디지털 화폐에 기반한 동적 균형 전략

저자:리디아, 창작: 2022-12-01 16:17:29, 업데이트: 2023-09-20 09:43:30

요약

워렌 버핏의 멘토인 벤자민 그레이엄은 책에서 동적 균형 거래 방식을 언급했습니다.

거래 방식은 매우 간단합니다. 자금의 50%를 주식 펀드에 투자하고 나머지 50%를 채권 펀드에 투자합니다. 즉 주식과 채권은 서로 절반을 차지합니다. - 고정된 간격 또는 시장 변화에 따라 자산 재균형을 수행하여 주식 자산과 채권 자산의 비율을 원래 1:1로 회복합니다. 이 전략의 논리, 언제 구매하고 판매하고 얼마나 구매하고 판매하는지를 포함합니다.

동적 균형 원칙

이 방법에서는 채권 펀드의 변동성은 실제로 주식 변동성보다 훨씬 낮습니다. 그래서 채권은 여기서 " 참조 앵커 "로 사용됩니다. 즉 채권에 의해 주가가 너무 많이 상승했는지 너무 적게 상승했는지 측정하기 위해서입니다. 주식 가격이 상승하면 주식의 시장 가치는 채권의 시장 가치보다 커질 것입니다. 두 가지의 시장 가치 비율이 설정된 임계치를 초과하면 전체 지위가 재조정되며 주식이 판매되고 채권이 구매되므로 주식과 채권의 시장 가치 비율이 원래 1:1로 돌아갈 것입니다. 반대로 주식 가격이 하락하면 주식의 시장 가치는 채권의 시장 가치보다 작을 것입니다. 두 가지의 시장 가치 비율이 설정된 임계치를 초과하면 전체 지위가 재조정되며 주식이 구입되고 채권이 판매되므로 주식과 채권의 시장 가치 비율이 원래 1:1로 돌아갈 것입니다. 이 방법으로 우리는 주식 성장의 열매를 즐길 수 있고 동적으로 주식과 채권 사이의 비율을 균형을 맞추어 자산 변동성을 줄일 수 있습니다. 가치 투자의 선구자로서 그레이엄은 우리에게 좋은 아이디어를 제공했습니다. 이것은 완전한 전략이기 때문에 왜 디지털 통화에서 사용하지 않습니까?

III. 전략 논리

블록체인 자산 BTC의 동적 균형 전략

전략 논리

- 현재 BTC 가치에 따르면 계좌 잔액은 ¥5000과 0.1 BTC의 현금을 보유합니다. 즉, 현금과 BTC 시장 가치의 초기 비율은 1:1입니다.

- BTC의 가격이 6000 엔으로 증가하면 즉 BTC의 시장 가치가 계좌 잔액보다 커지고 그 사이의 차이는 설정된 임계치를 초과하면 (6000-5000) / 6000/2 동전을 판매합니다. BTC가 상승했다는 것을 의미합니다. 그리고 우리는 돈을 다시 교환 할 수 있습니다.

- BTC의 가격이 4000엔으로 떨어지면, 즉 BTC의 시장 가치가 계좌 잔액보다 작고 그 사이의 차이는 설정된 임계치를 초과하면 (5000-4000)/4000/2 동전을 구입합니다. BTC가 절감되었음을 의미하며 BTC를 다시 구입할 수 있습니다.

이 방법으로, BTC가 상승하거나 하락하든 상관없이, 우리는 항상 계좌 잔액과 BTC의 시장 가치를 동적으로 동일하게 유지합니다. BTC가 하락하면, 우리는 구매하고, 다시 상승하면, 우리는 잔액처럼 판매합니다.

IV. 전략 틀

그래서, 어떻게 코드를 구현합니까? 우리는 예를 들어 FMZ 양자 거래 플랫폼을 가지고, 먼저 전략 프레임워크를 살펴보자:

// function to cancel orders

function CancelPendingOrders() {}

// function to place an order

function onTick() {}

// main function

function main() {

// filter non-important information

SetErrorFilter("GetRecords:|GetOrders:|GetDepth:|GetAccount|:Buy|Sell|timeout");

while (true) { // polling mode

if (onTick()) { // execute onTick function

CancelPendingOrders(); // cancel the outstanding pending orders

Log(_C(exchange.GetAccount)); // print the current account information

}

Sleep(LoopInterval * 1000); // sleep

}

}

전체 전략 프레임워크는 실제로 매우 간단합니다. 주요 기능, ONTICK 주문 배치 기능, CANCELPENDINGORDERS 기능, 필요한 매개 변수를 포함합니다.

