Estrategia EMV de volatilidad simple

El autor:La bondad, Creado: 2020-07-01 10:39:17, Actualizado: 2023-10-28 15:26:49

Resumen de las actividades

A diferencia de otros indicadores técnicos,

La EMV de volatilidad simple está diseñada de acuerdo con el principio de gráfico de volumen igual y gráfico comprimido. Su concepto central es: el precio del mercado consumirá mucha energía solo cuando la tendencia gire o esté a punto de girar, y el rendimiento externo es que el volumen de negociación se vuelve más grande. Cuando el precio está subiendo, no consumirá demasiada energía debido al efecto de impulso. Aunque esta idea es contraria a la opinión de que tanto la cantidad como el aumento del precio, tiene sus propias características únicas.

Fórmula para el cálculo de la EMV

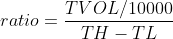

Paso 1: Calcular mov_mid

Entre ellos, TH representa el precio más alto del día, TL representa el precio más bajo del día, YH representa el precio más alto del día anterior y YL representa el precio más bajo del día anterior.

Paso 2: Calcular la proporción

Entre ellos, TVOL representa el volumen de operaciones del día, TH representa el precio más alto del día y TL representa el precio más bajo del día.

Paso 3: Calcular el valor de emisión

Uso de VEM

El autor de EMV cree que el gran aumento se acompaña de un rápido agotamiento de la energía, y el aumento a menudo no dura demasiado tiempo; por el contrario, el volumen moderado, que puede ahorrar cierta cantidad de energía, a menudo hace que el aumento dure más tiempo. Una vez que se forma una tendencia al alza, un menor volumen de negociación puede empujar los precios hacia arriba, y el valor de EMV aumentará. Una vez que se forma el mercado de tendencia bajista, a menudo se acompaña de un declive infinito o pequeño, y el valor de EMV disminuirá. Si el precio está en un mercado volátil o los aumentos y caídas de precios se acompañan de un gran volumen, el valor de EMV también estará cerca de cero.

El uso de EMV es bastante simple, solo mira si el EMV cruza el eje cero. Cuando el EMV está por debajo de 0, representa un mercado débil; cuando el EMV está por encima de 0, representa un mercado fuerte. Cuando el EMV cambia de negativo a positivo, debe comprarse; cuando el EMV cambia de positivo a negativo, debe venderse. Su característica es que no solo puede evitar el mercado de choque en el mercado, sino también entrar en el mercado a tiempo cuando comienza el mercado de tendencia. Sin embargo, debido a que el EMV refleja el cambio de volumen cuando los precios cambian, solo tiene un efecto en las tendencias a medio y largo plazo.

Realización de la estrategia

Paso 1: redactar un marco estratégico

# Strategy main function

def onTick():

pass

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

FMZ.COMEn primer lugar, es necesario definir unamainFunción yonTickLa funciónmainFunción es la función de entrada de la estrategia, y el programa ejecutará la línea de código por línea de lamainEn el caso de losmainFunción, escriba unwhileel bucle y ejecutar repetidamente elonTickTodo el código básico de la estrategia está escrito en elonTick function.

Paso 2: Obtener datos de posición

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

Porque en esta estrategia, sólo se utiliza el número de posiciones en tiempo real, con el fin de facilitar el mantenimiento,get_positionSi la posición actual es larga, devuelve un número positivo, y si la posición actual es corta, devuelve un número negativo.

Paso 3: Obtener datos de la línea K

exchange.SetContractType('IH000') # Subscribe to futures variety

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

Antes de obtener datos específicos de la línea K, primero debe suscribirse a un contrato comercial específico, utilizar elSetContractTypeFunción deFMZ.COMSi desea saber otra información sobre el contrato, también puede utilizar una variable para recibir estos datos.GetRecordsfunción para obtener datos de línea K, porque el devuelto es una matriz, por lo que usamos la variablebars_arrpara aceptarlo.

