단순 변동성 EMV 전략

저자:선함, 2020-07-01 10:39:17, 업데이트: 2023-10-28 15:26:49

요약

다른 기술 지표와 달리,

간단한 변동성 EMV는 동일한 볼륨 차트와 압축 차트의 원칙에 따라 설계되었습니다. 그것의 핵심 개념은: 시장 가격은 트렌드가 전환되거나 전환 될 때만 많은 에너지를 소비하고 외부 성능은 거래량이 커지는 것입니다. 가격이 상승할 때, 부팅 효과로 인해 너무 많은 에너지를 소비하지 않습니다. 이 아이디어가 양과 가격 상승 두 가지 견해에 반대하지만, 그것은 고유한 특징을 가지고 있습니다.

EMV 계산 공식

단계 1: mov_mid를 계산합니다

그 중 TH는 하루의 가장 높은 가격을 나타내고 TL는 하루의 가장 낮은 가격을 나타내고 YH는 전날의 가장 높은 가격을 나타내고 YL는 전날의 가장 낮은 가격을 나타냅니다. MID> 0는 오늘의 평균 가격이 어제의 평균 가격보다 높다는 것을 의미합니다.

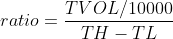

단계 2: 비율을 계산합니다.

그 중 TVOL는 하루 거래량을, TH는 하루 최고 가격을, TL는 하루 최저 가격을 나타냅니다.

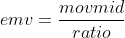

단계 3: emv를 계산합니다.

EMV 사용

EMV의 저자는 거대한 상승이 에너지의 급속한 고갈에 동반되며 상승은 종종 너무 오래 지속되지 않는다고 믿습니다. 반대로, 일정 양의 에너지를 절약 할 수있는 온건한 부피는 상승을 더 오래 지속시킵니다. 상승 추세가 형성되면 거래 부피가 줄어들면 가격이 상승 할 수 있으며 EMV의 가치가 증가 할 것입니다. 하락 추세가 형성되면 시장은 종종 무한하거나 작은 감소로 동반되며 EMV의 가치가 감소 할 것입니다. 가격이 변동적인 시장에 있거나 가격 상승과 하락이 큰 부피로 동반되면 EMV의 가치도 0에 가깝게 될 것입니다. 따라서 EMV가 시장의 대부분에서 0축 아래에 있음을 알게 될 것입니다. 이것은 또한이 지표의 주요 특징입니다. 다른 관점에서 EMV 메가 트렌드는 충분한 수익을 창출 할 수 있습니다.

EMV의 사용은 매우 간단합니다. EMV가 제로 축을 통과하는지 살펴보십시오. EMV가 0보다 낮을 때 약한 시장을 나타냅니다. EMV가 0보다 높을 때 강한 시장을 나타냅니다. EMV가 음에서 양으로 변하면 구입해야합니다; EMV가 양에서 음으로 변하면 판매해야합니다. 그것의 특징은 시장의 충격 시장을 피할 수있을뿐만 아니라 트렌드 시장이 시작되는 시간에 시장에 진입 할 수 있다는 것입니다. 그러나 EMV가 가격이 변할 때 볼륨의 변화를 반영하기 때문에 중장기 트렌드에만 영향을 미칩니다. 단기 또는 비교적 짧은 거래 주기에 EMV의 효과는 매우 약합니다.

전략 실현

단계 1: 전략 프레임워크를 작성

# Strategy main function

def onTick():

pass

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

FMZ.COM회전 훈련 모드를 채택합니다. 먼저, 당신은main기능 및onTick기능.main함수는 전략의 입력 함수입니다. 그리고 프로그램은 코드 라인을main기능.main함수, a를 적어while루프를 반복해서 실행onTick전략의 모든 핵심 코드는onTick function.

단계 2: 위치 데이터를 얻으십시오

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

왜냐하면 이 전략에서는 유지보수를 촉진하기 위해 실시간 위치만 사용되기 때문입니다.get_position포지션의 양을 포괄하기 위해 사용됩니다. 현재 포지션이 길다면 긍정적 인 숫자를 반환하고, 현재 포지션이 짧으면 부정적인 숫자를 반환합니다.

단계 3: K-라인 데이터를 얻으십시오

exchange.SetContractType('IH000') # Subscribe to futures variety

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

특정 K-라인 데이터를 얻기 전에 먼저 특정 거래 계약을 가입하고SetContractType함수에서FMZ.COM, 그리고 계약 코드를 입력합니다. 계약에 대한 다른 정보를 알고 싶다면, 당신은 또한 이 데이터를 수신하기 위해 변수를 사용할 수 있습니다.GetRecordsK선 데이터를 얻기 위한 함수입니다. 반환된 값은 배열이기 때문에 변수를 사용합니다.bars_arr받아들이기 위해서요.

