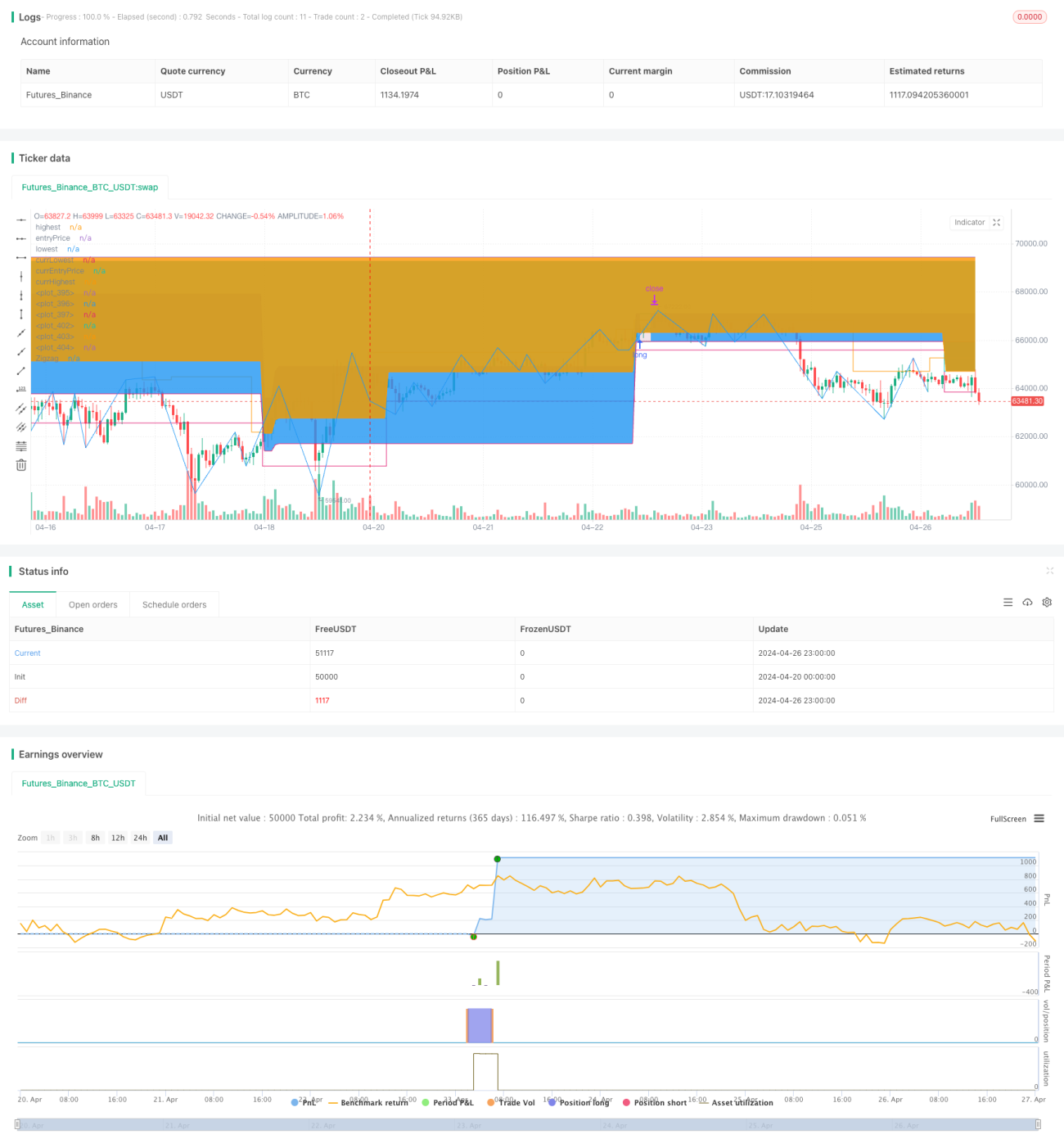

AlphaTradingBot Chiến lược giao dịch

Tổng quan

AlphaTradingBot là một chiến lược giao dịch trong ngày dựa trên chỉ báo Zigzag và dãy Fibonacci. Chiến lược này xác định xu hướng bằng cách nhận diện đỉnh cao (HH) và đáy thấp (LL) của thị trường, kết hợp với mức thoái lui và mở rộng Fibonacci để thiết lập điểm vào lệnh, chốt lời và cắt lỗ. Chiến lược chỉ hoạt động trong khoảng thời gian ngày đã định, có thể thực hiện cả lệnh mua và lệnh bán riêng biệt, có khả năng nắm bắt xu hướng và kiểm soát tỷ lệ lợi nhuận/rủi ro nhất định.

Nguyên lý chiến lược

- Sử dụng chỉ báo Zigzag để nhận diện đỉnh cao (HH), đáy thấp (LL), đáy cao hơn (HL) và đỉnh thấp hơn (LH) của thị trường.

