デジタル通貨に基づくダイナミックバランス戦略

作者: リン・ハーンリディア, 作成日:2022-12-01 16:17:29, 更新日:2023-09-20 09:43:30

I.要約

ウォーレン・バフェットのメンターである ベンジャミン・グラハムは 本"The Intelligent Investor"で 株式と債券のダイナミック・バランス・トレーディングモードについて言及しています

取引の仕方はとてもシンプルです - 資金の50%を株式基金に,残りの50%を債券基金に投資する.つまり,株と債券は,半分を互いに占めています. - 固定期間や市場変動に応じて,資産の再バランスを取って,株式資産と債券資産の比率を元の1:1に戻す. 購入・販売のタイミングや 購入・販売の金額など 簡単です!

II. ダイナミックバランス原則

この方法では,債券ファンドの変動は 実際には非常に小さく,株式の変動よりもはるかに低いので,債券はここで"参照アンカー"として使用されます.

株価が上昇すると,株価の市場価値は債券の市場価値より大きくなります.両者の市場価値比が設定された

戦略の論理

ブロックチェーン資産BTCにおける動的バランス戦略

戦略の論理

- 現在のBTC価値によると,口座残高は5000円と0.1BTCの現金で,つまり現金とBTCの市場価値の初期比率は1:1です.

- BTCの価格が6000円に上昇すると,つまりBTCの市場価値が口座残高よりも高く,その間の差が設定された

値を超えると, (6000-5000)/6000/2コインを売却します.それはBTCが値上がりしたことを意味し,お金を取り戻すことができます. - BTCの価格が4000円まで下がると,つまりBTCの市場価値が口座残高よりも低く,両者の差が設定された

値を超えると, (5000-4000)/4000/2コインを購入します.BTCが減価し,BTCを買い戻すことができます.

この方法で,BTCが値上げするか減価するかに関わらず,私たちは常に口座残高とBTCの市場価値を動的に等しく保っています.BTCが値下げした場合,私たちは購入し,再び上昇した場合,残高のように,いくつか販売します.

IV 戦略の枠組み

FMZ Quant Trading Platform を例として,まず戦略の枠組みを見てみましょう.

// function to cancel orders

function CancelPendingOrders() {}

// function to place an order

function onTick() {}

// main function

function main() {

// filter non-important information

SetErrorFilter("GetRecords:|GetOrders:|GetDepth:|GetAccount|:Buy|Sell|timeout");

while (true) { // polling mode

if (onTick()) { // execute onTick function

CancelPendingOrders(); // cancel the outstanding pending orders

Log(_C(exchange.GetAccount)); // print the current account information

}

Sleep(LoopInterval * 1000); // sleep

}

}

戦略の枠組み全体が非常にシンプルで,メイン機能,オンティックオーダー配置機能,キャンセル待ちオーダー機能,必要なパラメータを含む.

V. オーダープレスメント モジュール

// order-placing function

function onTick() {

var acc = _C(exchange.GetAccount); // obtain account information

var ticker = _C(exchange.GetTicker); // obtain Tick data

var spread = ticker.Sell - ticker.Buy; // obtain bid ask spread of Tick data

// 0.5 times of the difference between the account balance and the current position value

var diffAsset = (acc.Balance - (acc.Stocks * ticker.Sell)) / 2;

var ratio = diffAsset / acc.Balance; // diffAsset / account balance

LogStatus('ratio:', ratio, _D()); // Print ratio and current time

if (Math.abs(ratio) < threshold) { // If the absolute value of the ratio is less than the specified threshold

return false; // return false

}

if (ratio > 0) { // if ratio > 0

var buyPrice = _N(ticker.Sell + spread, ZPrecision); // Calculate the price of an order

var buyAmount = _N(diffAsset / buyPrice, XPrecision); // Calculate the order quantity

if (buyAmount < MinStock) { // If the order quantity is less than the minimum transaction quantity

return false; // return false

}

exchange.Buy(buyPrice, buyAmount, diffAsset, ratio); // Purchase order

} else {

var sellPrice = _N(ticker.Buy - spread, ZPrecision); // Calculate the price of an order

var sellAmount = _N(-diffAsset / sellPrice, XPrecision); // Calculate the order quantity

if (sellAmount < MinStock) { // If the order quantity is less than the minimum transaction quantity

return false; // return false

}

exchange.Sell(sellPrice, sellAmount, diffAsset, ratio); // Sell and place an order

}

return true; // return true

}

すべてのコメントがコードに書かれています. 拡大するには画像をクリックできます.

