Einfache Rasterstrategie in Python Version

Schriftsteller:Lydia., Erstellt: 2022-12-23 21:00:45, Aktualisiert: 2023-09-20 11:17:48

Einfache Rasterstrategie in Python Version

Es gibt nicht viele Python-Strategien auf dem Strategie-Quadrat. Hier wird eine Python-Version der Gitterstrategie geschrieben. Das Prinzip der Strategie ist sehr einfach. Eine Reihe von Gitterknoten werden durch eine feste Preisdistanz innerhalb einer Preisspanne erzeugt. Wenn der Markt sich ändert und der Preis eine Gitterknotenpreisposition erreicht, wird eine Kauforder platziert. Wenn die Bestellung geschlossen wird, dh nach dem Preis der ausstehenden Bestellung plus der Gewinnspanne, warten Sie auf eine Verkaufsorder, um die Position zu schließen.

Es versteht sich von selbst, dass das Risiko der Gitterstrategie darin besteht, dass jede Gitterstrategie eine Wette ist, dass der Preis in einem bestimmten Bereich schwankt. Sobald der Preis aus dem Gitterbereich herausbricht, kann dies zu ernsthaften schwimmenden Verlusten führen. Daher ist der Zweck des Schreibens dieser Strategie, eine Referenz für Python-Strategie-Schreibideen oder Programmdesign zu bieten. Diese Strategie wird nur zum Lernen verwendet und kann im echten Bot riskant sein.

Die Erläuterung der Strategieideen ist direkt in den Kommentaren zum Strategiecode geschrieben.

Strategiecode

'''backtest

start: 2019-07-01 00:00:00

end: 2020-01-03 00:00:00

period: 1m

exchanges: [{"eid":"OKEX","currency":"BTC_USDT"}]

'''

import json

# Parameters

beginPrice = 5000 # Grid interval begin price

endPrice = 8000 # Grid interval end price

distance = 20 # Price distance of each grid node

pointProfit = 50 # Profit spread per grid node

amount = 0.01 # Number of pending orders per grid node

minBalance = 300 # Minimum fund balance of the account (at the time of purchase)

# Global variables

arrNet = []

arrMsg = []

acc = None

def findOrder (orderId, NumOfTimes, ordersList = []) :

for j in range(NumOfTimes) :

orders = None

if len(ordersList) == 0:

orders = _C(exchange.GetOrders)

else :

orders = ordersList

for i in range(len(orders)):

if orderId == orders[i]["Id"]:

return True

Sleep(1000)

return False

def cancelOrder (price, orderType) :

orders = _C(exchange.GetOrders)

for i in range(len(orders)) :

if price == orders[i]["Price"] and orderType == orders[i]["Type"]:

exchange.CancelOrder(orders[i]["Id"])

Sleep(500)

def checkOpenOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "pending" :

orderId = exchange.Sell(arrNet[i]["coverPrice"], arrNet[i]["amount"], arrNet[i], ticker)

if orderId :

arrNet[i]["state"] = "cover"

arrNet[i]["id"] = orderId

else :

# Cancel

cancelOrder(arrNet[i]["coverPrice"], ORDER_TYPE_SELL)

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

def checkCoverOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "cover" :

arrNet[i]["id"] = -1

arrNet[i]["state"] = "idle"

Log(arrNet[i], "The node closes the position and resets to the idle state.", "#FF0000")

def onTick () :

global arrNet, arrMsg, acc

ticker = _C(exchange.GetTicker) # Get the latest current ticker every time

for i in range(len(arrNet)): # Iterate through all grid nodes, find out the position where you need to pend a buy order according to the current market, and pend a buy order.

if i != len(arrNet) - 1 and arrNet[i]["state"] == "idle" and ticker.Sell > arrNet[i]["price"] and ticker.Sell < arrNet[i + 1]["price"]:

acc = _C(exchange.GetAccount)

if acc.Balance < minBalance : # If there is not enough money left, you can only jump out and do nothing.

