빌라 다이내믹 피보트 슈퍼트렌드 전략

저자:차오장, 날짜: 2022-05-13 17:45:05태그:EMASMAATR피브

이 전략은 AUD/USD에서 15 분 시간 프레임에서 더 잘 작동합니다. 다음과 같은 다른 필터에 기반한 트레이드를 입력하기 위해 피보트 슈퍼 트렌드를 사용합니다.

- 간단한 EMA 필터: 3개의 EMA가 순서대로 있어야 합니다.

- DEMA 각: 당신은 DEMA 각의 문턱을 선택할 수 있습니다.

- 간단한 DEMA 필터: 단지 닫는 것이 DEMA 위에 있거나 아래에 있는지 확인

- 모든 슈퍼트렌드 신호를 가져가기: 이것은 모든 정상적인 슈퍼트렌드 신호를 가져가기 위해 피보트 슈퍼트렌드 신호가 거래에 들어갈 때까지 기다리지 않는 것을 의미합니다 (특히 긴 피보트 슈퍼트렌드 기간)

- 슈퍼트렌드에서 Stop Loss: 이것은 Stop Loss가 Normal Supertrend에 위치한다는 것을 의미합니다. 만약 false가 아니라면 선택된 ATR 수준에 Stop Loss가 배치됩니다.

- 2단계 취득: 이것은 당신이 정상적인 슈퍼 트렌드가 입상 가격을 넘으면 지점의 비율을 닫고 싶다면, 당신은

2단계 TP qty 입력에서 %를 선택할 수 있음을 의미합니다. - 스톱 로스 ATR 멀티플라이퍼: 슈퍼트렌드에서 스톱 로스가 꺼진 경우 이것은 atr에 기초한 스톱 로스입니다.

- 이윤 ATR 곱셈: 슈퍼트렌드에서 스톱 로스가 꺼진 경우 이것은 atr를 기반으로 하는 이윤을 취합니다 (이 둘 사이의 비율이 슈퍼트렌드에서 스톱 로스가 발생했을 때 리스크와 리워드 비율을 차지한다는 것을 명심해야합니다)

- 테스트: 과잉 적응을 피하기 위해, 당신은 백테스팅과 전향 테스트를위한 날짜 범위를 선택하고 어떤 테스트를 수행하고 싶은지 선택할 수 있습니다

