Nghiên cứu về Binance Futures Multi-currency Hedging Strategy Phần 2

Tác giả:Tốt, Tạo: 2020-05-09 16:03:01, Cập nhật: 2023-11-04 19:49:47

Địa chỉ báo cáo nghiên cứu gốc:https://www.fmz.com/digest-topic/5584Bạn có thể đọc nó trước, bài viết này sẽ không có nội dung trùng lặp. Bài viết này sẽ làm nổi bật quá trình tối ưu hóa của chiến lược thứ hai. Sau khi tối ưu hóa, chiến lược thứ hai được cải thiện rõ ràng, nên nâng cấp chiến lược theo bài viết này.

# Libraries to import

import pandas as pd

import requests

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

%matplotlib inline

symbols = ['ETH', 'BCH', 'XRP', 'EOS', 'LTC', 'TRX', 'ETC', 'LINK', 'XLM', 'ADA', 'XMR', 'DASH', 'ZEC', 'XTZ', 'BNB', 'ATOM', 'ONT', 'IOTA', 'BAT', 'VET', 'NEO', 'QTUM', 'IOST']

price_usdt = pd.read_csv('https://www.fmz.com/upload/asset/20227de6c1d10cb9dd1.csv ', index_col = 0)

price_usdt.index = pd.to_datetime(price_usdt.index)

price_usdt_norm = price_usdt/price_usdt.fillna(method='bfill').iloc[0,]

price_usdt_btc = price_usdt.divide(price_usdt['BTC'],axis=0)

price_usdt_btc_norm = price_usdt_btc/price_usdt_btc.fillna(method='bfill').iloc[0,]

class Exchange:

def __init__(self, trade_symbols, leverage=20, commission=0.00005, initial_balance=10000, log=False):

self.initial_balance = initial_balance # Initial asset

self.commission = commission

self.leverage = leverage

self.trade_symbols = trade_symbols

self.date = ''

self.log = log

self.df = pd.DataFrame(columns=['margin','total','leverage','realised_profit','unrealised_profit'])

self.account = {'USDT':{'realised_profit':0, 'margin':0, 'unrealised_profit':0, 'total':initial_balance, 'leverage':0, 'fee':0}}

for symbol in trade_symbols:

self.account[symbol] = {'amount':0, 'hold_price':0, 'value':0, 'price':0, 'realised_profit':0, 'margin':0, 'unrealised_profit':0,'fee':0}

def Trade(self, symbol, direction, price, amount, msg=''):

if self.date and self.log:

print('%-20s%-5s%-5s%-10.8s%-8.6s %s'%(str(self.date), symbol, 'buy' if direction == 1 else 'sell', price, amount, msg))

cover_amount = 0 if direction*self.account[symbol]['amount'] >=0 else min(abs(self.account[symbol]['amount']), amount)

open_amount = amount - cover_amount

self.account['USDT']['realised_profit'] -= price*amount*self.commission # Minus handling fee

self.account['USDT']['fee'] += price*amount*self.commission

self.account[symbol]['fee'] += price*amount*self.commission

if cover_amount > 0: # close position first

self.account['USDT']['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount # Profit

self.account['USDT']['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage # Free margin

self.account[symbol]['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount

self.account[symbol]['amount'] -= -direction*cover_amount

self.account[symbol]['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage

self.account[symbol]['hold_price'] = 0 if self.account[symbol]['amount'] == 0 else self.account[symbol]['hold_price']

if open_amount > 0:

total_cost = self.account[symbol]['hold_price']*direction*self.account[symbol]['amount'] + price*open_amount

total_amount = direction*self.account[symbol]['amount']+open_amount

self.account['USDT']['margin'] += open_amount*price/self.leverage

self.account[symbol]['hold_price'] = total_cost/total_amount

self.account[symbol]['amount'] += direction*open_amount

self.account[symbol]['margin'] += open_amount*price/self.leverage

self.account[symbol]['unrealised_profit'] = (price - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = price

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*price

return True

def Buy(self, symbol, price, amount, msg=''):

self.Trade(symbol, 1, price, amount, msg)

def Sell(self, symbol, price, amount, msg=''):

self.Trade(symbol, -1, price, amount, msg)

def Update(self, date, close_price): # Update assets

self.date = date

self.close = close_price

self.account['USDT']['unrealised_profit'] = 0

for symbol in self.trade_symbols:

if np.isnan(close_price[symbol]):

continue

self.account[symbol]['unrealised_profit'] = (close_price[symbol] - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = close_price[symbol]

