シンプル・ボラティリティ・EMV戦略

作者: リン・ハーン優しさ, 作成日:2020-07-01 10:39:17, 更新日:2023-10-28 15:26:49

概要

他の技術指標とは異なり,Ease of Movement Valueは価格,量,人気の変化を反映する技術である.これは価格と量の変化を組み合わせる技術である. 価格変動指標を形成する単位量の価格変化を測定する. 市場が人気を得て取引が活発になったとき,購入信号を提示する. 取引量が低く,市場エネルギーが尽きようとしているとき,販売信号を提示する.

シンプル・ボラティリティ・EMVは,同じボリューム・チャートと圧縮チャートの原理に従って設計されています.その核心コンセプトは:トレンドが回転する時または回転しようとしているときにのみ市場価格が多くのエネルギーを消費し,外部のパフォーマンスは取引量が大きくなるということです.価格が上昇しているとき,ブーシング効果のためにあまりにも多くのエネルギーを消費しません.この考えは量と価格の上昇の両方の見解に反しますが,独自の特徴があります.

EMV 計算式

ステップ1: mov_mid を計算する

その中,THは当日の最高価格,TLは当日の最低価格,YHは前日の最高価格,YLは前日の最低価格を表します.MID>0は,今日の平均価格が昨日の平均価格よりも高いことを意味します.

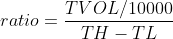

ステップ2:比率を計算する

TVOLは当日の取引量,THは当日の最高価格,TLは当日の最低価格を表しています.

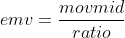

ステップ3:EMVを計算する

EMVの使用

EMVの著者は,巨大な上昇はエネルギーの急速な枯渇に伴い,上昇はしばしば長続きしないと考えており,反対に,一定量のエネルギーを節約できる適度なボリュームは,しばしば上昇を長続きさせる.上昇傾向が形成されると,取引量が少なくなり価格を押し上げ,EMVの価値が増加する.下落傾向市場が形成されると,それはしばしば無限または小さな減少に伴い,EMVの価値が低下する.価格が不安定な市場にある場合,または価格の上昇と減少が大きなボリュームに伴い,EMVの価値もゼロに近い.したがって,EMVはほとんどの市場でゼロ軸以下にあり,これはこの指標の主要な特徴でもあります.別の観点から,EMVのメガトレンドは十分な利益を生み出せる.

EMVの使用はかなりシンプルで,EMVがゼロ軸を横切るかを見るだけでよい.EMVが0を下回ると,それは弱い市場を表す.EMVが0を超えると,それは強い市場を表す.EMVがマイナスからポジティブに変化すると,それは購入されるべきである;EMVがポジティブからマイナスに変化すると,それは販売されるべきである.その特徴は,市場のショック市場を避けるだけでなく,トレンドマーケットが始まる時に市場に参入できるということです.しかし,EMVが価格の変化時のボリュムの変化を反映しているため,それは中期から長期間のトレンドにのみ影響を与えます.短期または比較的短い取引サイクルでは,EMV

戦略の実現

ステップ1: 戦略の枠組みを作成する

# Strategy main function

def onTick():

pass

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

FMZ.COMローテーション訓練モードを採用します. まず,main機能とonTick機能mainプログラムがコードを行ごとに実行します.main機能についてmain函数,a を書くwhileループを繰り返して実行しますonTick戦略のコアコードは全てonTick function.

ステップ2:位置データを取得

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

この戦略では 維持を容易にするため リアルタイムでの位置数だけを使いますget_positionポジションの数を表す.現在のポジションが長ければ正数,現在のポジションが短ければ負数返します.

ステップ3:K線データを取得

exchange.SetContractType('IH000') # Subscribe to futures variety

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

特定のK線データを取得する前に,まず特定の取引契約にサインし,SetContractType機能FMZ.COM契約に関する他の情報を知りたい場合は,このデータを受信するために変数も使用できます.GetRecords変数を使用します. 変数式は,bars_arr受け入れること

ステップ4:EMVを計算する

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

ここでは,最新の価格を使用してEMVの値を計算するのではなく,比較的遅れている現在のKラインを使用して信号を出力し,Kラインを配置して注文を出します.この目的は,バックテストを実際の取引に近いものにすることです.定量取引ソフトウェアが非常に進歩しているにもかかわらず,実際の価格ティック環境を完全にシミュレートすることはまだ困難です.特にバックテストの際には,バーレベルの長いデータを使用します.

ステップ 5: 注文を出す

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

オーダーを出す前に,我々は2つのデータを決定する必要があります. 1つはオーダーの価格であり,もう1つは現在のポジションの状態です. オーダーを出す価格は非常に簡単です.get_position最後に,位置は EMV とゼロ軸の位置関係に応じて開閉されます.