arrMsg.append("Insufficient funds" + json.dumps(acc) + "!" + ", time:" + _D())

break

orderId = exchange.Buy(arrNet[i]["price"], arrNet[i]["amount"], arrNet[i], ticker) # Pending buy orders

if orderId :

arrNet[i]["state"] = "pending" # Update the grid node status and other information if the buy order is successfully pending

arrNet[i]["id"] = orderId

else :

# Cancel h/the order

cancelOrder(arrNet[i]["price"], ORDER_TYPE_BUY) # Cancel orders by using the cancel function

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

Sleep(1000)

orders = _C(exchange.GetOrders)

checkOpenOrders(orders, ticker) # Check the status of all buy orders and process them according to the changes.

Sleep(1000)

orders = _C(exchange.GetOrders)

checkCoverOrders(orders, ticker) # Check the status of all sell orders and process them according to the changes.

# The following information about the construction status bar can be found in the FMZ API documentation.

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

while len(arrMsg) > 20 :

arrMsg.pop(0)

for i in range(len(arrMsg)) :

errTbl["rows"].append([i, json.dumps(arrMsg[i])])

for i in range(len(orders)) :

orderTbl["rows"].append([i, json.dumps(orders[i])])

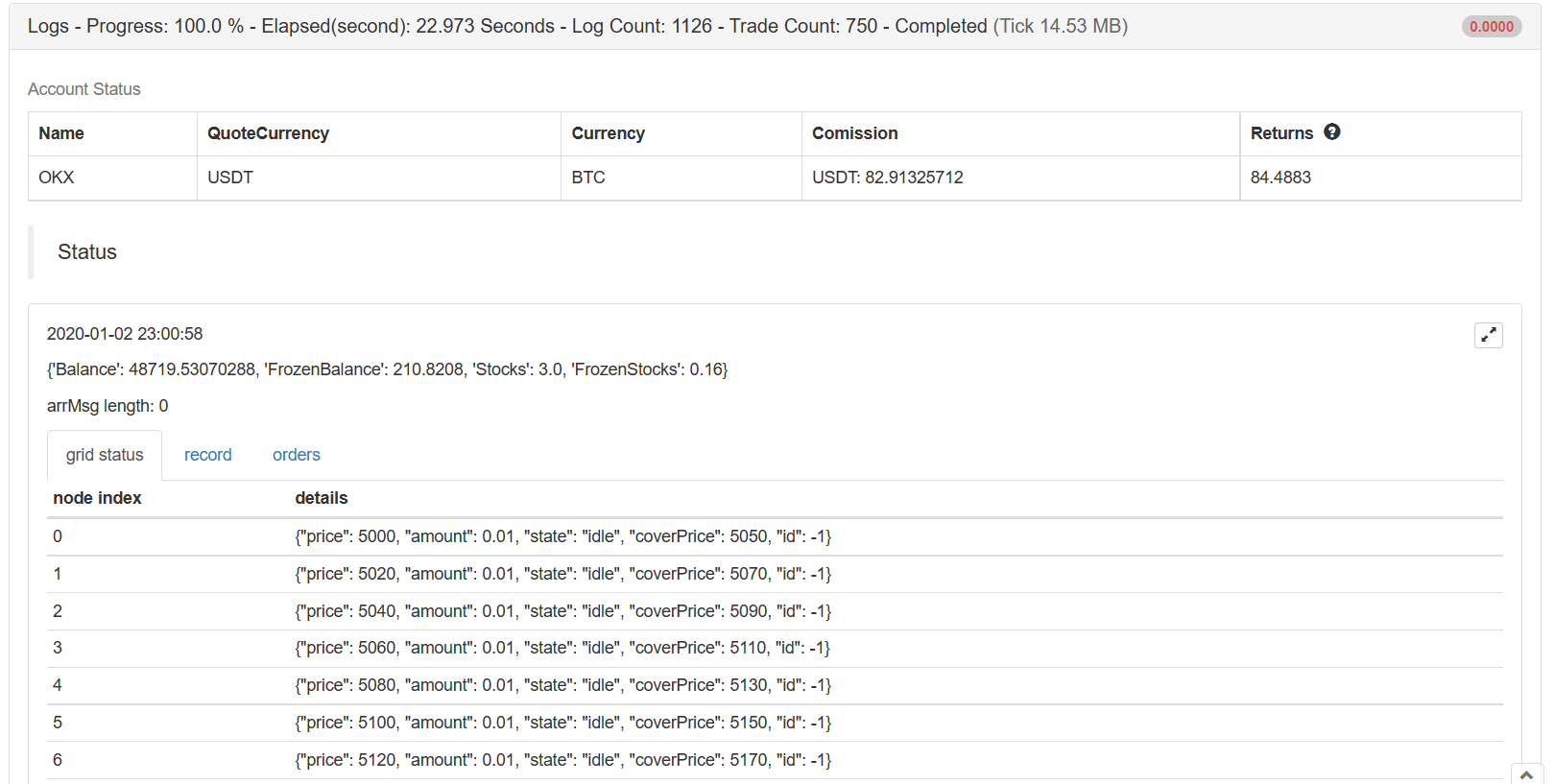

LogStatus(_D(), "\n", acc, "\n", "arrMsg length:", len(arrMsg), "\n", "`" + json.dumps([tbl, errTbl, orderTbl]) + "`")

def main (): # Strategy execution starts here

global arrNet

for i in range(int((endPrice - beginPrice) / distance)): # The for loop constructs a data structure for the grid based on the parameters, a list that stores each grid node, with the following information for each grid node:

arrNet.append({

"price" : beginPrice + i * distance, # Price of the node

"amount" : amount, # Number of orders

"state" : "idle", # pending / cover / idle # Node Status

"coverPrice" : beginPrice + i * distance + pointProfit, # Node closing price

"id" : -1, # ID of the current order related to the node

})

while True: # After the grid data structure is constructed, enter the main strategy loop