단계 4: emv를 계산합니다

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

여기서, 우리는 EMV의 값을 계산하기 위해 최신 가격을 사용하지 않고, 신호를 출력하고 명령을 내리기 위해 K 라인을 배치하기 위해 상대적으로 지연된 현재 K 라인을 사용합니다. 이의 목적은 실제 거래에 더 가까운 백테스트를 만드는 것입니다. 양적 거래 소프트웨어가 이제 매우 진보되었지만, 특히 바 레벨 긴 데이터의 백테스팅에 직면했을 때 실제 가격 틱 환경을 완전히 시뮬레이션하는 것이 여전히 어렵다는 것을 알고 있습니다. 따라서이 타협 방법이 사용됩니다.

단계 5: 주문을 하는 것

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

주문을 하기 전에, 우리는 두 가지 데이터를 결정 해야 합니다, 하나는 주문의 가격이고 다른 하나는 현재 위치 상태입니다. 주문을 하는 가격은 매우 간단합니다, 그냥 현재 폐쇄 가격을 사용하여 다양성의 최소 변화 가격을 더하거나 빼기.get_position위치를 캡슐화하는 함수, 우리는 여기에 직접 호출 할 수 있습니다. 마지막으로, EMV와 0 축 사이의 위치 관계에 따라 위치가 열리고 닫습니다.

