पायथन संस्करण में सरल ग्रिड रणनीति

लेखक:लिडिया, बनाया गयाः 2022-12-23 21:00:45, अद्यतन किया गयाः 2023-09-20 11:17:48

पायथन संस्करण में सरल ग्रिड रणनीति

रणनीति वर्ग पर कई पायथन रणनीतियाँ नहीं हैं। यहाँ ग्रिड रणनीति का एक पायथन संस्करण लिखा गया है। रणनीति का सिद्धांत बहुत सरल है। ग्रिड नोड्स की एक श्रृंखला एक मूल्य सीमा के भीतर एक निश्चित मूल्य दूरी द्वारा उत्पन्न की जाती है। जब बाजार बदलता है और कीमत ग्रिड नोड मूल्य स्थिति तक पहुंच जाती है, तो एक खरीद आदेश रखा जाता है। जब आदेश बंद हो जाता है, यानी लंबित आदेश की कीमत प्लस लाभ स्प्रेड के अनुसार, स्थिति को बंद करने के लिए एक बिक्री आदेश लंबित करें। निर्धारित मूल्य सीमा के भीतर उतार-चढ़ाव को पकड़ें।

यह कहने की जरूरत नहीं है कि ग्रिड रणनीति का जोखिम यह है कि किसी भी ग्रिड-प्रकार की रणनीति एक शर्त है कि कीमत एक निश्चित सीमा में उतार-चढ़ाव करती है। एक बार कीमत ग्रिड सीमा से बाहर निकल जाती है, तो यह गंभीर फ्लोटिंग नुकसान का कारण बन सकती है। इसलिए, इस रणनीति को लिखने का उद्देश्य पायथन रणनीति लेखन विचारों या कार्यक्रम डिजाइन के लिए संदर्भ प्रदान करना है। यह रणनीति केवल सीखने के लिए उपयोग की जाती है, और यह वास्तविक बॉट में जोखिम भरा हो सकता है।

रणनीतिक विचारों की व्याख्या सीधे रणनीतिक कोड टिप्पणियों में लिखी गई है।

रणनीति कोड

'''backtest

start: 2019-07-01 00:00:00

end: 2020-01-03 00:00:00

period: 1m

exchanges: [{"eid":"OKEX","currency":"BTC_USDT"}]

'''

import json

# Parameters

beginPrice = 5000 # Grid interval begin price

endPrice = 8000 # Grid interval end price

distance = 20 # Price distance of each grid node

pointProfit = 50 # Profit spread per grid node

amount = 0.01 # Number of pending orders per grid node

minBalance = 300 # Minimum fund balance of the account (at the time of purchase)

# Global variables

arrNet = []

arrMsg = []

acc = None

def findOrder (orderId, NumOfTimes, ordersList = []) :

for j in range(NumOfTimes) :

orders = None

if len(ordersList) == 0:

orders = _C(exchange.GetOrders)

else :

orders = ordersList

for i in range(len(orders)):

if orderId == orders[i]["Id"]:

return True

Sleep(1000)

return False

def cancelOrder (price, orderType) :

orders = _C(exchange.GetOrders)

for i in range(len(orders)) :

if price == orders[i]["Price"] and orderType == orders[i]["Type"]:

exchange.CancelOrder(orders[i]["Id"])

Sleep(500)

def checkOpenOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "pending" :

orderId = exchange.Sell(arrNet[i]["coverPrice"], arrNet[i]["amount"], arrNet[i], ticker)

if orderId :

arrNet[i]["state"] = "cover"

arrNet[i]["id"] = orderId

else :

# Cancel

cancelOrder(arrNet[i]["coverPrice"], ORDER_TYPE_SELL)

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

def checkCoverOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "cover" :

arrNet[i]["id"] = -1

arrNet[i]["state"] = "idle"

Log(arrNet[i], "The node closes the position and resets to the idle state.", "#FF0000")

def onTick () :

global arrNet, arrMsg, acc

ticker = _C(exchange.GetTicker) # Get the latest current ticker every time

for i in range(len(arrNet)): # Iterate through all grid nodes, find out the position where you need to pend a buy order according to the current market, and pend a buy order.

if i != len(arrNet) - 1 and arrNet[i]["state"] == "idle" and ticker.Sell > arrNet[i]["price"] and ticker.Sell < arrNet[i + 1]["price"]:

acc = _C(exchange.GetAccount)

if acc.Balance < minBalance : # If there is not enough money left, you can only jump out and do nothing.

