Lehren Sie, eine K-Linie Synthese-Funktion in der Python-Version zu schreiben

Schriftsteller:Lydia., Erstellt: 2022-12-26 09:28:58, Aktualisiert: 2023-09-20 09:48:46

Lehren Sie, eine K-Linie Synthese-Funktion in der Python-Version zu schreiben

Bei der Erstellung und Verwendung von Strategien verwenden wir oft einige selten verwendete K-Linien-Periodendaten. Allerdings liefern Austausch und Datenquellen keine Daten zu diesen Perioden. Es kann nur durch die Verwendung von Daten mit einer vorhandenen Periode synthetisiert werden. Der synthetisierte Algorithmus hat bereits eine JavaScript-Version (VerbindungEs ist einfach, ein Stück JavaScript-Code in Python zu transplantieren. Als nächstes schreiben wir eine Python-Version des K-Line-Synthese-Algorithmus.

JavaScript-Version

function GetNewCycleRecords (sourceRecords, targetCycle) { // K-line synthesis function

var ret = []

// Obtain the period of the source K-line data first

if (!sourceRecords || sourceRecords.length < 2) {

return null

}

var sourceLen = sourceRecords.length

var sourceCycle = sourceRecords[sourceLen - 1].Time - sourceRecords[sourceLen - 2].Time

if (targetCycle % sourceCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

throw "targetCycle is not an integral multiple of sourceCycle."

}

if ((1000 * 60 * 60) % targetCycle != 0 && (1000 * 60 * 60 * 24) % targetCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

throw "targetCycle cannot complete the cycle."

}

var multiple = targetCycle / sourceCycle

var isBegin = false

var count = 0

var high = 0

var low = 0

var open = 0

var close = 0

var time = 0

var vol = 0

for (var i = 0 ; i < sourceLen ; i++) {

// Get the time zone offset value

var d = new Date()

var n = d.getTimezoneOffset()

if (((1000 * 60 * 60 * 24) - sourceRecords[i].Time % (1000 * 60 * 60 * 24) + (n * 1000 * 60)) % targetCycle == 0) {

isBegin = true

}

if (isBegin) {

if (count == 0) {

high = sourceRecords[i].High

low = sourceRecords[i].Low

open = sourceRecords[i].Open

close = sourceRecords[i].Close

time = sourceRecords[i].Time

vol = sourceRecords[i].Volume

count++

} else if (count < multiple) {

high = Math.max(high, sourceRecords[i].High)

low = Math.min(low, sourceRecords[i].Low)

close = sourceRecords[i].Close

vol += sourceRecords[i].Volume

count++

}

if (count == multiple || i == sourceLen - 1) {

ret.push({

High : high,

Low : low,

Open : open,

Close : close,

Time : time,

Volume : vol,

})

count = 0

}

}

}

return ret

}

Es gibt JavaScript-Algorithmen. Python kann Zeile für Zeile übersetzt und transplantiert werden. Wenn Sie auf JavaScript-Eingebettete Funktionen oder inhärente Methoden stoßen, können Sie zu Python gehen, um die entsprechenden Methoden zu finden. Daher ist die Migration einfach.

Die Algorithmuslogik ist genau die gleiche, außer dass JavaScript Funktion Anrufevar n=d.getTimezoneOffset(). Wenn Sie auf Python migrieren,n=time.altzonein Python

Migrationscode für Python:

import time

def GetNewCycleRecords(sourceRecords, targetCycle):

ret = []

# Obtain the period of the source K-line data first

if not sourceRecords or len(sourceRecords) < 2 :

return None

sourceLen = len(sourceRecords)

sourceCycle = sourceRecords[-1]["Time"] - sourceRecords[-2]["Time"]

if targetCycle % sourceCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

raise "targetCycle is not an integral multiple of sourceCycle."

if (1000 * 60 * 60) % targetCycle != 0 and (1000 * 60 * 60 * 24) % targetCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

raise "targetCycle cannot complete the cycle."

multiple = targetCycle / sourceCycle

isBegin = False

count = 0

barHigh = 0

barLow = 0

barOpen = 0

barClose = 0

barTime = 0

barVol = 0

for i in range(sourceLen) :