主なプロセスは次のとおりです

- 口座情報を入手する

- ティックのデータを取れ

- Tick のデータ の bid ask スプレッド を計算する.

- 口座残高とBTC市場価値の差を計算する.

- 購入・販売条件,注文価格,注文量などを計算する.

- 注文して返品する

VI. 撤収モジュール

// Withdrawal function

function CancelPendingOrders() {

Sleep(1000); // Sleep for 1 second

var ret = false;

while (true) {

var orders = null;

// Obtain the unsettled order array continuously. If an exception is returned, continue to obtain

while (!(orders = exchange.GetOrders())) {

Sleep(1000); // Sleep for 1 second

}

if (orders.length == 0) { // If the order array is empty

return ret; // Return to order withdrawal status

}

for (var j = 0; j < orders.length; j++) { // Iterate through the array of unfilled orders

exchange.CancelOrder(orders[j].Id); // Cancel unfilled orders in sequence

ret = true;

if (j < (orders.length - 1)) {

Sleep(1000); // Sleep for 1 second

}

}

}

}

撤収のモジュールは よりシンプルです.手順は以下の通りです.

- 注文をキャンセルする前は1秒待って

- 不定の順序配列を継続的に取得します.例外が返される場合は,取得を続けます.

- 処理されていないオーダーの配列が空いている場合,引き出しの状態は直ちに返されます.

- 順序が決まっていない場合は,配列全体を横切って順序番号に従って順序をキャンセルします.

VII 戦略の完全なソースコード

// Backtest environment

/*backtest

start: 2018-01-01 00:00:00

end: 2018-08-01 11:00:00

period: 1m

exchanges: [{"eid":"Bitfinex","currency":"BTC_USD"}]

*/

// Order withdrawal function

function CancelPendingOrders() {

Sleep(1000); // Sleep for 1 second

var ret = false;

while (true) {

var orders = null;

// Obtain the unsettled order array continuously. If an exception is returned, continue to obtain

while (!(orders = exchange.GetOrders())) {

Sleep(1000); // Sleep for 1 second

}

if (orders.length == 0) { // If the order array is empty

return ret; // Return to order withdrawal status

}

for (var j = 0; j < orders.length; j++) { // Iterate through the array of unfilled orders

exchange.CancelOrder(orders[j].Id); // Cancel unfilled orders in sequence

ret = true;

if (j < (orders.length - 1)) {

Sleep(1000); // Sleep for 1 second

}

}

}

}

// Order function

function onTick() {

var acc = _C(exchange.GetAccount); // obtain account information

var ticker = _C(exchange.GetTicker); // obtain Tick data

var spread = ticker.Sell - ticker.Buy; // obtain bid ask spread of Tick data

// 0.5 times of the difference between the account balance and the current position value

var diffAsset = (acc.Balance - (acc.Stocks * ticker.Sell)) / 2;

var ratio = diffAsset / acc.Balance; // diffAsset / account balance

LogStatus('ratio:', ratio, _D()); // Print ratio and current time

if (Math.abs(ratio) < threshold) { // If the absolute value of ratio is less than the specified threshold

return false; // return false

}

if (ratio > 0) { // if ratio > 0

var buyPrice = _N(ticker.Sell + spread, ZPrecision); // Calculate the order price

var buyAmount = _N(diffAsset / buyPrice, XPrecision); // Calculate the order quantity

if (buyAmount < MinStock) { // If the order quantity is less than the minimum trading quantity

return false; // return false

}

exchange.Buy(buyPrice, buyAmount, diffAsset, ratio); // buy order

} else {

var sellPrice = _N(ticker.Buy - spread, ZPrecision); // Calculate the order price

var sellAmount = _N(-diffAsset / sellPrice, XPrecision); // Calculate the order quantity

if (sellAmount < MinStock) { // If the order quantity is less than the minimum trading quantity

return false; // return false

}

exchange.Sell(sellPrice, sellAmount, diffAsset, ratio); // sell order

}

return true; // return true

}

// main function

function main() {

// Filter non-important information

SetErrorFilter("GetRecords:|GetOrders:|GetDepth:|GetAccount|:Buy|Sell|timeout");