V. 주문 배치 모듈

// order-placing function

function onTick() {

var acc = _C(exchange.GetAccount); // obtain account information

var ticker = _C(exchange.GetTicker); // obtain Tick data

var spread = ticker.Sell - ticker.Buy; // obtain bid ask spread of Tick data

// 0.5 times of the difference between the account balance and the current position value

var diffAsset = (acc.Balance - (acc.Stocks * ticker.Sell)) / 2;

var ratio = diffAsset / acc.Balance; // diffAsset / account balance

LogStatus('ratio:', ratio, _D()); // Print ratio and current time

if (Math.abs(ratio) < threshold) { // If the absolute value of the ratio is less than the specified threshold

return false; // return false

}

if (ratio > 0) { // if ratio > 0

var buyPrice = _N(ticker.Sell + spread, ZPrecision); // Calculate the price of an order

var buyAmount = _N(diffAsset / buyPrice, XPrecision); // Calculate the order quantity

if (buyAmount < MinStock) { // If the order quantity is less than the minimum transaction quantity

return false; // return false

}

exchange.Buy(buyPrice, buyAmount, diffAsset, ratio); // Purchase order

} else {

var sellPrice = _N(ticker.Buy - spread, ZPrecision); // Calculate the price of an order

var sellAmount = _N(-diffAsset / sellPrice, XPrecision); // Calculate the order quantity

if (sellAmount < MinStock) { // If the order quantity is less than the minimum transaction quantity

return false; // return false

}

exchange.Sell(sellPrice, sellAmount, diffAsset, ratio); // Sell and place an order

}

return true; // return true

}

주문 거래 논리는 잘 조직되어 있으며 모든 댓글이 코드에 기록되었습니다. 확대하기 위해 이미지를 클릭할 수 있습니다.

주요 과정은 다음과 같습니다.

- 계좌 정보를 얻어요

- 틱 데이터를 가져와

- Tick 데이터의 bid/ask 스프레드를 계산합니다.

- 계좌 잔액과 BTC 시장 가치의 차이를 계산합니다.

- 구매 및 판매 조건, 주문 가격 및 주문 수를 계산합니다.

- 주문을 하고 다시 돌려주세요.

VI. 철수 모듈

// Withdrawal function

function CancelPendingOrders() {

Sleep(1000); // Sleep for 1 second

var ret = false;

while (true) {

var orders = null;

// Obtain the unsettled order array continuously. If an exception is returned, continue to obtain

while (!(orders = exchange.GetOrders())) {

Sleep(1000); // Sleep for 1 second

}

if (orders.length == 0) { // If the order array is empty

return ret; // Return to order withdrawal status

}

for (var j = 0; j < orders.length; j++) { // Iterate through the array of unfilled orders

exchange.CancelOrder(orders[j].Id); // Cancel unfilled orders in sequence

ret = true;

if (j < (orders.length - 1)) {

Sleep(1000); // Sleep for 1 second

}

}

}

}

인출 모듈은 더 간단합니다. 단계는 다음과 같습니다.

- 주문을 취소하기 전에 1초만 기다려요

- 연속적으로 unsettled 순서 배열을 얻습니다. 예외가 반환되면 계속 얻습니다.

- 해결되지 않은 명령어 배열이 비어있는 경우, 철수 상태는 즉시 반환됩니다.

- 정해지지 않은 순서가 있다면, 전체 배열을 가로질러 순서 번호에 따라 순서가 취소됩니다.