onTick() # Processing functions on the main loop, the main processing logic

Sleep(500) # Control polling frequency

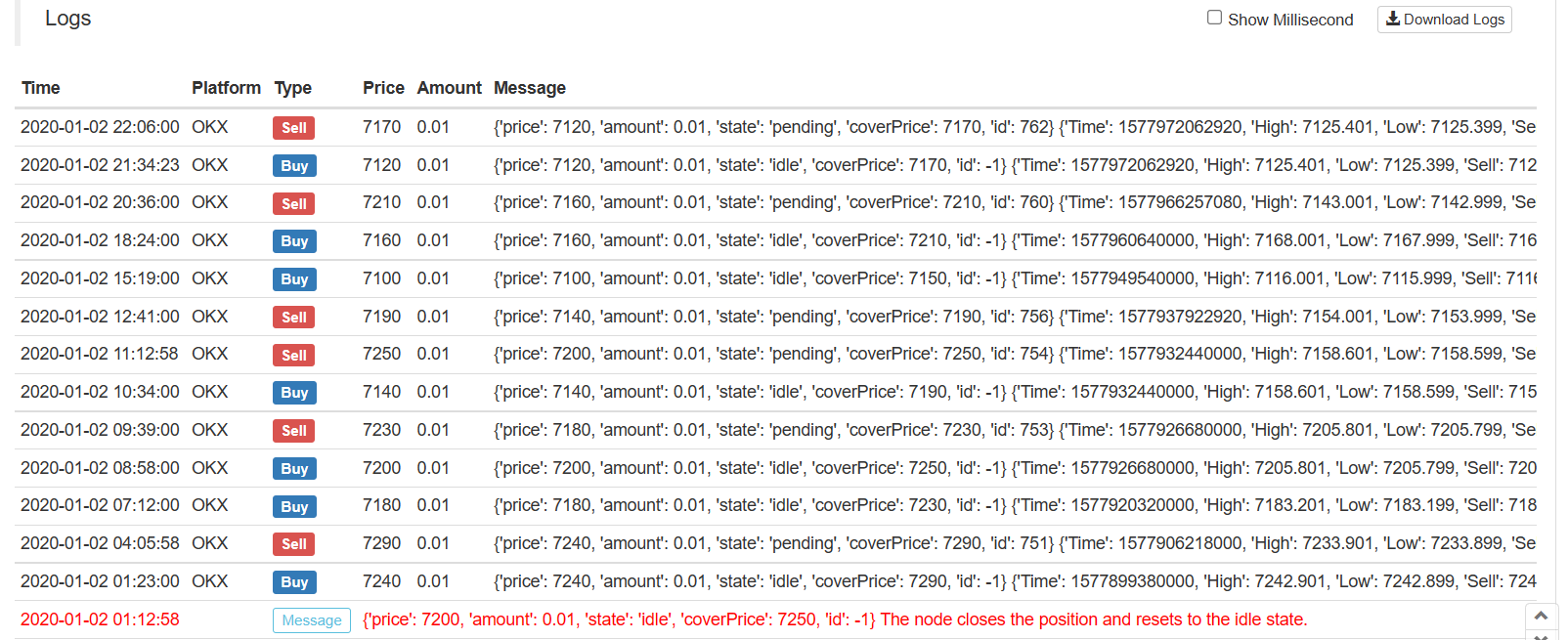

Der Hauptgedanke der Strategie besteht darin, die aktuelle Liste der von derGetOrdersAnalyse der Änderungen der ausstehenden Aufträge (ob sie geschlossen sind oder nicht), aktualisiere die Netzdatenstruktur und führe nachfolgende Operationen durch. Darüber hinaus werden ausstehende Aufträge nicht storniert, bis die Transaktion abgeschlossen ist, auch wenn der Preis abweicht, da der digitale Währungsmarkt oft die Situation von Pins hat, können diese ausstehenden Aufträge auch die Aufträge von Pins erhalten (wenn die Anzahl der ausstehenden Aufträge in der Börse begrenzt ist, wird sie angepasst).

Strategie-Datenvisualisierung verwendet dieLogStatusFunktion zur Echtzeitanzeige der Daten in der Statusleiste.

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

Die erste Tabelle zeigt die Informationen jedes Knotenpunktes in der aktuellen Gitterdatenstruktur, die zweite Tabelle zeigt abnorme Informationen und die dritte Tabelle zeigt die tatsächlichen Auflistungsinformationen der Börse.