while (true) { // Polling mode

if (onTick()) { // Execute onTick function

CancelPendingOrders(); // Cancel pending orders

Log(_C(exchange.GetAccount)); // Print current account information

}

Sleep(LoopInterval * 1000); // sleep

}

}

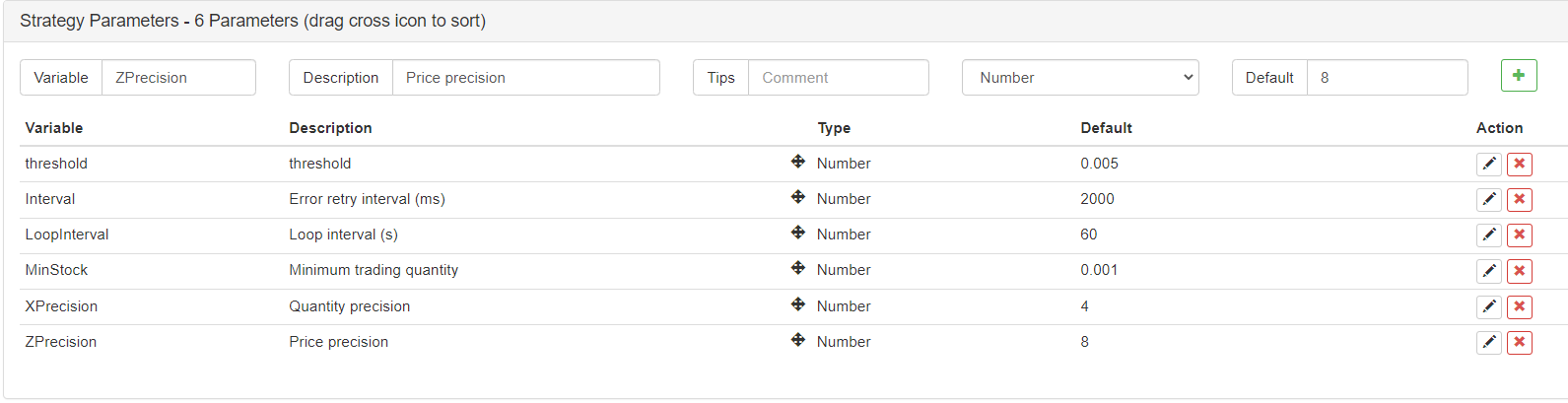

外部パラメータ

戦略のバックテスト

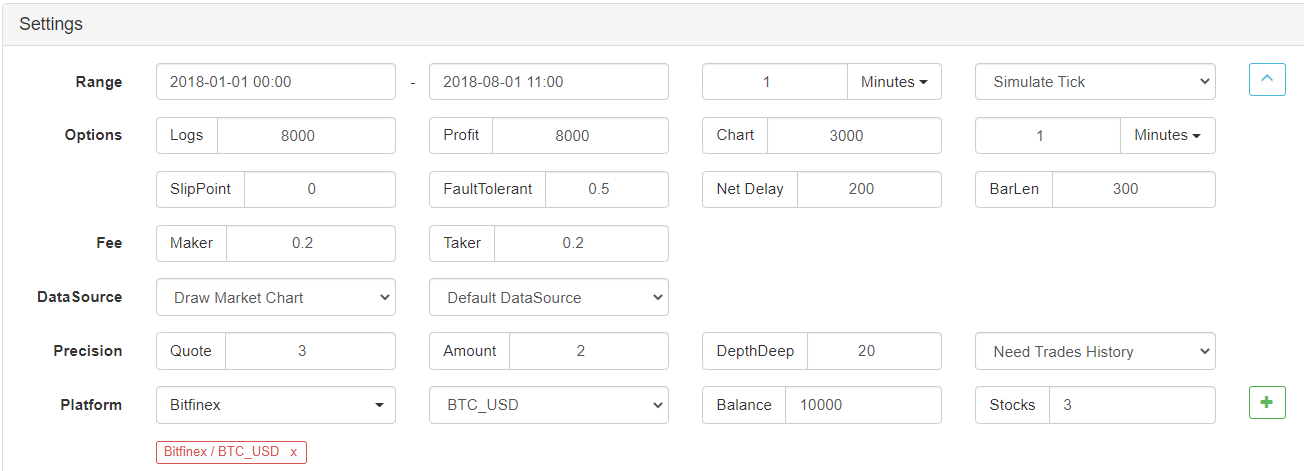

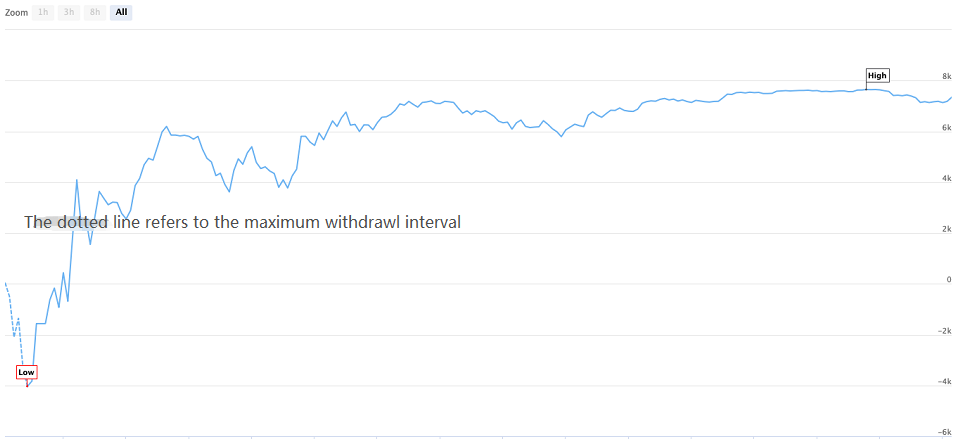

次に,この単純なダイナミックバランス戦略をテストして,それが有効かどうか見てみましょう. 以下は,参照のためだけのBTCの歴史的なデータに対するバックテストです.

バックテスト環境

バックテスト性能

バックテスト曲線

バックテスト期間中,BTCは最大70%以上の減少にもかかわらず,最大8ヶ月間も下落を続け,多くの投資家がブロックチェーン資産への信頼を失わせました.この戦略の累積収益率は160%まで,年間リターンリスク比率は5を超えています.このような単純な投資戦略では,投資収益率は,フルポジションにいるほとんどの人のものよりも高くなっています.

戦略のソースコードを取得

戦略のソースコードは FMZ Quantの公式ウェブサイトに公開されています.https://www.fmz.com/strategy/110545. 設定する必要はありません,あなたは直接オンラインバックテストすることができます.

X 概要

この記事のダイナミックバランス戦略には,非常に単純な投資方法である1つのコアパラメータ (しきい値) しかありません.それは過剰な収益ではなく,安定した収益を追求しています.トレンド戦略とは異なり,ダイナミックバランス戦略はトレンドに反しています.しかしダイナミックバランス戦略はちょうど逆です.市場は人気のあるとき,ポジションを減らす,市場は人気がないとき,ポジションをスケールする,これはマクロ経済規制に似ている.

