Preface: Why Skip Crypto and Trade TradFi?

Anyone who has run a grid strategy on crypto knows the same nightmare: the grid is set up, the price tanks, every level fills, and you're either chasing margin or getting liquidated outright. Crypto's charm is that prices can move without an upper bound — and that is exactly what kills grid strategies. Grids are built for chop; one-way moves destroy them.

Is there a class of assets that still gives you enough intraday wiggle to keep the grid firing, but doesn't routinely throw 30% or 50% melt-ups or stampedes at you? Yes — TradFi instruments.

TradFi (traditional finance) derivatives include perpetual contracts on classic assets: the S&P 500, Nasdaq, gold, crude oil, FX, and so on. Each one is anchored by real fundamentals. Equity indices are constrained by corporate earnings and Fed policy. Commodities are driven by supply and demand. FX rates are set by the relative dynamics between two sovereign economies. These assets don't 5× overnight for no reason, and they don't crater 80% over a tweet. Their prices have gravity — they can chop in the short term, but they revert to fundamentals in the long term.

That property is a near-perfect fit for grid strategies: 1%–3% of normal intraday range, enough to repeatedly trip the cells; and even in extreme moves, the grid doesn't get blown out entirely, leaving room for stops and capital management. This strategy is built on exactly that logic — it scans every TradFi pair available, picks the most actively oscillating ones, runs circulating grids on each, and automatically rotates between pairs as the volatility structure shifts.

Background: Crypto Exchanges Have Quietly Listed a New Asset Class

Over the past two years, top crypto exchanges like OKX and Bitget have quietly listed a large batch of TradFi perpetual contracts. The coverage spans US equity indices (S&P 500, Nasdaq 100), individual stocks (Apple, Nvidia, Tesla), commodities (gold, oil, natural gas), and FX (EUR, JPY). In plain English: you can now trade US stocks, gold, and FX from a crypto exchange account, 24/7, with leverage.

This matters for quants. On one hand, these instruments inherit the fundamental anchoring of traditional finance — prices don't moonshot or capitulate without reason. On the other hand, they're listed as perpetual contracts on a crypto exchange, which means familiar trading mechanics, deep liquidity, transparent fees, and an API surface identical to regular crypto pairs. They drop right into any existing quant stack.

In other words, this opens a new arbitrage surface: use crypto-native infrastructure to harvest oscillation on traditional finance assets. This strategy is purpose-built for that scenario — let the program pick the most volatile TradFi names, run grids on them, and eat the chop.

1. Selection Logic: Trade Only the Most Volatile Pairs

Whether a grid makes money is 60% determined by what you put it on. Pick the right pair and the cells trip a dozen times a day and profit compounds naturally. Pick the wrong one and the cells sit untouched for a week, locking up margin for nothing.

The strategy's selection criterion has one dimension only: average daily range over the past N daily bars.

volatility score = Σ [ (High_i − Low_i) / Close_i × 100 ] / N

Code-wise the logic is straightforward:

python

def score_symbol(info):

bars = exchange.GetRecords(info["sym"], PERIOD_D1, KLINE_COUNT + 2)

if not bars or len(bars) < 3:

return None

bars = bars[-KLINE_COUNT:]

atr_pcts = [(b["High"] - b["Low"]) / b["Close"] * 100 for b in bars if b["Close"] > 0]

avg_atr = sum(atr_pcts) / len(atr_pcts)

# Avg daily range must be at least 1.5x grid spacing, otherwise drop the symbol

if avg_atr < GRID_RATIO * 100 * 1.5:

return None

return {"sym": info["sym"], "atr": round(avg_atr, 3), "price": bars[-1]["Close"]}

The strategy periodically scans every TradFi pair, ranks them, and holds positions on the top-N by range. The entry threshold matters: average daily range has to be at least 1.5× the grid spacing, otherwise the price might not cross a single cell in a day. Anything below that is discarded immediately, so capital doesn't sit idle on a dead pair while still consuming margin.