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*close_price[symbol]

self.account['USDT']['unrealised_profit'] += self.account[symbol]['unrealised_profit']

if self.date.hour in [0,8,16]:

pass

self.account['USDT']['realised_profit'] += -self.account[symbol]['amount']*close_price[symbol]*0.01/100

self.account['USDT']['total'] = round(self.account['USDT']['realised_profit'] + self.initial_balance + self.account['USDT']['unrealised_profit'],6)

self.account['USDT']['leverage'] = round(self.account['USDT']['margin']/self.account['USDT']['total'],4)*self.leverage

self.df.loc[self.date] = [self.account['USDT']['margin'],self.account['USDT']['total'],self.account['USDT']['leverage'],self.account['USDT']['realised_profit'],self.account['USDT']['unrealised_profit']]

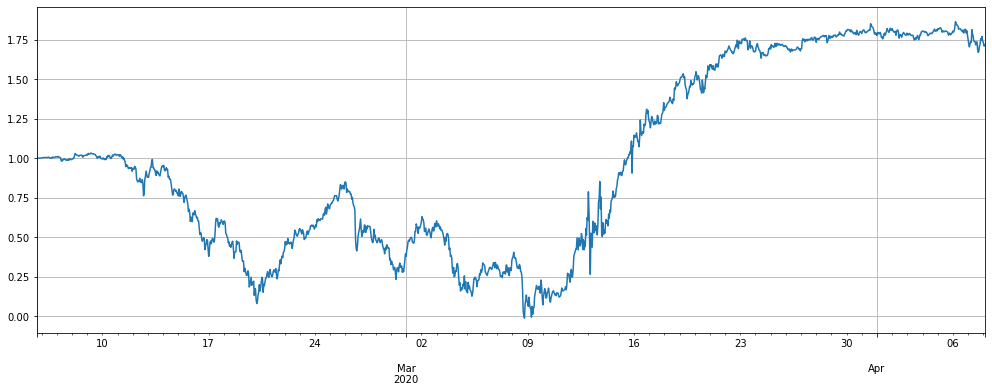

Hiệu suất của chiến lược ban đầu, sau khi lựa chọn loại tiền tệ, hoạt động tốt, nhưng vẫn còn nhiều vị trí nắm giữ, nói chung là khoảng 4 lần

Nguyên tắc:

- Cập nhật báo giá thị trường và các vị trí giữ tài khoản, giá ban đầu sẽ được ghi lại trong lần chạy đầu tiên (tiền tệ mới được thêm được tính theo thời điểm tham gia)

- Cập nhật chỉ số, chỉ số là chỉ số giá altcoin-bitcoin = trung bình (tổng ((giá altcoin / giá bitcoin) / (giá ban đầu altcoin / giá ban đầu bitcoin)))

- Đánh giá hoạt động dài và ngắn theo chỉ số lệch và đánh giá kích thước vị trí theo kích thước lệch

- Đặt đơn đặt hàng, số lượng đơn đặt hàng được xác định bởi chiến lược ủy quyền băng trôi và giao dịch được thực hiện theo giá thực thi mới nhất

- Quay lại.

trade_symbols = list(set(symbols)-set(['LINK','XTZ','BCH', 'ETH'])) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2b = e

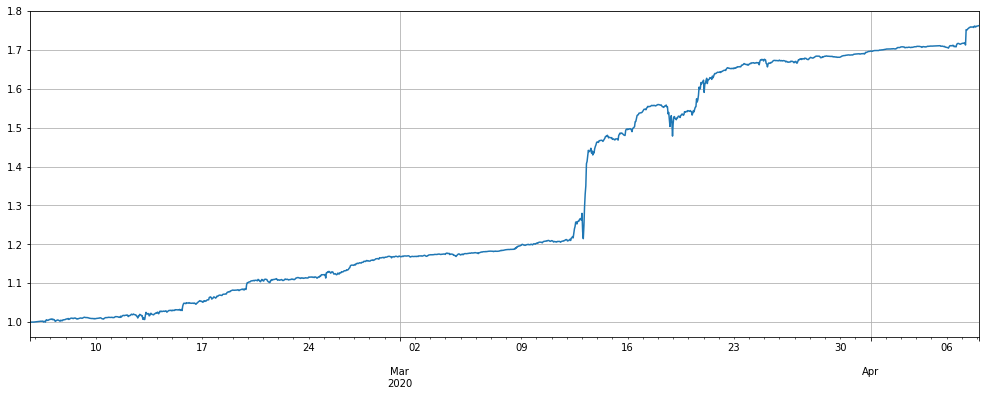

(stragey_2b.df['total']/stragey_2b.initial_balance).plot(figsize=(17,6),grid = True);