Paso 4: Calcular el valor de emisión

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

Aquí, no usamos el precio más reciente para calcular el valor de EMV, sino que usamos la línea K de corriente relativamente rezagada para emitir la señal y colocar una línea K para emitir una orden. El propósito de esto es hacer que la prueba posterior esté más cerca del comercio real. Sabemos que aunque el software de comercio cuantitativo ahora es muy avanzado, todavía es difícil simular completamente el entorno de tick de precio real, especialmente cuando se enfrenta a la prueba posterior de datos largos de nivel de barra, por lo que se utiliza este método de compromiso.

Paso 5: Posición de las órdenes

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

Antes de colocar el pedido, necesitamos determinar dos datos, uno es el precio del pedido y el otro es el estado de la posición actual. El precio de colocar un pedido es muy simple, sólo utilizar el precio de cierre actual para agregar o restar el precio mínimo de cambio de la variedad.get_positionFinalmente, la posición se abre y cierra de acuerdo con la relación posicional entre el EMV y el eje cero.

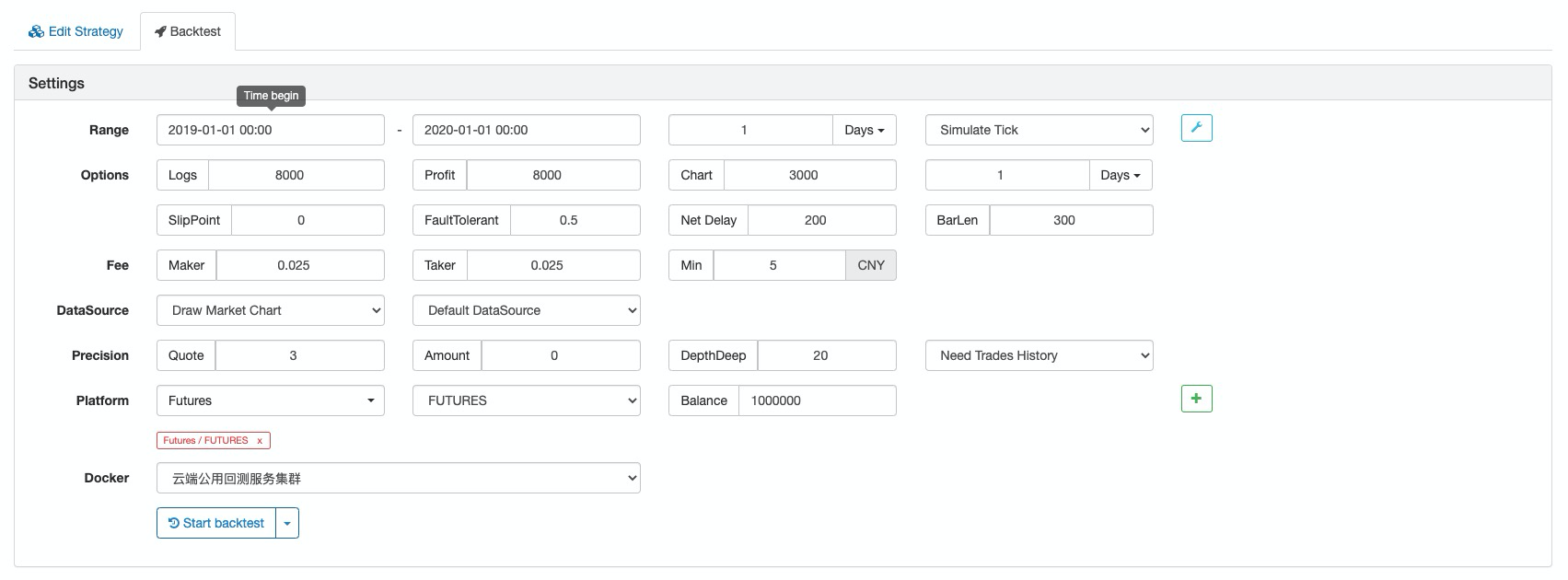

Prueba posterior de la estrategia