Identifying which symbols are TradFi requires special handling. On FMZ, TradFi pairs are distinguished from regular crypto via the instCategory field:

python

def scan_tradfi():

markets = exchange.GetMarkets()

for sym, mkt in markets.items():

if not sym.endswith("USDT.swap"):

continue

info = mkt.get("Info") or {}

# instCategory != 1 means it's a TradFi pair

if int(info.get("instCategory", 1)) == 1:

continue

result.append({"sym": sym, "base": base, "cat": cat})

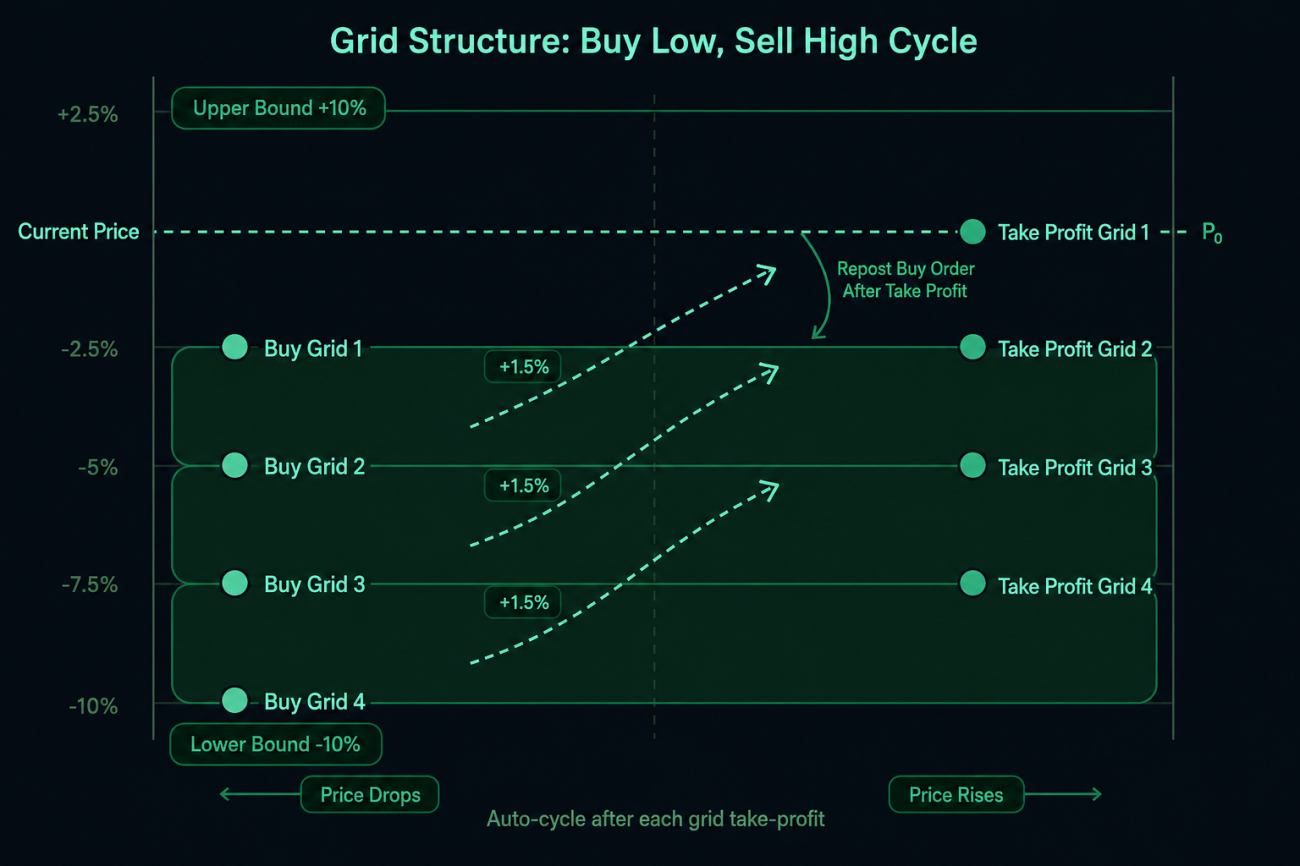

2. Grid Structure: Buy Low, Sell High, Rinse, Repeat

On each selected pair, the grid is centered on the current price and extended a fixed percentage in each direction, then divided into geometrically-spaced cells. Every cell below current price is seeded with a buy order, waiting for price to come down and fill it.