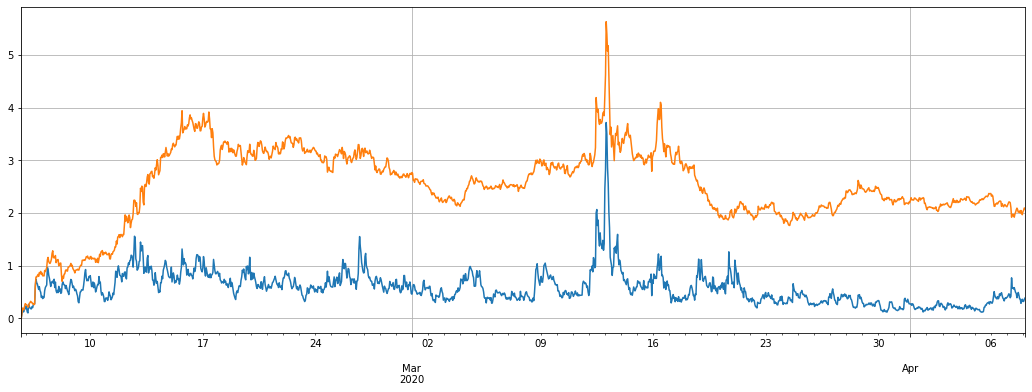

stragey_2b.df['leverage'].plot(figsize=(18,6),grid = True); # leverage

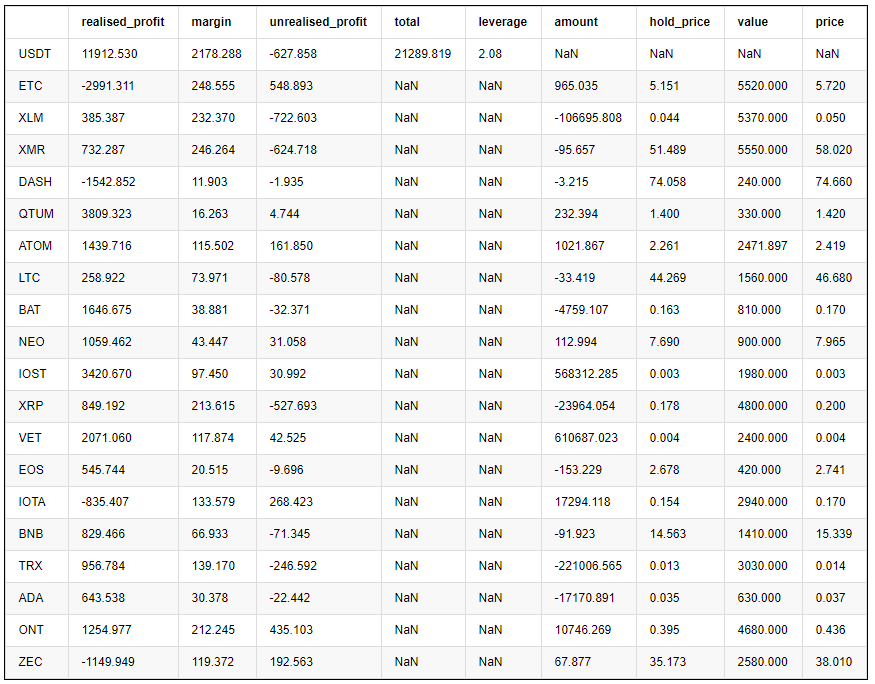

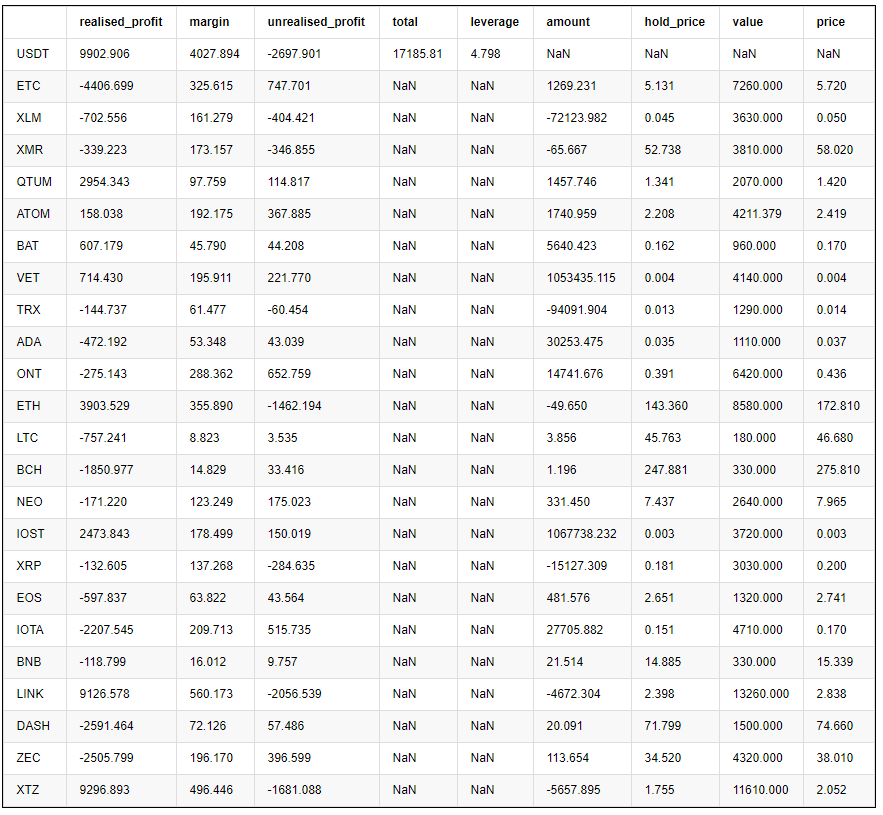

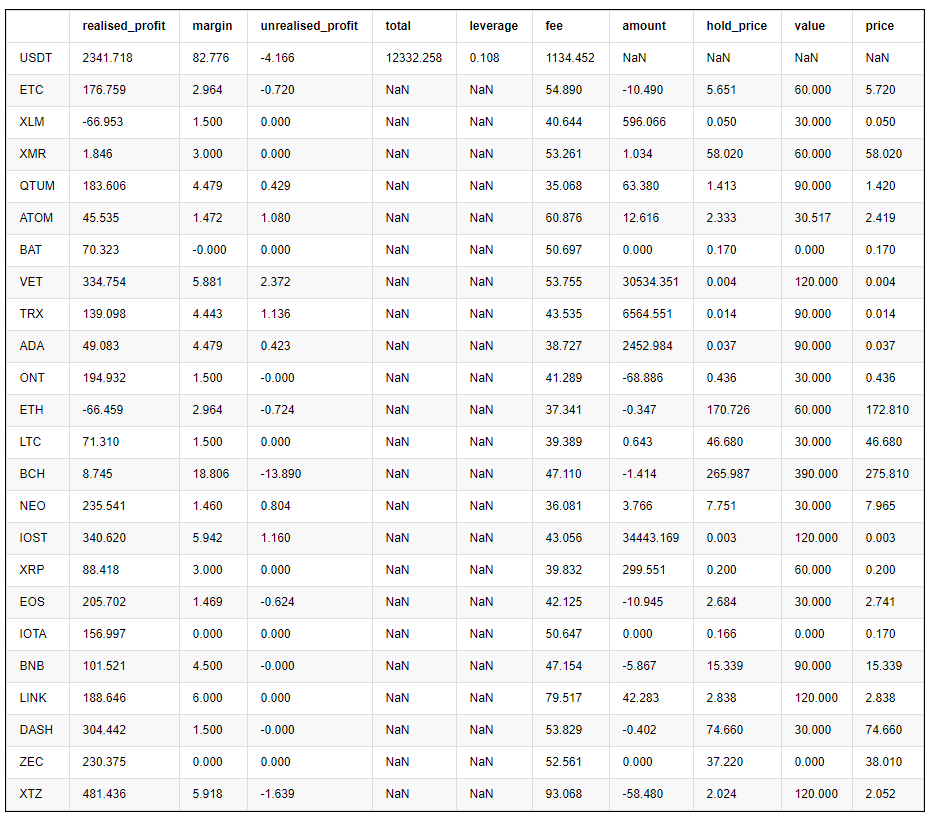

pd.DataFrame(e.account).T.apply(lambda x:round(x,3)) # holding position

Tại sao phải cải thiện

Vấn đề lớn nhất ban đầu là so sánh giữa giá mới nhất và giá ban đầu bắt đầu bởi chiến lược. Khi thời gian trôi qua, nó sẽ trở nên càng ngày càng lệch. Chúng ta sẽ tích lũy rất nhiều vị trí trong các loại tiền tệ này. Vấn đề lớn nhất với việc lọc tiền tệ là chúng ta vẫn có thể có các loại