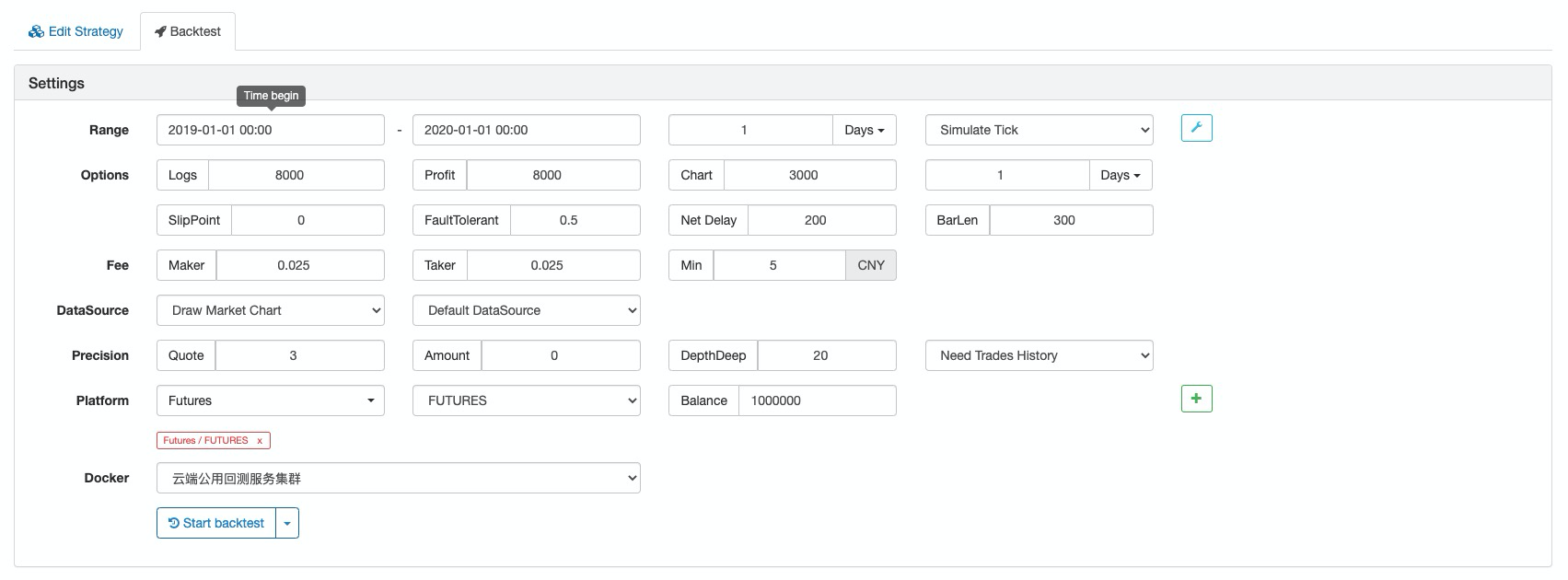

전략 백테스트

백테스트 구성

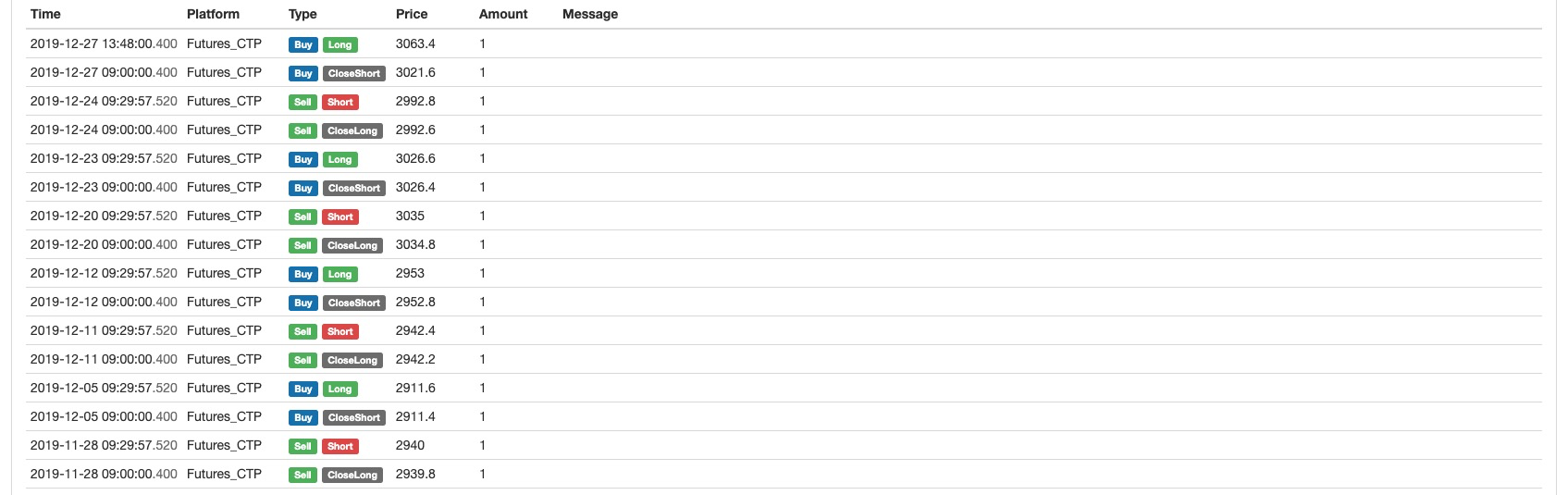

백테스트 로그

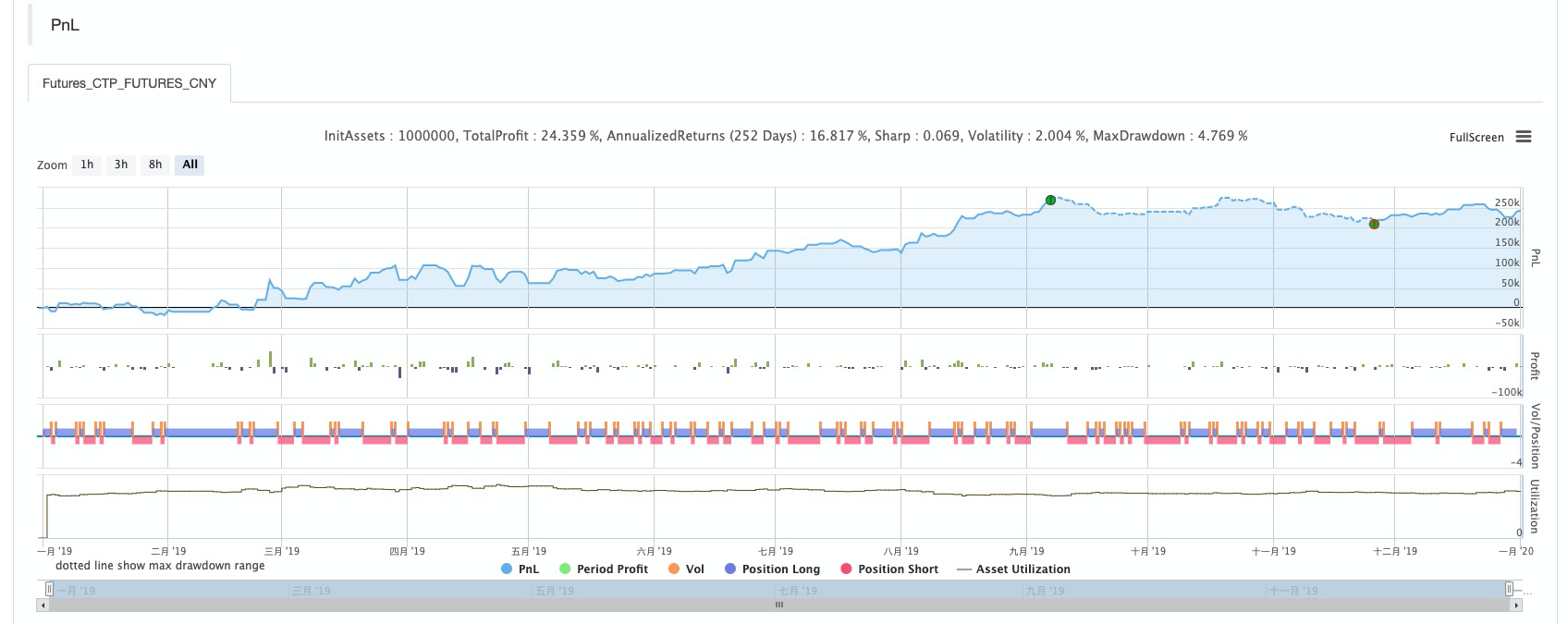

자본 곡선

전체 전략

# Backtest configuration

'''backtest

start: 2019-01-01 00:00:00

end: 2020-01-01 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

'''