VII. 전체 전략 소스 코드

// Backtest environment

/*backtest

start: 2018-01-01 00:00:00

end: 2018-08-01 11:00:00

period: 1m

exchanges: [{"eid":"Bitfinex","currency":"BTC_USD"}]

*/

// Order withdrawal function

function CancelPendingOrders() {

Sleep(1000); // Sleep for 1 second

var ret = false;

while (true) {

var orders = null;

// Obtain the unsettled order array continuously. If an exception is returned, continue to obtain

while (!(orders = exchange.GetOrders())) {

Sleep(1000); // Sleep for 1 second

}

if (orders.length == 0) { // If the order array is empty

return ret; // Return to order withdrawal status

}

for (var j = 0; j < orders.length; j++) { // Iterate through the array of unfilled orders

exchange.CancelOrder(orders[j].Id); // Cancel unfilled orders in sequence

ret = true;

if (j < (orders.length - 1)) {

Sleep(1000); // Sleep for 1 second

}

}

}

}

// Order function

function onTick() {

var acc = _C(exchange.GetAccount); // obtain account information

var ticker = _C(exchange.GetTicker); // obtain Tick data

var spread = ticker.Sell - ticker.Buy; // obtain bid ask spread of Tick data

// 0.5 times of the difference between the account balance and the current position value

var diffAsset = (acc.Balance - (acc.Stocks * ticker.Sell)) / 2;

var ratio = diffAsset / acc.Balance; // diffAsset / account balance

LogStatus('ratio:', ratio, _D()); // Print ratio and current time

if (Math.abs(ratio) < threshold) { // If the absolute value of ratio is less than the specified threshold

return false; // return false

}

if (ratio > 0) { // if ratio > 0

var buyPrice = _N(ticker.Sell + spread, ZPrecision); // Calculate the order price

var buyAmount = _N(diffAsset / buyPrice, XPrecision); // Calculate the order quantity

if (buyAmount < MinStock) { // If the order quantity is less than the minimum trading quantity

return false; // return false

}

exchange.Buy(buyPrice, buyAmount, diffAsset, ratio); // buy order

} else {

var sellPrice = _N(ticker.Buy - spread, ZPrecision); // Calculate the order price

var sellAmount = _N(-diffAsset / sellPrice, XPrecision); // Calculate the order quantity

if (sellAmount < MinStock) { // If the order quantity is less than the minimum trading quantity

return false; // return false

}

exchange.Sell(sellPrice, sellAmount, diffAsset, ratio); // sell order

}

return true; // return true

}

// main function

function main() {

// Filter non-important information

SetErrorFilter("GetRecords:|GetOrders:|GetDepth:|GetAccount|:Buy|Sell|timeout");