tiền tệ độc đáo trong tương lai dựa trên kinh nghiệm trong quá khứ của chúng ta. Sau đây là hiệu suất của chế độ không lọc. Trên thực tế, khi trade_value = 300, ở giai đoạn giữa của chiến lược chạy, nó đã mất tất cả mọi thứ. Ngay cả khi không, LINK và XTZ cũng nắm giữ các vị trí trên 10000USDT, quá lớn. Do đó, chúng ta phải giải quyết vấn đề này trong backtest và vượt qua bài kiểm tra của tất cả các loại tiền tệ.

trade_symbols = list(set(symbols)) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2c = e

(stragey_2c.df['total']/stragey_2c.initial_balance).plot(figsize=(17,6),grid = True);

pd.DataFrame(stragey_2c.account).T.apply(lambda x:round(x,3)) # Last holding position

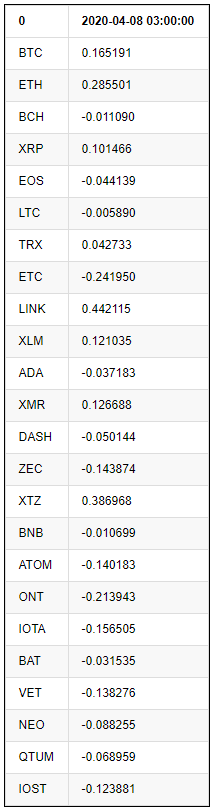

((price_usdt_btc_norm.iloc[-1:] - price_usdt_btc_norm_mean[-1]).T) # Each currency deviates from the initial situation

Vì nguyên nhân của vấn đề là so sánh với giá ban đầu, nó có thể ngày càng thiên vị hơn.

Alpha = 0.05

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() #Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))#All currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2d = e

#print(N,stragey_2d.df['total'][-1],pd.DataFrame(stragey_2d.account).T.apply(lambda x:round(x,3))['value'].sum())