- Khi xuất hiện HH, coi như xu hướng tăng bắt đầu, bắt đầu tìm kiếm cơ hội mua; khi xuất hiện LL, coi như xu hướng giảm bắt đầu, bắt đầu tìm kiếm cơ hội bán.

- Trong xu hướng tăng, nếu xuất hiện HL, thì lấy khoảng hình thành giữa HL và LL trước đó làm vùng thoái lui Fibonacci cho vị thế mua. Nếu giá phá vỡ đỉnh trước, thì mở lệnh mua tại vùng thoái lui 23.6%-38.2% (có thể cài đặt), cắt lỗ đặt tại mức thoái lui 61.8%, chốt lời tính theo giá trị RR (có thể cài đặt).

- Trong xu hướng giảm, nếu xuất hiện LH, thì lấy khoảng hình thành giữa LH và HH trước đó làm vùng thoái lui Fibonacci cho vị thế bán. Nếu giá phá vỡ đáy trước, thì mở lệnh bán tại vùng thoái lui 61.8%-76.4% (có thể cài đặt), cắt lỗ đặt tại mức thoái lui 38.2%, chốt lời tính theo giá trị RR (có thể cài đặt).

- Quản lý lệnh: Mỗi tín hiệu chỉ mở một lệnh, cho đến khi lệnh đó được đóng. Nếu khoản lỗ đơn lẻ đạt đến X% (có thể cài đặt) tổng tài khoản, chiến lược sẽ ngừng hoạt động.

Phân tích ưu điểm

- Khả năng bám xu hướng mạnh. Nhờ Zigzag nhận diện xu hướng hiệu quả, có thể tham gia vào giai đoạn đầu của xu hướng.

- Logic thoái lui rõ ràng. Sử dụng Fibonacci thoái lui để thiết lập vùng vào lệnh, tham gia khi xu hướng điều chỉnh, tỷ lệ thắng tương đối cao.

- Rủi ro có thể kiểm soát. Kiểm soát rủi ro mỗi giao dịch bằng cách đặt tỷ lệ thua lỗ tối đa cho mỗi lệnh, đồng thời quy tắc cắt lỗ chặt chẽ cũng đảm bảo tổng rủi ro có thể kiểm soát.

- Tỷ lệ lợi nhuận/rủi ro có thể tối ưu. Có thể điều chỉnh giá trị RR để tối ưu tỷ lệ lợi nhuận/rủi ro của chiến lược dựa trên đặc điểm thị trường và sở thích cá nhân.

Phân tích rủi ro

- Giao dịch thường xuyên. Do độ nhạy của Zigzag cao, có thể tạo ra tín hiệu thường xuyên, dẫn đến giao dịch quá mức.

- Nắm bắt xu hướng không chính xác. Xu hướng do Zigzag xác định vẫn có thể sai lệch, dẫn đến thời điểm vào lệnh chưa lý tưởng.

- Hiệu suất kém trong thị trường đi ngang. Trong thị trường đi ngang, chiến lược này có thể tạo ra nhiều giao dịch thua lỗ.

- Chu kỳ hoạt động hạn chế. Chiến lược chỉ hoạt động trong khoảng thời gian ngày được chỉ định, có thể bỏ lỡ một phần thị trường.

Hướng tối ưu hóa

- Đưa thêm các chỉ báo kỹ thuật như MA, MACD,... để nâng cao độ chính xác của việc xác định xu hướng.

- Tối ưu hóa quản lý vị thế, ví dụ điều chỉnh vị thế động theo các chỉ báo như ATR.

- Tối ưu hóa logic chốt lời cắt lỗ, ví dụ điều chỉnh điểm cắt lỗ động theo biến động thị trường.

- Đưa vào các chỉ báo tâm lý thị trường, tránh vào lệnh khi thị trường quá lạc quan hoặc bi quan.

- Nới lỏng giới hạn ngày, tăng tính phổ quát của chiến lược.

Tổng kết

AlphaTradingBot là một chiến lược giao dịch trong ngày bám xu hướng dựa trên chỉ báo zigzag và thoái lui Fibonacci. Nó xác định xu hướng thông qua các đỉnh đáy, và vào lệnh khi xu hướng điều chỉnh để theo đuổi tỷ lệ thắng và tỷ lệ lợi nhuận/rủi ro cao hơn. Ưu điểm của chiến lược này là khả năng nắm bắt xu hướng mạnh, logic thoái lui rõ ràng, rủi ro có thể đo lường, nhưng cũng tồn tại rủi ro như giao dịch quá mức, sai lệch nhận định xu hướng, hiệu suất kém trong thị trường đi ngang. Trong tương lai, có thể tối ưu hóa chiến lược này từ các khía cạnh như chỉ báo kỹ thuật, quản lý vị thế, chốt lời cắt lỗ, tâm lý thị trường,... nhằm nâng cao tính ổn định và khả năng sinh lời của chiến lược.

- 1