while (true) { // Polling mode

if (onTick()) { // Execute onTick function

CancelPendingOrders(); // Cancel pending orders

Log(_C(exchange.GetAccount)); // Print current account information

}

Sleep(LoopInterval * 1000); // sleep

}

}

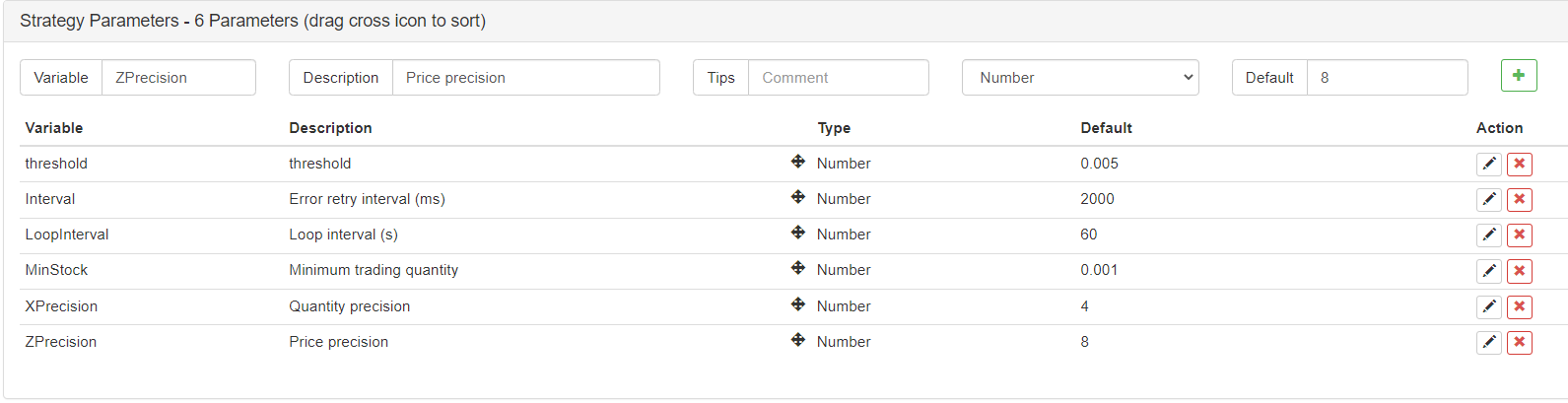

외부 매개 변수

VIII. 전략 역 테스트

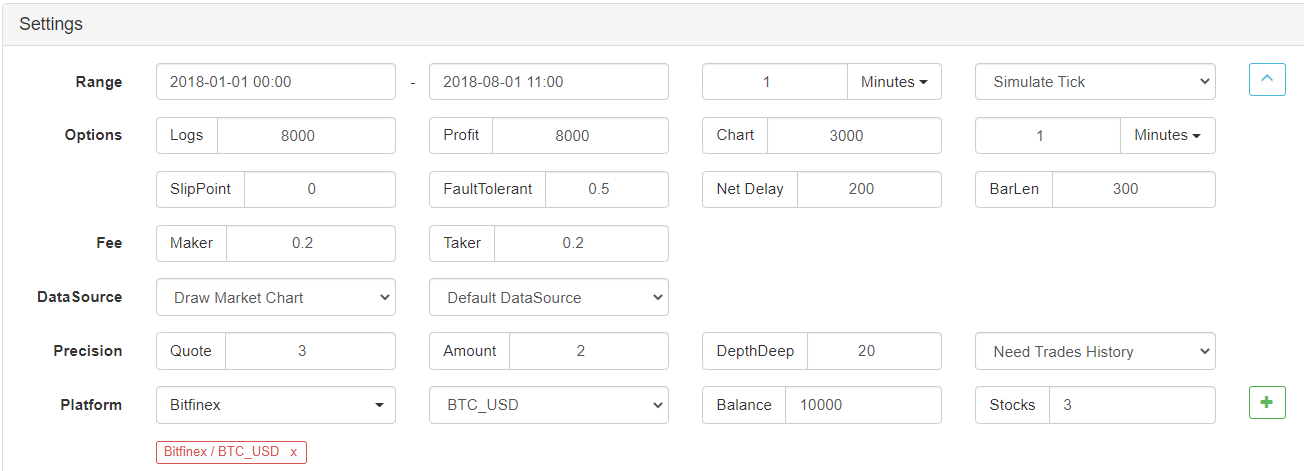

다음으로, 이 간단한 동적 균형 전략이 작동하는지 확인하기 위해 테스트 해 봅시다. 다음은 참조를 위해 BTC의 역사적 데이터에 대한 백테스트입니다.