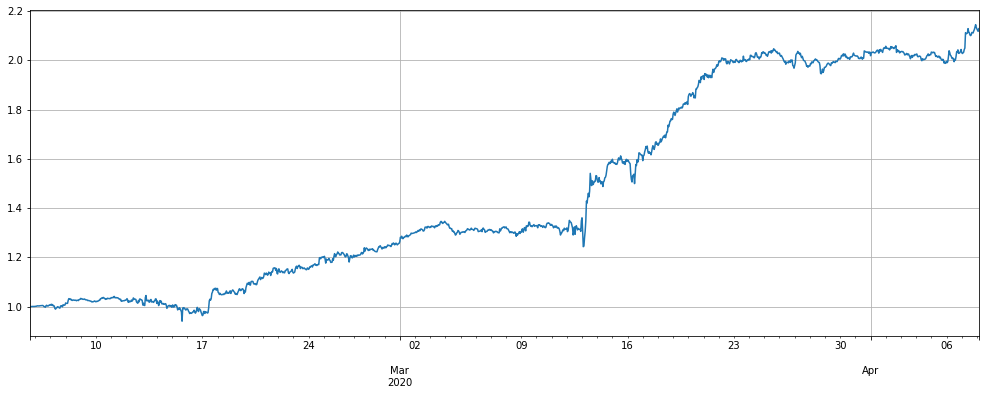

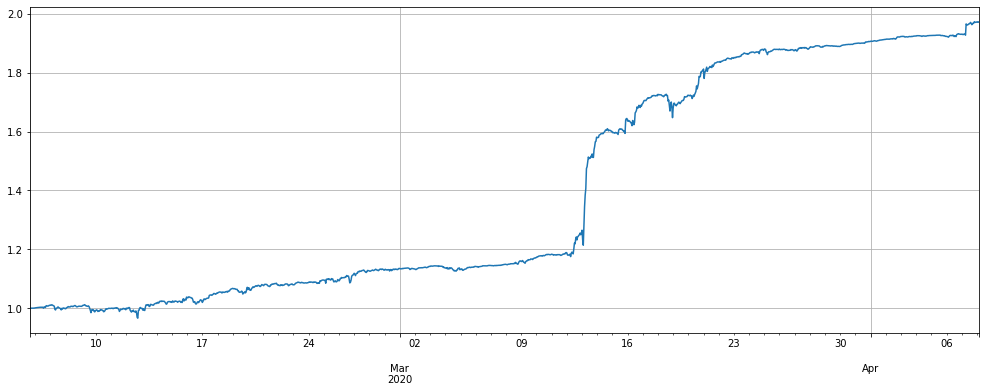

Hiệu suất của chiến lược đã hoàn toàn đáp ứng mong đợi của chúng tôi, và lợi nhuận gần như giống nhau. Tình huống bùng nổ các vị trí tài khoản trong đồng tiền gốc của tất cả các loại tiền tệ cũng đã chuyển đổi trơn tru, và hầu như không có sự thoái lui. Kích thước vị trí mở đầu tương tự, hầu hết đòn bẩy đều dưới 1 lần, vào ngày 12 tháng 3 năm 2020 giá giảm mạnh trường hợp cực đoan, nó vẫn không vượt quá 4 lần, có nghĩa là chúng tôi có thể tăng trade_value, và dưới cùng một đòn bẩy, tăng gấp đôi lợi nhuận.

Tại sao vị trí sẽ bị hạ thấp? Hãy tưởng tượng tham gia chỉ số altcoin không thay đổi, một đồng tiền đã tăng 100% và nó sẽ được duy trì trong một thời gian dài. Chiến lược ban đầu sẽ giữ các vị trí ngắn 300 * 100 = 30000USDT trong một thời gian dài, và chiến lược mới cuối cùng sẽ theo dõi giá chuẩn Tại mức giá mới nhất, bạn sẽ không giữ bất kỳ vị trí nào vào cuối.

(stragey_2d.df['total']/stragey_2d.initial_balance).plot(figsize=(17,6),grid = True);

#(stragey_2c.df['total']/stragey_2c.initial_balance).plot(figsize=(17,6),grid = True);