実際,ダイナミックバランス戦略は,予測不可能な価格の概念を継承し,同時に価格変動を捉える工夫である.ダイナミックバランス戦略の核は,資産配分比率,トリガースロージックを設定し調整することです.長さを考えると,記事は包括的になることはできません.言葉を超えて,心があることを知っておくべきです.ダイナミックバランス戦略の最も重要な部分は投資アイデアです.この記事で個々のBTC資産をブロックチェーン資産ポートフォリオのバスケットに置き換えることもできます.

最後に,本文をベンジャミン・グラハムの著書"The Intelligent Investor"の有名な言葉で締めくくりましょう. 株式市場は,価値を正確に測定できる"計測機"ではなく",投票機"です. 無数の人が取る決断は,理性と感覚の混合物です. 多くの場合,これらの決定は理性的な価値判断から遠いものです. 投資の秘訣は,価格が本質的な価値よりもはるかに低いときに投資し,市場のトレンドが回復すると信じることです. ベンジャミン・グラハム 賢明な投資家

- 暗号通貨市場の基本分析を定量化する: データが自分で話せ!

- 通貨圏の基礎的な定量化研究 - 数字を客観的に話すために,あらゆる

教師を信頼しなくていい! - 量化取引の必須ツール - 発明者による量化データ探索モジュール

- すべてをマスターする - FMZの新バージョンの取引ターミナルへの紹介 (TRB仲裁ソースコード)

- FMZの新バージョンの取引端末のご紹介 (TRBの利息ソースコード追加)

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (II)

- 80行のコードで高周波戦略で 脳のない販売ボットを利用する方法

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (II)

- 80行コードの高周波戦略で脳のないロボットを搾取して売る方法

- FMZ Quant: 仮想通貨市場における共通要件設計例の分析 (I)

- FMZ定量化:仮想通貨市場の常用需要設計事例解析 (1)