# Get the time zone offset value

n = time.altzone

if ((1000 * 60 * 60 * 24) - (sourceRecords[i]["Time"] * 1000) % (1000 * 60 * 60 * 24) + (n * 1000)) % targetCycle == 0 :

isBegin = True

if isBegin :

if count == 0 :

barHigh = sourceRecords[i]["High"]

barLow = sourceRecords[i]["Low"]

barOpen = sourceRecords[i]["Open"]

barClose = sourceRecords[i]["Close"]

barTime = sourceRecords[i]["Time"]

barVol = sourceRecords[i]["Volume"]

count += 1

elif count < multiple :

barHigh = max(barHigh, sourceRecords[i]["High"])

barLow = min(barLow, sourceRecords[i]["Low"])

barClose = sourceRecords[i]["Close"]

barVol += sourceRecords[i]["Volume"]

count += 1

if count == multiple or i == sourceLen - 1 :

ret.append({

"High" : barHigh,

"Low" : barLow,

"Open" : barOpen,

"Close" : barClose,

"Time" : barTime,

"Volume" : barVol,

})

count = 0

return ret

# Test

def main():

while True:

r = exchange.GetRecords()

r2 = GetNewCycleRecords(r, 1000 * 60 * 60 * 4)

ext.PlotRecords(r2, "r2")

Sleep(1000)

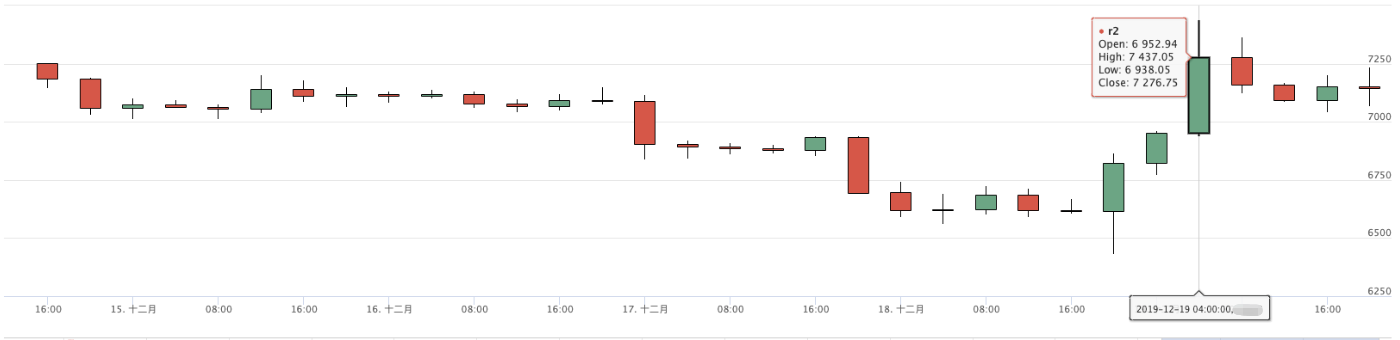

Prüfung

Marktdiagramm von Huobi

4-Stunden-Diagramm der Backtest-Synthese

Der oben genannte Code dient nur als Referenz; wenn er in spezifischen Strategien verwendet wird, wird er entsprechend den spezifischen Anforderungen geändert und getestet. Wenn es einen Fehler oder Verbesserungsvorschlag gibt, hinterlassen Sie bitte eine Nachricht. Vielen Dank. o^_^ o

- Quantifizierung der Fundamentalanalyse auf dem Kryptowährungsmarkt: Die Daten sprechen für sich!

- Die Quantifizierung der Kernforschung der Münzkreise - nicht mehr auf alle Arten von Lehrern zu vertrauen, die überzeugt sind, dass die Daten objektiv sind!

- Ein wichtiges Werkzeug im Bereich der Quantitative Transaktionen - der Erfinder der Quantitative Data Exploration Module

- Mastering Everything - Einführung in FMZ Neue Version des Handelsterminals (mit TRB Arbitrage Source Code)

- Die neue Version des FMZ-Trading-Terminals ist verfügbar.

- FMZ Quant: Eine Analyse von gemeinsamen Anforderungen Designbeispielen auf dem Kryptowährungsmarkt (II)

- Wie man Hirnlose Verkaufs-Bots mit einer Hochfrequenz-Strategie in 80 Codezeilen ausnutzt

- FMZ-Quantifizierung: Analyse von Designbeispielen für häufige Bedürfnisse im Kryptowährungsmarkt (II)

- Wie man Hirnlose Roboter ausbeuten und verkaufen kann mit einer 80-Zeilen-code-Hochfrequenz-Strategie

- FMZ Quant: Eine Analyse von gemeinsamen Anforderungen Designbeispielen auf dem Kryptowährungsmarkt (I)

- FMZ-Quantifizierung: Analyse von Designbeispielen für häufige Bedürfnisse im Kryptowährungsmarkt