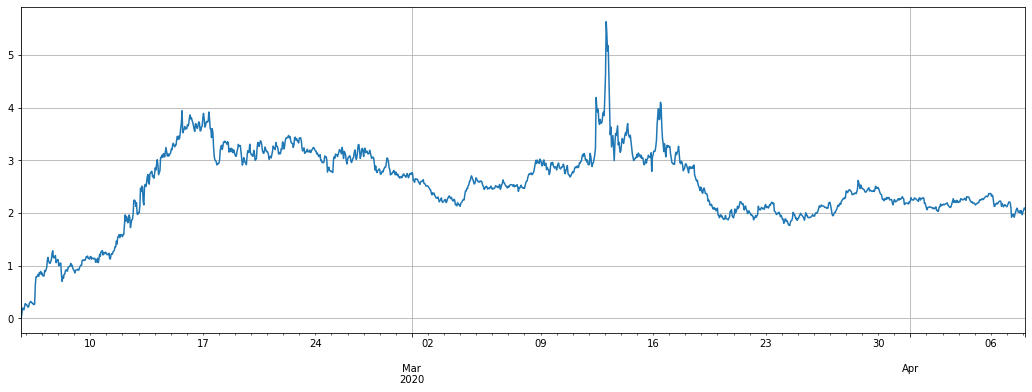

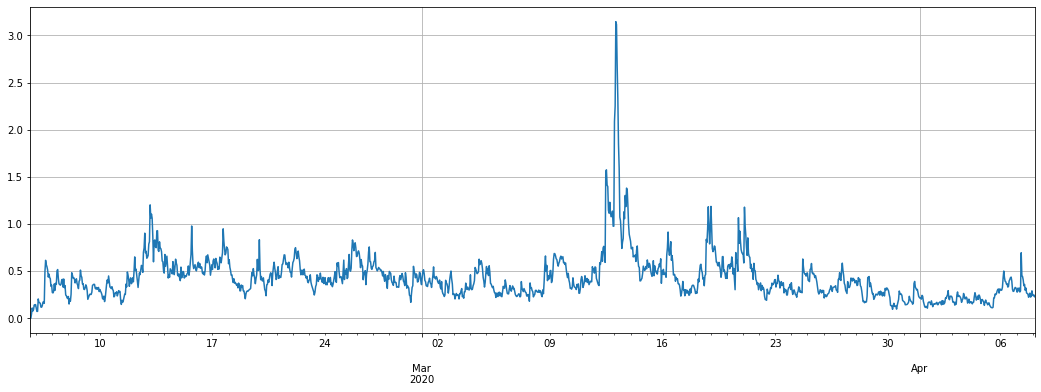

stragey_2d.df['leverage'].plot(figsize=(18,6),grid = True);

stragey_2b.df['leverage'].plot(figsize=(18,6),grid = True); # Screen currency strategy leverage

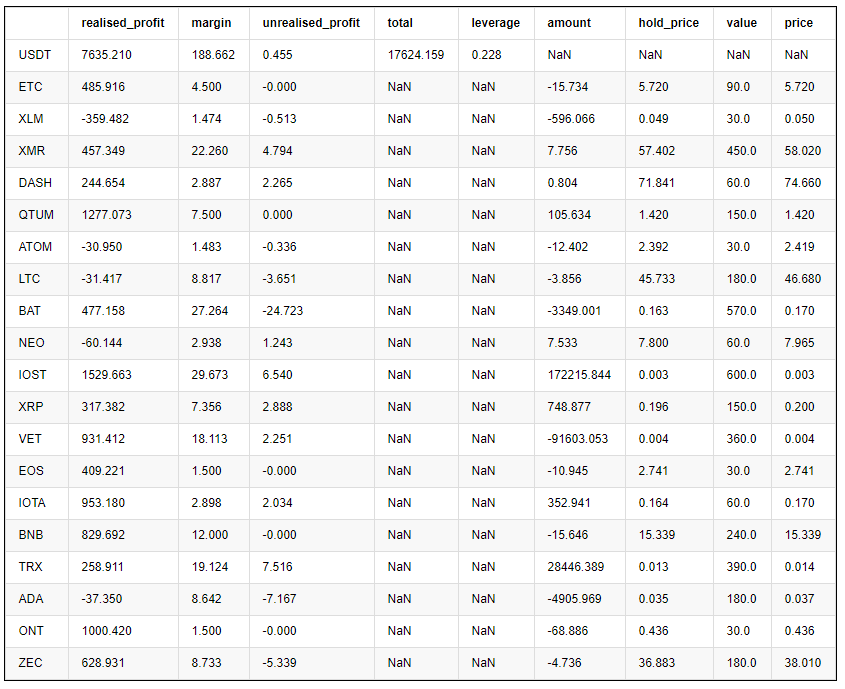

pd.DataFrame(stragey_2d.account).T.apply(lambda x:round(x,3))

Điều gì sẽ xảy ra với đồng tiền với cơ chế sàng lọc, với các tham số tương tự, lợi nhuận giai đoạn trước có hiệu suất tốt hơn, sự khôi phục nhỏ hơn, nhưng lợi nhuận tổng thể thấp hơn một chút.

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(50).mean()

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=0.05).mean()

trade_symbols = list(set(symbols)-set(['LINK','XTZ','BCH', 'ETH'])) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2e = e

#(stragey_2d.df['total']/stragey_2d.initial_balance).plot(figsize=(17,6),grid = True);

(stragey_2e.df['total']/stragey_2e.initial_balance).plot(figsize=(17,6),grid = True);

stragey_2e.df['leverage'].plot(figsize=(18,6),grid = True);

pd.DataFrame(stragey_2e.account).T.apply(lambda x:round(x,3))

Tối ưu hóa tham số

Càng lớn thiết lập tham số Alpha của đường trung bình chuyển động theo cấp số nhân, mức độ nhạy cảm của việc theo dõi giá chuẩn càng nhiều, số lượng giao dịch càng ít, vị trí nắm giữ cuối cùng càng thấp. khi hạ đòn bẩy, lợi nhuận cũng giảm. Giảm mức khôi phục tối đa, nó có thể làm tăng khối lượng giao dịch. Các hoạt động cân bằng cụ thể cần dựa trên kết quả backtest.