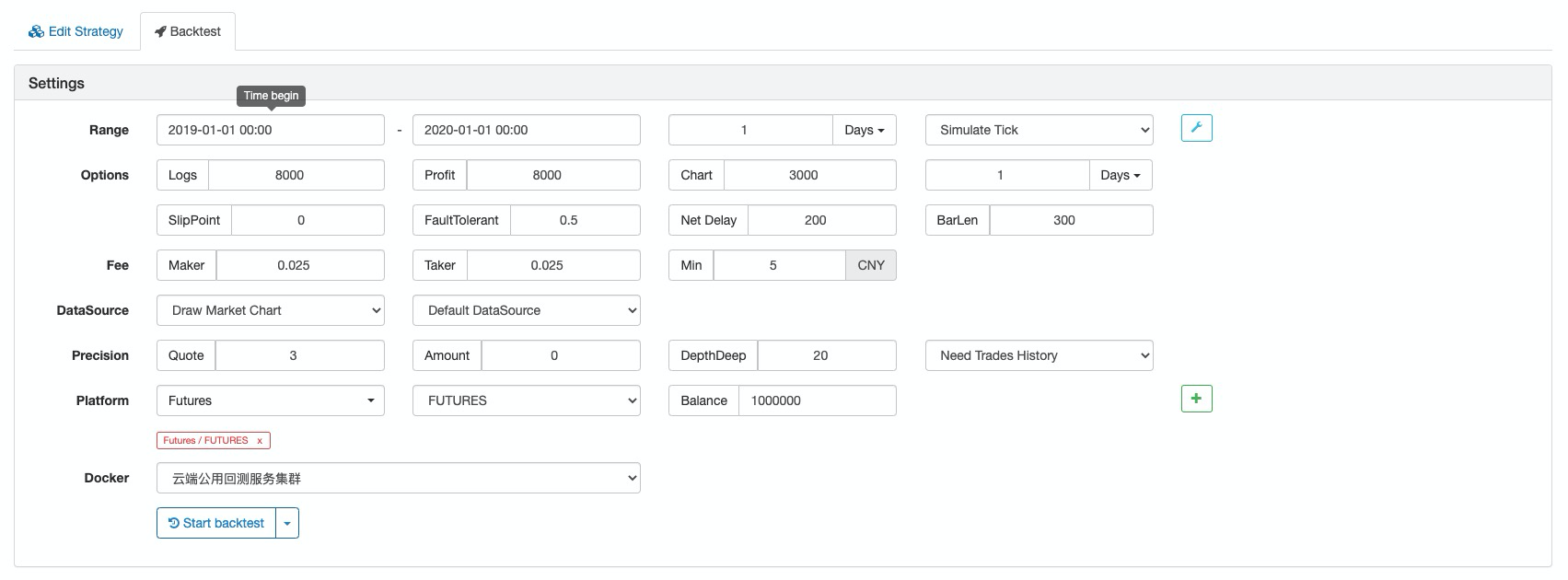

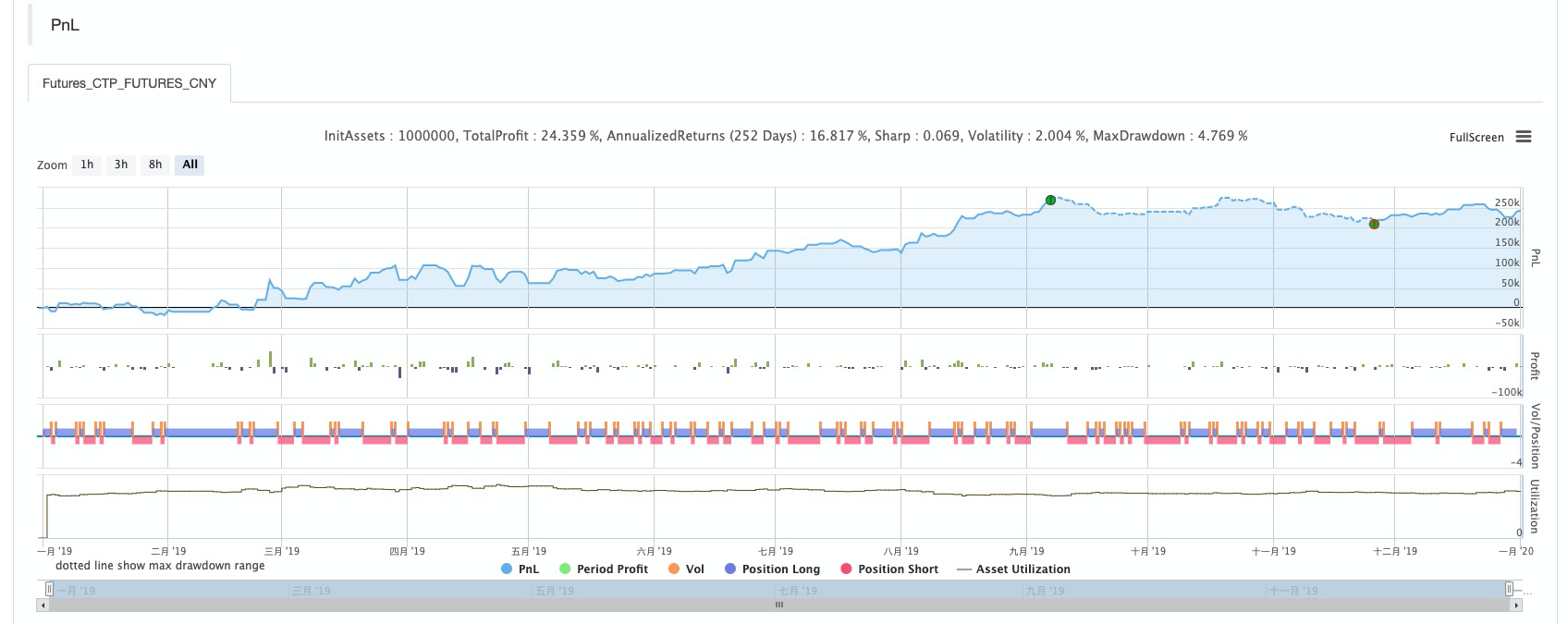

戦略のバックテスト

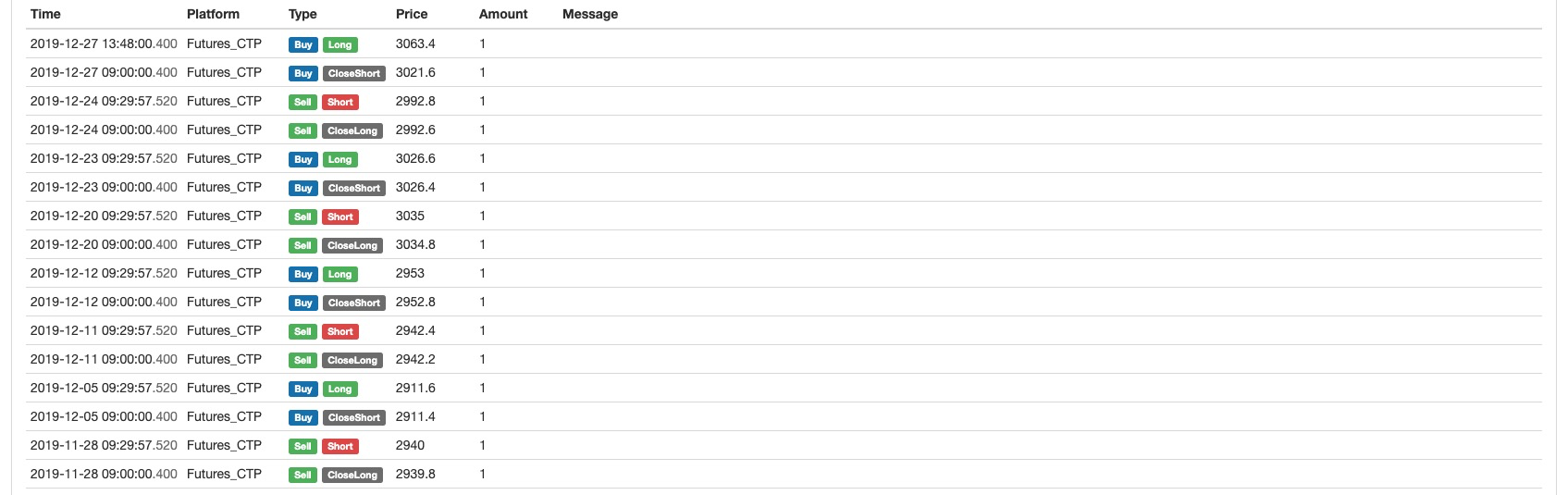

バックテスト設定

バックテスト ログ

資本曲線

完全な戦略

# Backtest configuration

'''backtest

start: 2019-01-01 00:00:00

end: 2020-01-01 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

'''

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

# Strategy main function

def onTick():

# retrieve data

exchange.SetContractType('IH000') # Subscribe to futures

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

# Calculate emv

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

# Placing orders

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

戦略の広場で公開されました.FMZ.COMコピーをクリックして利用できます.https://www.fmz.com/strategy/213636

結論から言うと

この研究を通して,EMVは普通のトレーダーと違っていることがわかりますが,それは不合理ではありません.EMVはボリュームデータを導入しているため,価格の背後にあるものを調べるために価格計算を使用する他の技術指標よりも効果的です.各戦略には異なる特徴があります.異なる戦略のメリットとデメリットを完全に理解し,ゴミを取り除き,その本質を抽出することでのみ,私たちは成功からさらに遠ざかることができます.

- 暗号通貨市場の基本分析を定量化する: データが自分で話せ!

- 通貨圏の基礎的な定量化研究 - 数字を客観的に話すために,あらゆる

教師を信頼しなくていい! - 量化取引の必須ツール - 発明者による量化データ探索モジュール

- すべてをマスターする - FMZの新バージョンの取引ターミナルへの紹介 (TRB仲裁ソースコード)

- FMZの新バージョンの取引端末のご紹介 (TRBの利息ソースコード追加)

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (II)

- 80行のコードで高周波戦略で 脳のない販売ボットを利用する方法

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (II)

- 80行コードの高周波戦略で脳のないロボットを搾取して売る方法

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (I)

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (1)