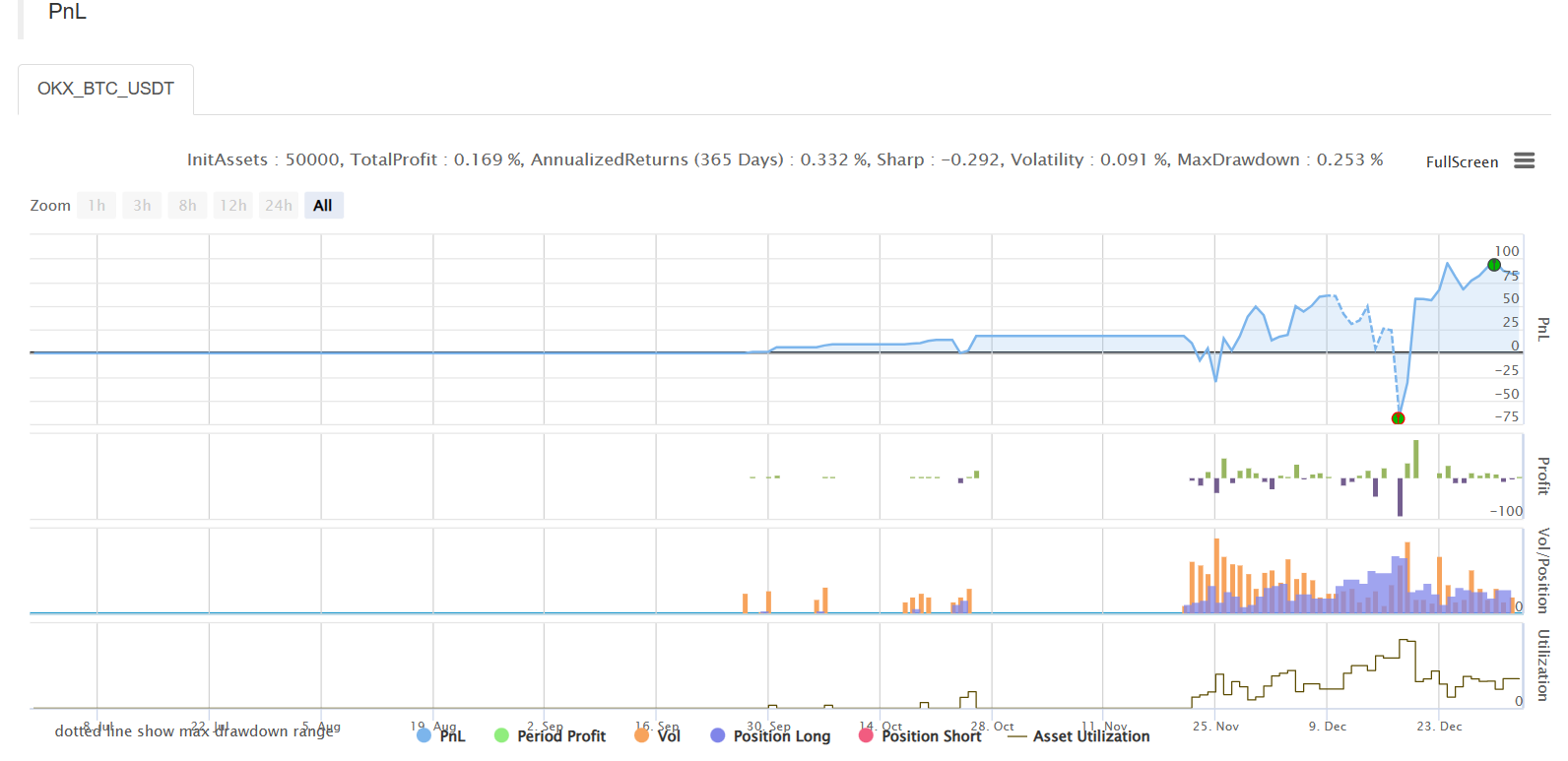

Zurückprüfung

Strategieadresse

Die Strategie ist nur für Lern- und Backtestzwecke gedacht und kann optimiert und aktualisiert werden, wenn Sie interessiert sind.

- Quantifizierung der Fundamentalanalyse auf dem Kryptowährungsmarkt: Die Daten sprechen für sich!

- Die Quantifizierung der Kernforschung der Münzkreise - nicht mehr auf alle Arten von Lehrern zu vertrauen, die überzeugt sind, dass die Daten objektiv sind!

- Ein wichtiges Werkzeug im Bereich der Quantitative Transaktionen - der Erfinder der Quantitative Data Exploration Module

- Mastering Everything - Einführung in FMZ Neue Version des Handelsterminals (mit TRB Arbitrage Source Code)

- Die neue Version des FMZ-Trading-Terminals ist verfügbar.

- FMZ Quant: Eine Analyse von gemeinsamen Anforderungen Designbeispielen auf dem Kryptowährungsmarkt (II)

- Wie man Hirnlose Verkaufs-Bots mit einer Hochfrequenz-Strategie in 80 Codezeilen ausnutzt

- FMZ-Quantifizierung: Analyse von Designbeispielen für häufige Bedürfnisse im Kryptowährungsmarkt (II)

- Wie man Hirnlose Roboter ausbeuten und verkaufen kann mit einer 80-Zeilen-code-Hochfrequenz-Strategie

- FMZ Quant: Eine Analyse von gemeinsamen Anforderungen Designbeispielen auf dem Kryptowährungsmarkt (I)

- FMZ-Quantifizierung: Analyse von Designbeispielen für häufige Bedürfnisse im Kryptowährungsmarkt