The core of grid construction:

python

def build_grid(sym, price):

low = price * (1 - LOWER_RANGE)

high = price * (1 + LOWER_RANGE)

# geometric spacing

grids, p = [], low

while p <= high * 1.001:

grids.append(round(p, g_states[sym]["pp"]))

p = p * (1 + GRID_RATIO)

for i in range(len(grids) - 1):

buy_p, sell_p = grids[i], grids[i + 1]

if buy_p < price:

oid = buy_open(sym, buy_p, GRID_VALUE) # below current price: place buy

g["status"] = "pending_buy" if oid else "skip"

else:

g["status"] = "above" # above current price: wait for price to drop

Grid sync is the strategy's main loop. It checks every cell's order status and reacts:

python

def sync(sym):

for g in grids:

if g["status"] == "pending_buy":

s, deal, avgp = check_order(g["buy_oid"])

if s == "filled":

# buy filled → immediately place take-profit sell

oid = sell_close(sym, g["sp"], ct)

g["status"] = "pending_sell"

elif g["status"] == "pending_sell":

s, deal, avgp = check_order(g["sell_oid"])

if s == "filled":

# TP filled → log profit, re-place the buy at the same level

profit = g["ct"] * cv * (avgp - g["fp"])

g_total_profit += profit

oid = buy_open(sym, g["bp"], GRID_VALUE)

g["status"] = "pending_buy"

The runtime logic is simple: price drops through a cell → buy. Price rises through the next cell up → take profit. After TP, re-seed the buy at the same level. Around and around. Order cancellation, missed TP, and other anomalies all have automatic detection and re-placement, so the strategy doesn't break on the occasional bad fill.

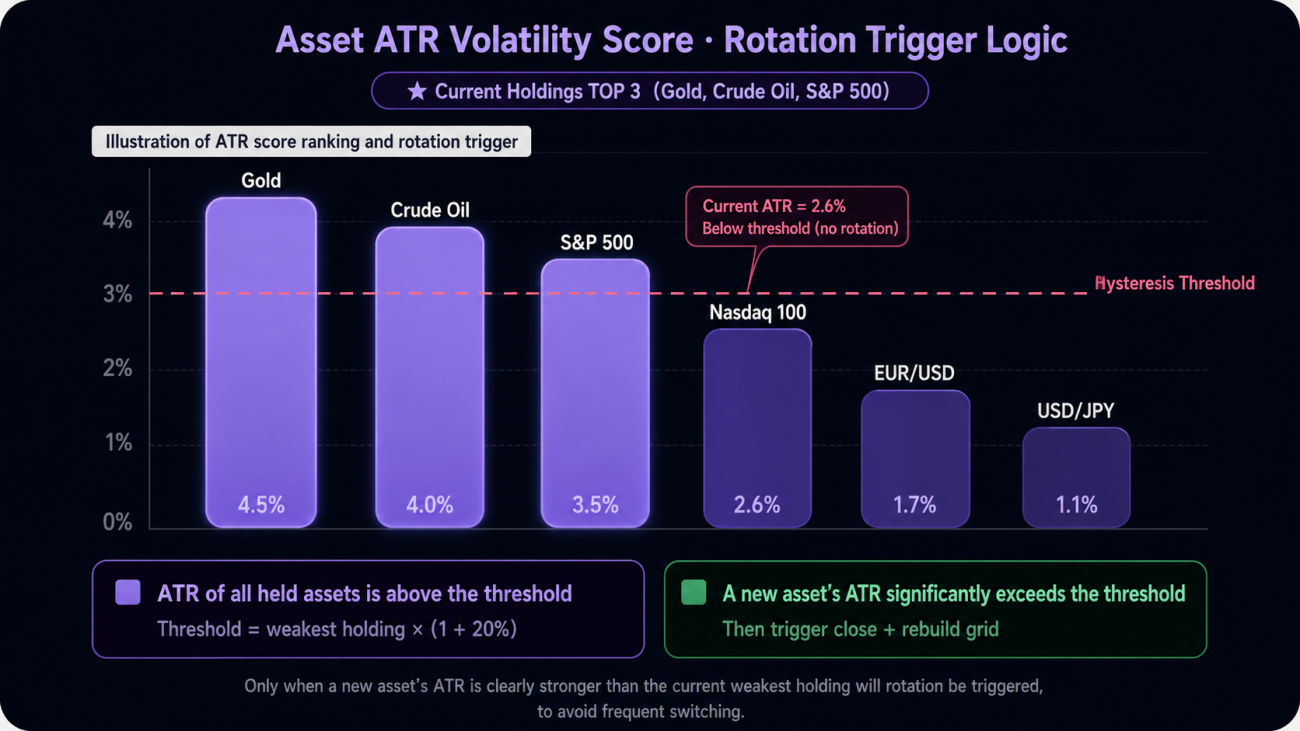

3. Smart Rotation: Always Keep Capital on the Most Active Pairs

TradFi pairs cycle their volatility regimes with macro events, earnings seasons, and policy shifts. Gold might be the most active name for a stretch; then it rolls over to oil, then to S&P futures. Lock yourself into one pair and eventually it enters a quiet phase and the cells go a full week without firing.