Vì backtest là một đường 1h K, nó chỉ có thể được cập nhật một lần mỗi giờ, thị trường thực tế có thể được cập nhật nhanh hơn, và cần phải cân nhắc các cài đặt cụ thể một cách toàn diện.

Đây là kết quả của việc tối ưu hóa:

for Alpha in [i/100 for i in range(1,30)]:

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))# All currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2d = e

# These are the final net value, the initial maximum backtest, the final position size, and the handling fee

print(Alpha, round(stragey_2d.account['USDT']['total'],1), round(1-stragey_2d.df['total'].min()/stragey_2d.initial_balance,2),round(pd.DataFrame(stragey_2d.account).T['value'].sum(),1),round(stragey_2d.account['USDT']['fee']))

0.01 21116.2 0.14 15480.0 2178.0

0.02 20555.6 0.07 12420.0 2184.0

0.03 20279.4 0.06 9990.0 2176.0

0.04 20021.5 0.04 8580.0 2168.0

0.05 19719.1 0.03 7740.0 2157.0

0.06 19616.6 0.03 7050.0 2145.0

0.07 19344.0 0.02 6450.0 2133.0

0.08 19174.0 0.02 6120.0 2117.0

0.09 18988.4 0.01 5670.0 2104.0

0.1 18734.8 0.01 5520.0 2090.0

0.11 18532.7 0.01 5310.0 2078.0

0.12 18354.2 0.01 5130.0 2061.0

0.13 18171.7 0.01 4830.0 2047.0

0.14 17960.4 0.01 4770.0 2032.0

0.15 17779.8 0.01 4531.3 2017.0

0.16 17570.1 0.01 4441.3 2003.0

0.17 17370.2 0.01 4410.0 1985.0

0.18 17203.7 0.0 4320.0 1971.0

0.19 17016.9 0.0 4290.0 1955.0

0.2 16810.6 0.0 4230.6 1937.0

0.21 16664.1 0.0 4051.3 1921.0

0.22 16488.2 0.0 3930.6 1902.0

0.23 16378.9 0.0 3900.6 1887.0

0.24 16190.8 0.0 3840.0 1873.0

0.25 15993.0 0.0 3781.3 1855.0

0.26 15828.5 0.0 3661.3 1835.0

0.27 15673.0 0.0 3571.3 1816.0

0.28 15559.5 0.0 3511.3 1800.0

0.29 15416.4 0.0 3481.3 1780.0

- Xác định số lượng phân tích cơ bản trong thị trường tiền điện tử: Hãy để dữ liệu nói cho chính nó!

- Các nghiên cứu định lượng cơ bản của vòng đồng tiền - đừng tin vào những giáo viên mờ nhạt, nói khách quan về dữ liệu!

- Một công cụ thiết yếu trong lĩnh vực giao dịch định lượng - nhà phát minh mô-đun khám phá dữ liệu định lượng

- Kiểm soát mọi thứ - giới thiệu về FMZ Phiên bản mới của Terminal giao dịch (với mã nguồn TRB Arbitrage)

- Có tất cả các thông tin về FMZ phiên bản mới của giao dịch đầu cuối (được thêm mã nguồn TRB)

- FMZ Quant: Phân tích các ví dụ thiết kế yêu cầu chung trong thị trường tiền điện tử (II)

- Làm thế nào để khai thác robot bán hàng không có não với một chiến lược tần số cao trong 80 dòng mã

- FMZ định lượng: Phân tích các trường hợp thiết kế nhu cầu phổ biến của thị trường tiền điện tử (II)

- Cách khai thác robot vô trí tuệ để bán bằng chiến lược tần số cao 80 dòng mã

- FMZ Quant: Phân tích các ví dụ thiết kế yêu cầu chung trong thị trường tiền điện tử (I)

- FMZ định lượng: Các nhu cầu phổ biến của thị trường tiền điện tử