022-10-08 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

args: [["ZPrecision",0,358374]]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Credits to the original Script - Range Filter DonovanWall https://www.tradingview.com/script/lut7sBgG-Range-Filter-DW/

// This version is the old version of the Range Filter with less settings to tinker with

//@version=4

study(title="Range Filter - B&S Signals", shorttitle="RF - B&S Signals", overlay=true)

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Functions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Size Function

rng_size(x, qty, n)=>

// AC = Cond_EMA(abs(x - x[1]), 1, n)

wper = (n*2) - 1

avrng = ema(abs(x - x[1]), n)

AC = ema(avrng, wper)*qty

rng_size = AC

//Range Filter Function

rng_filt(x, rng_, n)=>

r = rng_

var rfilt = array.new_float(2, x)

array.set(rfilt, 1, array.get(rfilt, 0))

if x - r > array.get(rfilt, 1)

array.set(rfilt, 0, x - r)

if x + r < array.get(rfilt, 1)

array.set(rfilt, 0, x + r)

rng_filt1 = array.get(rfilt, 0)

hi_band = rng_filt1 + r

lo_band = rng_filt1 - r

rng_filt = rng_filt1

[hi_band, lo_band, rng_filt]

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Inputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Source

rng_src = input(defval=close, type=input.source, title="Swing Source")

//Range Period

rng_per = input(defval=20, minval=1, title="Swing Period")

//Range Size Inputs

rng_qty = input(defval=3.5, minval=0.0000001, title="Swing Multiplier")

//Bar Colors

use_barcolor = input(defval=false, type=input.bool, title="Bar Colors On/Off")

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Definitions

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Range Filter Values

[h_band, l_band, filt] = rng_filt(rng_src, rng_size(rng_src, rng_qty, rng_per), rng_per)

//Direction Conditions

var fdir = 0.0

fdir := filt > filt[1] ? 1 : filt < filt[1] ? -1 : fdir

upward = fdir==1 ? 1 : 0

downward = fdir==-1 ? 1 : 0

//Trading Condition

longCond = rng_src > filt and rng_src > rng_src[1] and upward > 0 or rng_src > filt and rng_src < rng_src[1] and upward > 0

shortCond = rng_src < filt and rng_src < rng_src[1] and downward > 0 or rng_src < filt and rng_src > rng_src[1] and downward > 0

CondIni = 0

CondIni := longCond ? 1 : shortCond ? -1 : CondIni[1]

longCondition = longCond and CondIni[1] == -1

shortCondition = shortCond and CondIni[1] == 1

//Colors

filt_color = upward ? #05ff9b : downward ? #ff0583 : #cccccc

bar_color = upward and (rng_src > filt) ? (rng_src > rng_src[1] ? #05ff9b : #00b36b) :

downward and (rng_src < filt) ? (rng_src < rng_src[1] ? #ff0583 : #b8005d) : #cccccc

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Outputs

//-----------------------------------------------------------------------------------------------------------------------------------------------------------------

//Filter Plot

filt_plot = plot(filt, color=filt_color, transp=67, linewidth=3, title="Filter")

//Band Plots

h_band_plot = plot(h_band, color=color.new(#05ff9b, 100), title="High Band")

l_band_plot = plot(l_band, color=color.new(#ff0583, 100), title="Low Band")

//Band Fills

fill(h_band_plot, filt_plot, color=color.new(#00b36b, 92), title="High Band Fill")

fill(l_band_plot, filt_plot, color=color.new(#b8005d, 92), title="Low Band Fill")

//Bar Color

barcolor(use_barcolor ? bar_color : na)

//Plot Buy and Sell Labels

plotshape(longCondition, title = "Buy Signal", text ="BUY", textcolor = color.white, style=shape.labelup, size = size.normal, location=location.belowbar, color = color.new(color.green, 0))

plotshape(shortCondition, title = "Sell Signal", text ="SELL", textcolor = color.white, style=shape.labeldown, size = size.normal, location=location.abovebar, color = color.new(color.red, 0))

//Alerts

alertcondition(longCondition, title="Buy Alert", message = "BUY")

alertcondition(shortCondition, title="Sell Alert", message = "SELL")

// extend

fastEmaPeriod = input(50, "fastEmaPeriod")

slowEmaPeriod = input(200, "slowEmaPeriod")

loss = input(30, "loss")

trailPoints = input(30, "trailPoints")

trailOffset = input(30, "trailOffset")

amount = input(1, "amount")

emaFast = ta.ema(close, fastEmaPeriod)

emaSlow = ta.ema(close, slowEmaPeriod)

buyCondition = longCondition and emaFast > emaSlow and close > open and close > emaFast

sellCondition = shortCondition and emaFast < emaSlow and close < open and close < emaFast

if buyCondition and strategy.position_size == 0

strategy.entry("long", strategy.long, amount)

strategy.exit("exit_long", "long", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

if sellCondition and strategy.position_size == 0

strategy.entry("short", strategy.short, amount)

strategy.exit("exit_short", "short", amount, loss=loss, trail_points=trailPoints, trail_offset=trailOffset)