This strategy re-scores and re-ranks every TradFi pair on a fixed cadence (default 48 hours), then decides whether to swap out a currently-held pair. To avoid churning fees from frequent rotations on marginal differences, it uses a hysteresis mechanism:

python

def needs_rebalance(new_selected):

cur_scores = {s["sym"]: s["atr"] for s in g_score_log if s["sym"] in g_active}

for s in new_selected:

if s["sym"] in g_active:

continue

weakest_atr = min(cur_scores.values())

threshold = weakest_atr * (1 + HYSTERESIS) # must beat weakest by 20%

if s["atr"] >= threshold:

Log(f"{s['base']} ATR={s['atr']:.2f}% > threshold={threshold:.2f}%, rotating")

else:

Log(f"{s['base']} ATR={s['atr']:.2f}% < threshold={threshold:.2f}%, hysteresis holds")

Rotation only triggers when a candidate's average daily range is at least 20% above the weakest currently-held pair. The swap flow: cancel every open order on the outgoing pair, flatten all positions, then rebuild a complete grid on the incoming pair. The whole thing runs unattended.

4. Key Parameters

TOP_N— number of pairs held concurrently. Default 3; capital is spread across the three most volatile names.GRID_RATIO— grid spacing as a percentage. Default 1.5%; this is also the per-cell take-profit.GRID_VALUE— fixed USDT amount allocated per cell. Default 50. Does not scale with price level.LOWER_RANGE— price range the grid covers. Default ±10% around current price.REBALANCE_HOURS— rotation evaluation cadence. Default 48 hours.HYSTERESIS— rotation threshold. Default 20%, prevents excessive churning.LEVERAGE— leverage multiplier. Recommended ≤ 3×.STOP_LOSS_RATIO— global stop-loss. When account loss exceeds this fraction of starting equity, auto-flatten and halt. Default 30%.KLINE_COUNT— number of daily bars used for scoring. Default 20.EXCLUDE_SYMBOLS— blacklist; comma-separated codes the strategy should never touch.

5. Risk Controls

Global stop-loss is the final safety net. When account equity drawdown exceeds the configured fraction of starting equity, the strategy cancels everything, flattens everything, and halts all subsequent action:

python

def check_stop():

acc = exchange.GetAccount()

loss = (g_init_equity - acc.Equity) / g_init_equity

if loss >= STOP_LOSS_RATIO:

Log(f"Stop-loss triggered! Loss={loss*100:.1f}% → close all and halt")

for sym in list(g_active):

close_all(sym)

g_state = "STOP"

The selection phase's entry filter screens out low-volatility pairs, so every name that enters the strategy has enough intraday range to actually drive the grid. The blacklist lets you manually exclude pairs with poor liquidity, abnormal spreads, or unstable behavior. All order prices and sizes are strictly aligned to the exchange's precision requirements, eliminating rejected orders at the source. Capital is evenly distributed across pairs, so a loss on one pair doesn't drag the rest of the book down with it.

6. Suitable Regimes and Things to Watch

The strategy works best in choppy, range-bound markets. When a target pair oscillates inside a band, the cells get hit at high frequency and P&L accumulates linearly with time — almost no manual intervention required.

A few things to watch:

- If price runs one-way and breaks below the grid's lower bound, every buy fill is stuck holding inventory until price recovers or the global stop triggers.

- Some TradFi pairs have sharply reduced liquidity during off-hours (e.g. when US equities are closed). Orders sitting unfilled for long stretches is normal.

GRID_RATIOshould be sized relative to the target pair's average daily range — somewhere between 1/3 and 1/2 of the daily range. Too wide and the trigger frequency drops; too tight and fees eat the profit.- Keep leverage at 3× or below. High leverage in an extreme move accelerates losses faster than the stop-loss can react.

Closing

The core logic of this strategy can be stated in one sentence: keep capital on the highest-volatility TradFi pairs at all times, and let the grid be friends with time. Selection, grid construction, rotation, and risk control — four modules, chained, fully automated. The fundamental anchoring of TradFi assets guarantees prices don't drift off to infinity, while the programmatic volatility filter keeps capital allocated to the highest-efficiency names. With reasonable parameters, the strategy can produce steady grid returns across most market regimes, while the stop-loss and hysteresis mechanisms keep downside risk inside an acceptable envelope.

This article is an original strategy write-up from the FMZ Quant platform, intended for educational discussion only. It does not constitute investment advice.

- 1