백테스팅 환경

백테스팅 성능

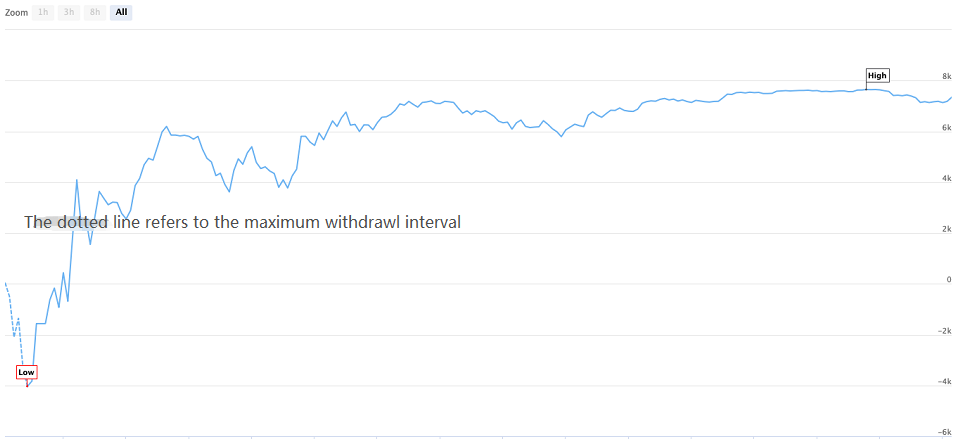

백테스팅 곡선

백테스트 기간 동안 BTC는 최대 70% 이상의 최대 감소에도 불구하고 최대 8 개월 동안 계속 하락했으며 많은 투자자들이 블록체인 자산에 대한 신뢰를 잃게되었습니다. 이 전략의 누적 수익률은 최대 160%이며 연간 수익 위험 비율은 5을 초과합니다. 그러한 간단한 투자 전략의 경우 투자 수익률은 완전한 위치에있는 대부분의 사람들의 수익률을 초과했습니다.

IX. 전략 소스 코드를 얻으십시오

전략의 소스 코드는 FMZ Quant 공식 웹사이트에 공개되었습니다.https://www.fmz.com/strategy/110545설정할 필요가 없습니다, 당신은 온라인으로 직접 백테스팅 할 수 있습니다.

X. 요약

이 문서의 동적 균형 전략은 매우 간단한 투자 방법인 하나의 핵심 매개 변수 (약수) 만 가지고 있습니다. 그것은 과도한 수익을 추구하는 것이 아니라 안정적인 수익을 추구합니다. 트렌드 전략과 달리 동적 균형 전략은 트렌드에 반대합니다. 그러나 동적 균형 전략은 바로 그 반대입니다. 시장이 인기가있을 때 위치를 줄이고 시장이 인기가 없을 때 위치를 확장하는 것이 거시 경제 규제와 유사합니다.

사실, 동적 균형 전략은 예측 불가능한 가격의 개념을 계승하고 동시에 가격 변동을 포착하는 기술이다. 동적 균형 전략의 핵심은 자산 할당 비율을 설정하고 조정하는 것뿐만 아니라 트리거 문턱이다. 길이를 고려하면 기사는 포괄적일 수 없다. 단어 너머에는 마음이 있다는 것을 알아야 한다. 동적 균형 전략의 가장 중요한 부분은 투자 아이디어이다. 이 기사에서 개별 BTC 자산을 블록체인 자산 포트폴리오의 바구니로 대체할 수도 있다.

마지막으로 벤자민 그레이엄의 저서?? 지능형 투자자?? 에서 유명한 단어로 이 기사를 마무리하자: 주식 시장은 가치를 정확하게 측정할 수 있는 "중량 기계"가 아니라 "투표 기계"입니다. 수많은 사람들이 결정하는 것은 합리성과 감수성의 혼합물입니다. 종종 이러한 결정은 합리적인 가치 판단과는 거리가 멀습니다. 투자의 비결은 가격이 본질적 가치보다 훨씬 낮을 때 투자하고 시장 추세가 회복 될 것이라고 믿는 것입니다. 벤자민 그레이엄 똑똑한 투자자

- 암호화폐 시장의 근본 분석을 정량화: 데이터를 스스로 이야기하도록!

- 동전圈의 기초적인 양적 연구 - 더 이상 모든

선생님들을 믿지 말고, 데이터를 객관적으로 이야기하십시오! - 양적 거래의 필수 도구 - 발명자 양적 데이터 탐색 모듈

- 모든 것을 마스터 - FMZ에 대한 소개 트레이딩 터미널의 새로운 버전 (TRB 중재 소스 코드)

- FMZ의 새로운 거래 단말기 소개 (TRB 리비트 소스 추가)

- FMZ 퀀트: 암호화폐 시장에서 공통 요구 사항 설계 예제 분석 (II)

- 80 줄의 코드에서 고주파 전략으로 뇌 없는 판매봇을 이용하는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (II)

- 80줄의 코드의 고주파 전략으로 뇌 없는 로봇을 파는 방법

- FMZ Quant: 암호화폐 시장에서 공통 요구 사항 디자인 예의 분석 (I)

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (1)