arrMsg.append("Insufficient funds" + json.dumps(acc) + "!" + ", time:" + _D())

break

orderId = exchange.Buy(arrNet[i]["price"], arrNet[i]["amount"], arrNet[i], ticker) # Pending buy orders

if orderId :

arrNet[i]["state"] = "pending" # Update the grid node status and other information if the buy order is successfully pending

arrNet[i]["id"] = orderId

else :

# Cancel h/the order

cancelOrder(arrNet[i]["price"], ORDER_TYPE_BUY) # Cancel orders by using the cancel function

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

Sleep(1000)

orders = _C(exchange.GetOrders)

checkOpenOrders(orders, ticker) # Check the status of all buy orders and process them according to the changes.

Sleep(1000)

orders = _C(exchange.GetOrders)

checkCoverOrders(orders, ticker) # Check the status of all sell orders and process them according to the changes.

# The following information about the construction status bar can be found in the FMZ API documentation.

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

while len(arrMsg) > 20 :

arrMsg.pop(0)

for i in range(len(arrMsg)) :

errTbl["rows"].append([i, json.dumps(arrMsg[i])])

for i in range(len(orders)) :

orderTbl["rows"].append([i, json.dumps(orders[i])])

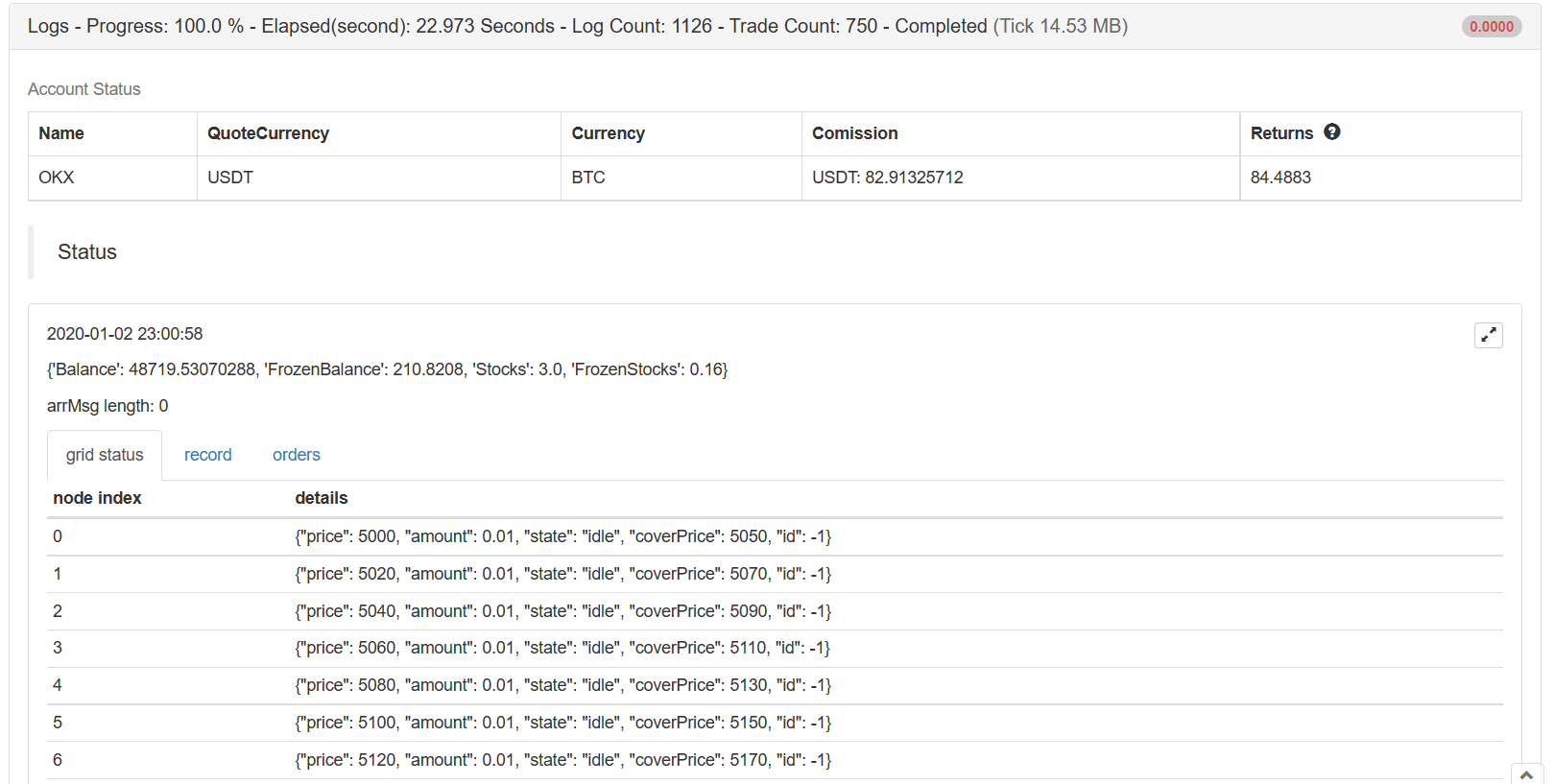

LogStatus(_D(), "\n", acc, "\n", "arrMsg length:", len(arrMsg), "\n", "`" + json.dumps([tbl, errTbl, orderTbl]) + "`")

def main (): # Strategy execution starts here

global arrNet

for i in range(int((endPrice - beginPrice) / distance)): # The for loop constructs a data structure for the grid based on the parameters, a list that stores each grid node, with the following information for each grid node:

arrNet.append({

"price" : beginPrice + i * distance, # Price of the node

"amount" : amount, # Number of orders

"state" : "idle", # pending / cover / idle # Node Status

"coverPrice" : beginPrice + i * distance + pointProfit, # Node closing price

"id" : -1, # ID of the current order related to the node

})

while True: # After the grid data structure is constructed, enter the main strategy loop