Configuración de pruebas de retroceso

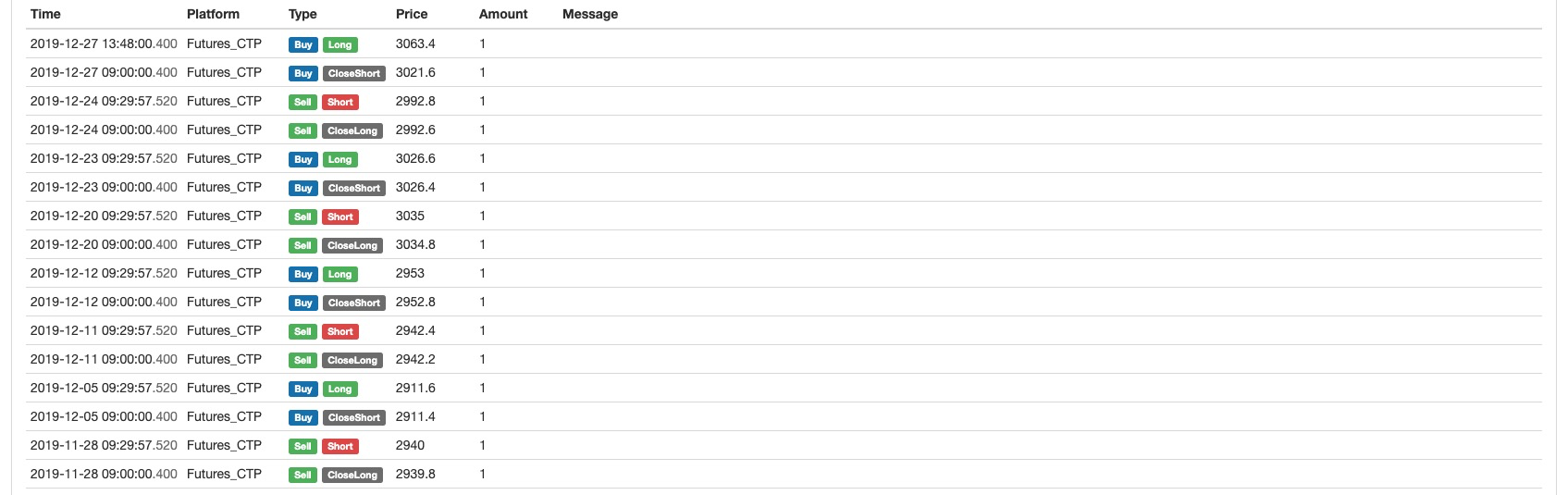

Registro de pruebas de retroceso

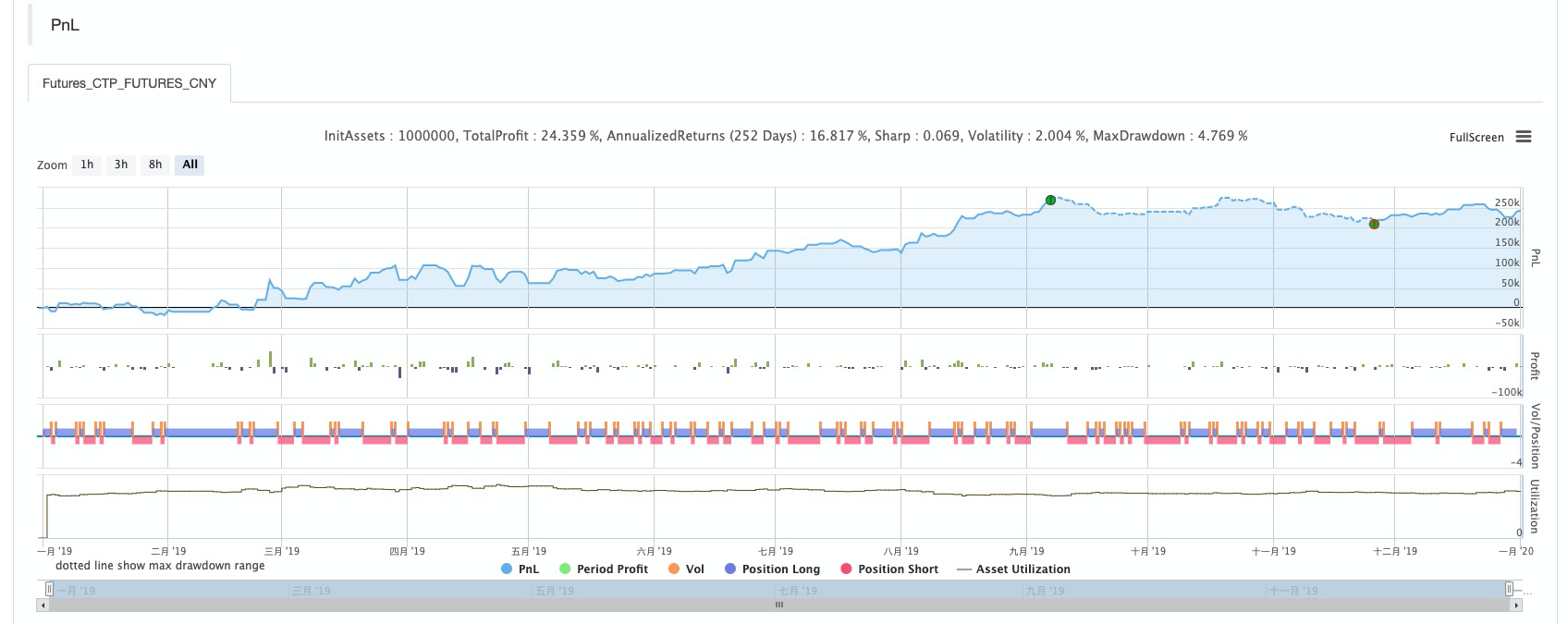

Curva del capital

Estrategia completa

# Backtest configuration

'''backtest

start: 2019-01-01 00:00:00

end: 2020-01-01 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

'''

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

# Strategy main function

def onTick():

# retrieve data

exchange.SetContractType('IH000') # Subscribe to futures

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

# Calculate emv

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

# Placing orders

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

La estrategia completa se ha publicado en el cuadrado de estrategia de laFMZ.COMpágina web, y se puede utilizar haciendo clic en copiar.https://www.fmz.com/strategy/213636

En resumen

A través de este curso de estudio, podemos ver que EMV es contrario a los comerciantes ordinarios, pero no es irrazonable. Debido a que EMV introduce datos de volumen, es más eficaz que otros indicadores técnicos que utilizan cálculos de precios para averiguar qué hay detrás del precio. Cada estrategia tiene características diferentes. Solo al comprender completamente las ventajas y desventajas de diferentes estrategias y eliminar la escoria y extraer su esencia podemos ir más lejos del éxito.

- Cuantificar el análisis fundamental en el mercado de criptomonedas: ¡Deja que los datos hablen por sí mismos!

- La investigación cuantitativa básica del círculo monetario - ¡No confíes más en los profesores de idiomas, los datos hablan objetivamente!

- Una herramienta esencial en el campo de la transacción cuantitativa - inventor de módulos de exploración de datos cuantitativos

- Dominarlo todo - Introducción a FMZ Nueva versión de la terminal de negociación (con el código fuente de TRB Arbitrage)

- Conozca todo acerca de la nueva versión del terminal de operaciones de FMZ (con código de código de TRB)

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (II)

- Cómo explotar robots de venta sin cerebro con una estrategia de alta frecuencia en 80 líneas de código

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (II)

- Cómo utilizar una estrategia de alta frecuencia de 80 líneas de código para explotar y vender robots sin cerebro

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (I)

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (1)