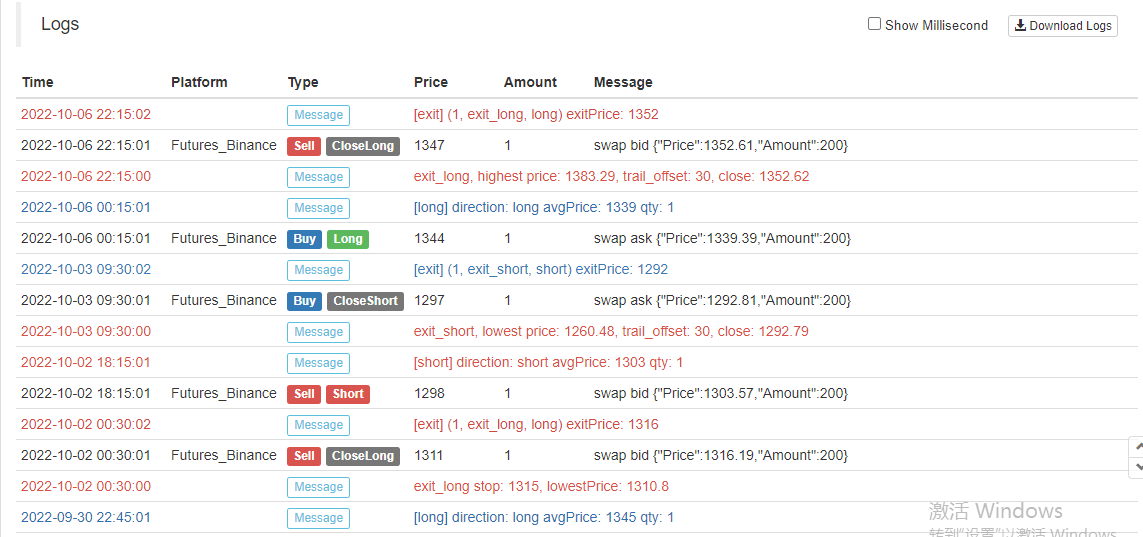

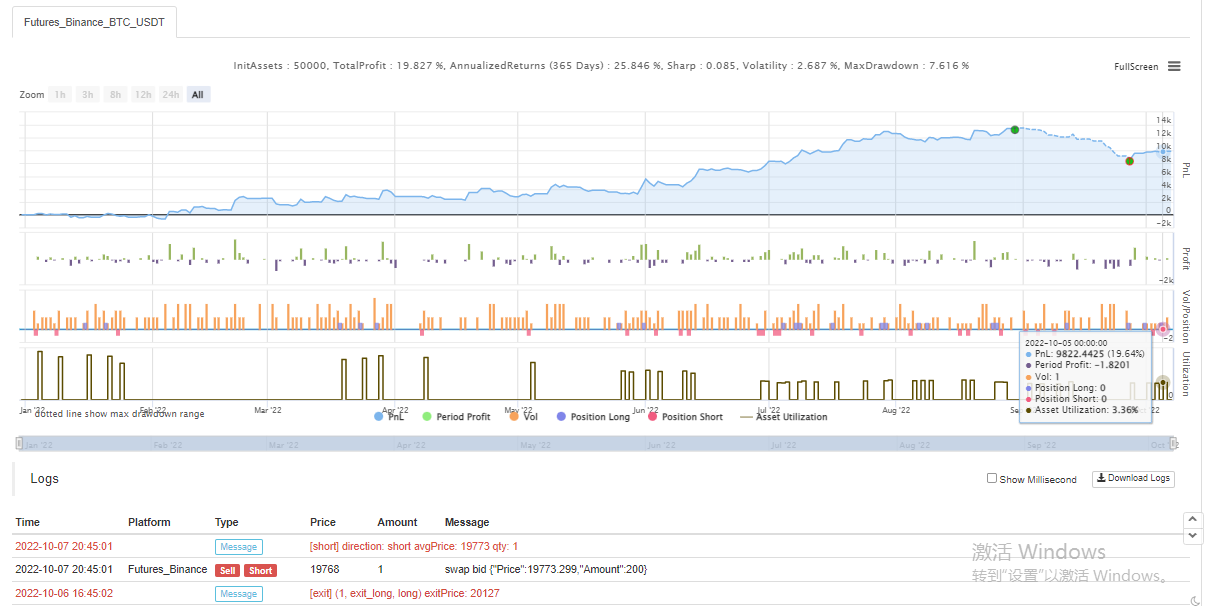

بیک ٹیسٹ

بیک ٹیسٹ کا وقت جنوری 2022 سے اکتوبر 2022 تک ہے۔ کے لائن کی مدت 15 منٹ ہے اور بیک ٹیسٹ کے لئے اختتامی قیمت کا ماڈل استعمال کیا جاتا ہے۔ مارکیٹ بائننس ETH_USDT دائمی معاہدے کا انتخاب کرتی ہے۔ پیرامیٹرز ماخذ ویڈیو میں تیز لائن کی 50 مدت اور سست لائن کی 200 مدت کے مطابق مقرر کیے گئے ہیں۔ دیگر پیرامیٹرز ڈیفالٹ کے مطابق تبدیل نہیں ہوتے ہیں۔ میں اسٹاپ نقصان اور ٹریکنگ اسٹاپ منافع کے پوائنٹس کو 30 پوائنٹس تک ذہنی طور پر مقرر کرتا ہوں۔

بیک ٹسٹنگ کے نتائج معمول کے مطابق ہیں ، اور ایسا لگتا ہے کہ اسٹاپ نقصان کے پیرامیٹرز کا بیک ٹسٹنگ کے نتائج پر کچھ اثر پڑتا ہے۔ مجھے لگتا ہے کہ اس پہلو کو ابھی بھی بہتر بنانے اور ڈیزائن کرنے کی ضرورت ہے۔ تاہم ، اسٹریٹجک سگنل ٹریڈنگ کو متحرک کرنے کے بعد ، جیت کی شرح اب بھی ٹھیک ہے۔

آئیے ایک مختلف BTC_USDT دائمی معاہدہ آزمائیں:

بی ٹی سی پر بیک ٹیسٹ کا نتیجہ بھی بہت منافع بخش تھا:

حکمت عملی:https://www.fmz.com/strategy/385745

ایسا لگتا ہے کہ یہ تجارتی طریقہ رجحان کو سمجھنے کے لئے نسبتا reliable قابل اعتماد ہے ، آپ اس خیال کے مطابق ڈیزائن کو بہتر بنانا جاری رکھ سکتے ہیں۔ اس مضمون میں ، ہم نے نہ صرف ڈبل موونگ ایوریج حکمت عملی کے خیال کے بارے میں سیکھا ، بلکہ یوٹیوب پر تجربہ کاروں کی حکمت عملی پر کارروائی اور سیکھنے کا طریقہ بھی سیکھا۔ ٹھیک ہے ، مذکورہ بالا حکمت عملی کا کوڈ صرف میرا اینٹوں اور مارٹر ہے ، بیک ٹیسٹ کے نتائج مخصوص اصلی بوٹ کے نتائج کی نمائندگی نہیں کرتے ہیں ، حکمت عملی کا کوڈ ، ڈیزائن صرف حوالہ کے لئے ہے۔ آپ کی حمایت کے لئے شکریہ ، ہم آپ کو اگلی بار دیکھیں گے!

- کریپٹوکرنسی مارکیٹ میں بنیادی تجزیہ کی مقدار: اعداد و شمار کو اپنے لئے بولنے دیں!

- ایک بار پھر ، ہم نے ایک بار پھر اس بات کا یقین کرلیا ہے کہ یہ ایک بہت بڑا مسئلہ ہے ، لیکن ہم اس کے بارے میں مزید نہیں جانتے ہیں۔

- کوانٹائزڈ ٹرانزیکشنز کے لیے ایک لازمی ٹول۔

- ہر چیز پر قابو پانا - ایف ایم زیڈ ٹریڈنگ ٹرمینل کا نیا ورژن (ٹی آر بی آربیٹریج سورس کوڈ کے ساتھ) کا تعارف

- FMZ کے نئے ورژن کے ٹرانزیکشن ٹرمینل کے بارے میں سب کچھ جاننے کے لئے یہاں کلک کریں

- ایف ایم زیڈ کوانٹ: کریپٹوکرنسی مارکیٹ میں مشترکہ تقاضوں کے ڈیزائن مثالوں کا تجزیہ (II)

- 80 لائنوں کے کوڈ میں ہائی فریکوئینسی حکمت عملی کے ساتھ دماغ کے بغیر سیلز بوٹس کا استحصال کیسے کریں

- ایف ایم زیڈ کیوٹیفیکیشن: کریپٹوکرنسی مارکیٹ میں عام ضروریات کے ڈیزائن کی مثالوں کا تجزیہ (ب)

- 80 لائنوں کے کوڈ کے ساتھ ہائی فریکوئینسی کی حکمت عملی کے ساتھ فروخت کے لیے بے دماغ روبوٹ کا استحصال کیسے کیا گیا؟

- ایف ایم زیڈ کوانٹ: کریپٹوکرنسی مارکیٹ میں مشترکہ تقاضوں کے ڈیزائن مثالوں کا تجزیہ (I)

- ایف ایم زیڈ کیوٹیفیکیشن: کریپٹوکرنسی مارکیٹ میں عام ضروریات کے ڈیزائن کی مثالوں کا تجزیہ (1)