onTick() # Processing functions on the main loop, the main processing logic

Sleep(500) # Control polling frequency

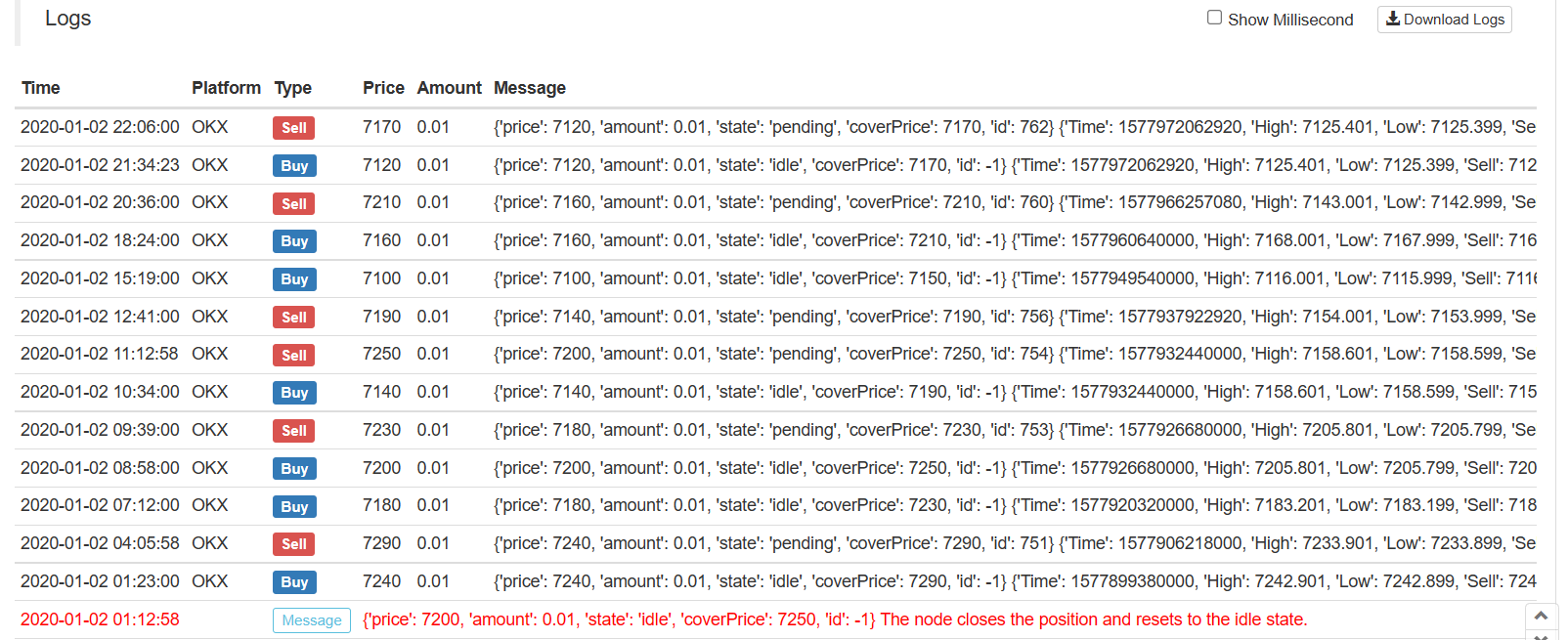

रणनीति का मुख्य डिजाइन विचार लंबित आदेशों की वर्तमान सूची की तुलना करना है।GetOrdersअपने द्वारा बनाए गए ग्रिड डेटा संरचना के अनुसार इंटरफ़ेस। लंबित आदेशों के परिवर्तनों का विश्लेषण करें (चाहे वे बंद हों या नहीं), ग्रिड डेटा संरचना को अपडेट करें, और बाद के संचालन करें। इसके अलावा, लेनदेन पूरा होने तक लंबित आदेश रद्द नहीं किए जाएंगे, भले ही कीमत विचलित हो, क्योंकि डिजिटल मुद्रा बाजार में अक्सर पिन की स्थिति होती है, ये लंबित आदेश पिन के आदेश भी प्राप्त कर सकते हैं (यदि एक्सचेंज में लंबित आदेशों की संख्या सीमित है, तो इसे समायोजित किया जाएगा) ।

रणनीति डेटा विज़ुअलाइज़ेशन का उपयोग करता हैLogStatusवास्तविक समय में स्थिति पट्टी पर डेटा प्रदर्शित करने के लिए कार्य।

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

तीन तालिकाएं बनाई जाती हैं। पहली तालिका वर्तमान ग्रिड डेटा संरचना में प्रत्येक नोड की जानकारी प्रदर्शित करती है, दूसरी तालिका असामान्य जानकारी प्रदर्शित करती है, और तीसरी तालिका एक्सचेंज की वास्तविक लिस्टिंग जानकारी प्रदर्शित करती है।