def get_position():

position = 0 # The number of assigned positions is 0

position_arr = _C(exchange.GetPosition) # Get array of positions

if len(position_arr)> 0: # If the position array length is greater than 0

for i in position_arr: # Traverse the array of positions

if i['ContractType'] =='IH000': # If the position symbol is equal to the subscription symbol

if i['Type']% 2 == 0: # if it is long position

position = i['Amount'] # Assign a positive number of positions

else:

position = -i['Amount'] # Assign the number of positions to be negative

return position # return position quantity

# Strategy main function

def onTick():

# retrieve data

exchange.SetContractType('IH000') # Subscribe to futures

bars_arr = exchange.GetRecords() # Get K-line array

if len(bars_arr) <10: # If the number of K lines is less than 10

return

# Calculate emv

bar1 = bars_arr[-2] # Get the previous K-line data

bar2 = bars_arr[-3] # get the previous K-line data

# Calculate the value of mov_mid

mov_mid = (bar1['High'] + bar1['Low']) / 2-(bar2['High'] + bar2['Low']) / 2

if bar1['High'] != bar1['Low']: # If the dividend is not 0

# Calculate the value of ratio

ratio = (bar1['Volume'] / 10000) / (bar1['High']-bar1['Low'])

else:

ratio = 0

# If the value of ratio is greater than 0

if ratio> 0:

emv = mov_mid / ratio

else:

emv = 0

# Placing orders

current_price = bars_arr[-1]['Close'] # latest price

position = get_position() # Get the latest position

if position> 0: # If you are holding long positions

if emv <0: # If the current price is less than teeth

exchange.SetDirection("closebuy") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # close long position

if position <0: # If you are holding short positions

if emv> 0: # If the current price is greater than the teeth

exchange.SetDirection("closesell") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # close short position

if position == 0: # If there is no holding position

if emv> 0: # If the current price is greater than the upper lip

exchange.SetDirection("buy") # Set the trading direction and type

exchange.Buy(round(current_price + 0.2, 2), 1) # open long position

if emv <0: # if the current price is smaller than the chin

exchange.SetDirection("sell") # Set the trading direction and type

exchange.Sell(round(current_price-0.2, 2), 1) # open short position

# Program entry

def main():

while True: # Enter infinite loop mode

onTick() # execution strategy main function

Sleep(1000) # sleep for 1 second

전체 전략은FMZ.COM이 웹사이트는 복사 버튼을 눌러서 사용할 수 있습니다.https://www.fmz.com/strategy/213636

요약하면

이 연구 과정을 통해 우리는 EMV가 일반 상인들과는 반대되는 것을 볼 수 있지만, 그것은 불합리하지 않습니다. EMV가 볼륨 데이터를 도입하기 때문에 가격 계산을 사용하여 가격 뒤에있는 것을 알아내는 다른 기술 지표보다 더 효과적입니다. 각 전략은 다른 특성을 가지고 있습니다. 다른 전략의 장단점을 완전히 이해하고 쓰레기를 제거하고 본질을 추출하는 것만이 성공을 통해 더 나아갈 수 있습니다.

- 암호화폐 시장의 근본 분석을 정량화: 데이터를 스스로 이야기하도록!

- 동전圈의 기초적인 양적 연구 - 더 이상 모든

선생님들을 믿지 말고, 데이터를 객관적으로 이야기하십시오! - 양적 거래의 필수 도구 - 발명자 양적 데이터 탐색 모듈

- 모든 것을 마스터 - FMZ에 대한 소개 트레이딩 터미널의 새로운 버전 (TRB 중재 소스 코드)

- FMZ의 새로운 거래 단말기 소개 (TRB 리비트 소스 추가)

- FMZ 퀀트: 암호화폐 시장에서 공통 요구 사항 설계 예제 분석 (II)

- 80 줄의 코드에서 고주파 전략으로 뇌 없는 판매봇을 이용하는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (II)

- 80줄의 코드의 고주파 전략으로 뇌 없는 로봇을 파는 방법

- FMZ Quant: 암호화폐 시장에서 공통 요구 사항 디자인 예의 분석 (I)

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (1)