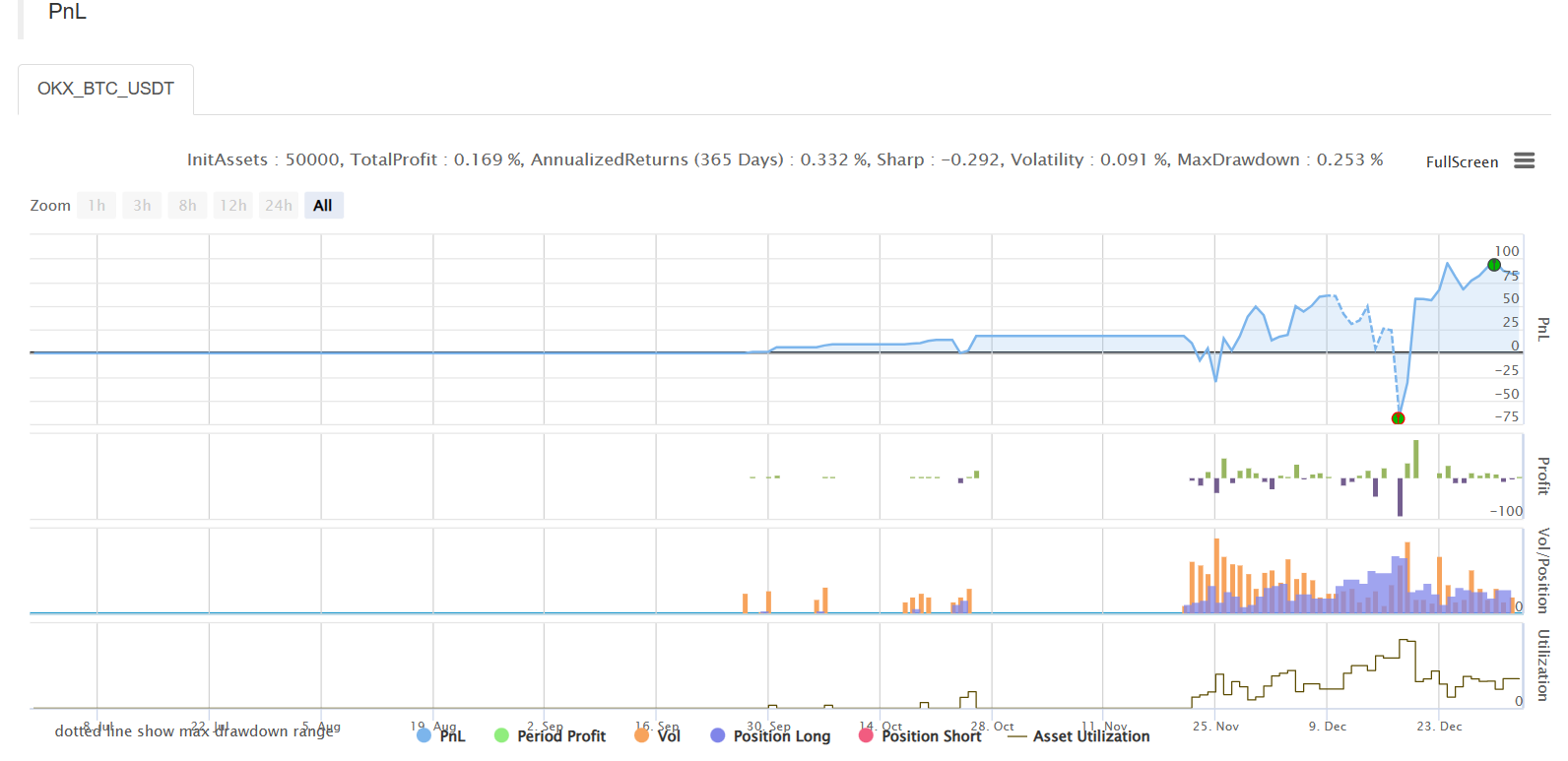

बैकटेस्ट

रणनीतिक पता

रणनीति केवल सीखने और बैकटेस्टिंग उद्देश्य के लिए है, और यह अनुकूलित किया जा सकता है और यदि आप रुचि रखते हैं उन्नयन.

- क्रिप्टोक्यूरेंसी बाजार में मौलिक विश्लेषण की मात्राः डेटा को खुद के लिए बोलने दें!

- मौद्रिक सर्कल के मूलभूत मात्रात्मक अनुसंधान - अब हर तरह के जादूगरों पर भरोसा न करें, डेटा निष्पक्ष रूप से बोलते हैं!

- क्वांटिफाइड ट्रेडिंग के लिए आवश्यक उपकरण - आविष्कारक क्वांटिफाइड डेटा एक्सप्लोरर मॉड्यूल

- सब कुछ में महारत हासिल करना - एफएमजेड ट्रेडिंग टर्मिनल का नया संस्करण (टीआरबी आर्बिट्रेज स्रोत कोड के साथ)

- सब कुछ जानने के लिए FMZ के नए संस्करण के लिए ट्रेडिंग टर्मिनल का परिचय (अनुदानित TRB सूट स्रोत कोड)

- एफएमजेड क्वांटः क्रिप्टोकरेंसी बाजार में सामान्य आवश्यकताओं के डिजाइन उदाहरणों का विश्लेषण (II)

- 80 पंक्तियों के कोड में उच्च आवृत्ति रणनीति के साथ मस्तिष्क रहित बिक्री बॉट्स का शोषण कैसे करें

- एफएमजेड क्वांटिकेशनः क्रिप्टोक्यूरेंसी बाजार में आम जरूरतों के डिजाइन उदाहरण का विश्लेषण

- 80 लाइनों के कोड के साथ उच्च आवृत्ति रणनीतियों का उपयोग करके बेचने के लिए मस्तिष्क रहित रोबोट का शोषण कैसे करें

- एफएमजेड क्वांटः क्रिप्टोकरेंसी बाजार में सामान्य आवश्यकताओं के डिजाइन उदाहरणों का विश्लेषण (I)

- एफएमजेड क्वांटिकेशनः क्रिप्टोक्यूरेंसी बाजार में आम जरूरतों के डिजाइन उदाहरण का विश्लेषण (1)