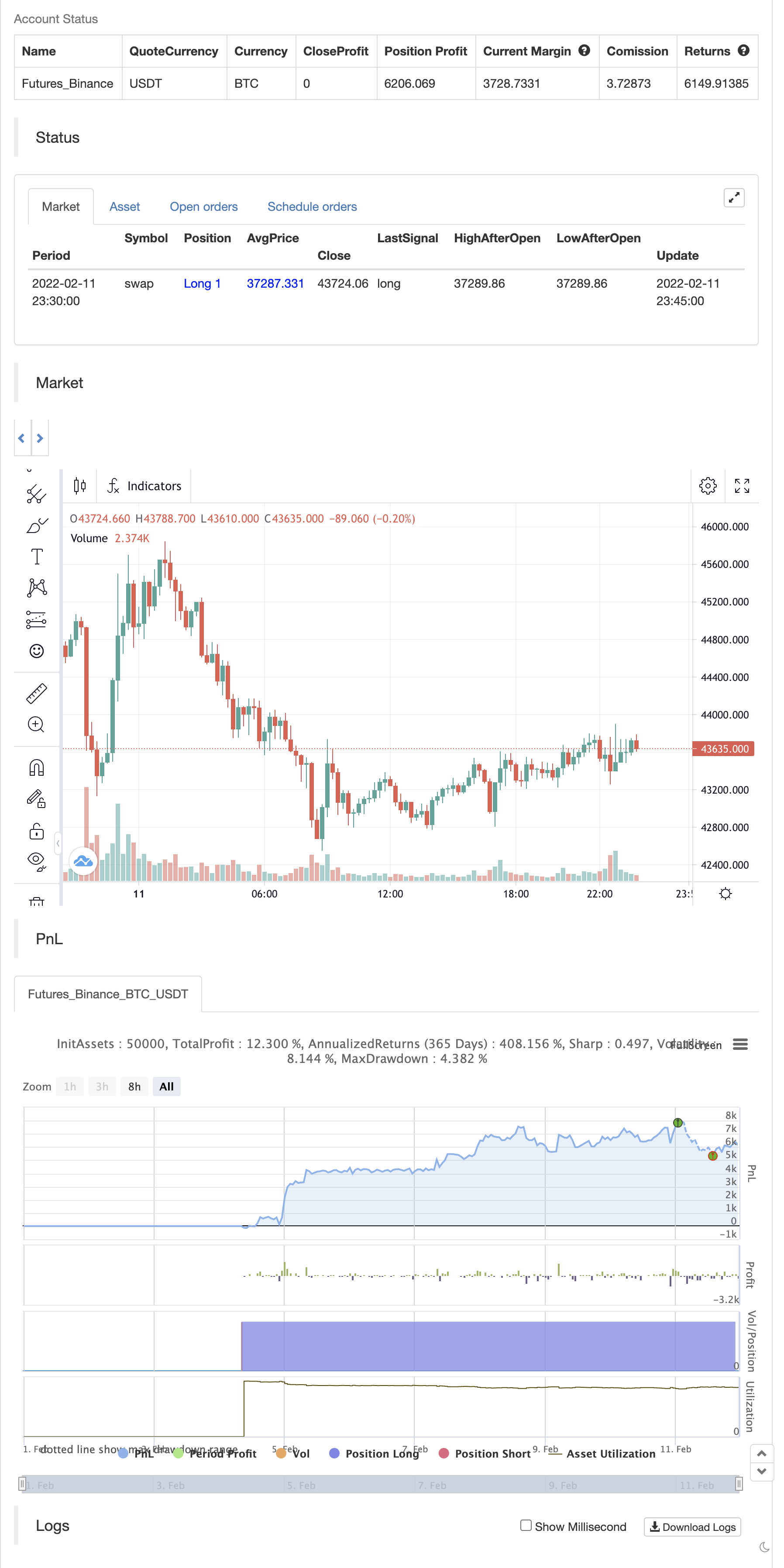

백테스트

/*backtest

start: 2022-02-01 00:00:00

end: 2022-02-11 23:59:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © evillalobos1123

//@version=5

strategy("Villa Dinamic Pivot Supertrend Strategy", overlay=true, calc_on_every_tick = true)

//INPUTS

ema_b = input.bool(false, "Use Simple EMA Filter", group = "Strategy Inputs")

ema_b_ang = input.bool(true, "Use DEMA Angle Filter", group = "Strategy Inputs")

dema_b = input.bool(true, "Use DEMA Filter", group = "Strategy Inputs")

st_sig = input.bool(false, "Take Every Supertrend Signal" , group = "Strategy Inputs")

take_p = input.bool(true, "Stop Loss at Supertrend", group = "Strategy Inputs")

din_tp = input.bool(false, "2 Steps Take Profit", group = "Strategy Inputs")

move_sl = input.bool(true, "Move SL", group = "Strategy Inputs")

sl_atr = input.float(2.5, "Stop Loss ATR Multiplier", group = "Strategy Inputs")

tp_atr = input.float(4, "Take Profit ATR Multiplier", group = "Strategy Inputs")

din_tp_qty = input.int(50, "2 Steps TP qty%", group = "Strategy Inputs")

dema_a_filter = input.float(0, "DEMA Angle Threshold (+ & -)", group = "Strategy Inputs")

dema_a_look = input.int(1, "DEMA Angle Lookback", group = "Strategy Inputs")

dr_test = input.string("All", "Testing", options = ["Backtest", "Forwardtest", "All"], group = "Strategy Inputs")

test_act = input.string('Forex', 'Market', options = ['Forex', 'Stocks'], group = "Strategy Inputs")

not_in_trade = strategy.position_size == 0

//Backtesting date range

start_year = input.int(2021, "Backtesting start year", group = "BT Date Range")

start_month = input.int(1, "Backtesting start month", group = "BT Date Range")

start_date = input.int(1, "Backtesting start day", group = "BT Date Range")

end_year = input.int(2021, "Backtesting end year", group = "BT Date Range")

end_month = input.int(12, "Backtesting end month", group = "BT Date Range")

end_date = input.int(31, "Backtesting end day", group = "BT Date Range")

bt_date_range = (time >= timestamp(syminfo.timezone, start_year,

start_month, start_date, 0, 0)) and

(time < timestamp(syminfo.timezone, end_year, end_month, end_date, 0, 0))

//Forward testing date range

start_year_f = input.int(2022, "Forwardtesting start year", group = "FT Date Range")

start_month_f = input.int(1, "Forwardtesting start month", group = "FT Date Range")

start_date_f = input.int(1, "Forwardtesting start day", group = "FT Date Range")

end_year_f = input.int(2022, "Forwardtesting end year", group = "FT Date Range")

end_month_f = input.int(03, "Forwardtesting end month", group = "FT Date Range")

end_date_f = input.int(26, "Forwardtesting end day", group = "FT Date Range")

ft_date_range = (time >= timestamp(syminfo.timezone, start_year_f,

start_month_f, start_date_f, 0, 0)) and

(time < timestamp(syminfo.timezone, end_year_f, end_month_f, end_date_f, 0, 0))

//date condition

date_range_cond = if dr_test == "Backtest"

bt_date_range

else if dr_test == "Forwardtest"

ft_date_range

else

true

//INDICATORS

//PIVOT SUPERTREND

prd = input.int(2, "PVT ST Pivot Point Period", group = "Pivot Supertrend")

Factor=input.float(3, "PVT ST ATR Factor", group = "Pivot Supertrend")

Pd=input.int(9 , "PVT ST ATR Period", group = "Pivot Supertrend")

// get Pivot High/Low

float ph = ta.pivothigh(prd, prd)

float pl = ta.pivotlow(prd, prd)

// calculate the Center line using pivot points

var float center = na

float lastpp = ph ? ph : pl ? pl : na

if lastpp

if na(center)

center := lastpp

else

//weighted calculation

center := (center * 2 + lastpp) / 3

// upper/lower bands calculation

Up = center - (Factor * ta.atr(Pd))

Dn = center + (Factor * ta.atr(Pd))

// get the trend

float TUp = na

float TDown = na

Trend = 0

TUp := close[1] > TUp[1] ? math.max(Up, TUp[1]) : Up

TDown := close[1] < TDown[1] ? math.min(Dn, TDown[1]) : Dn

Trend := close > TDown[1] ? 1: close < TUp[1]? -1: nz(Trend[1], 1)

Trailingsl = Trend == 1 ? TUp : TDown

// check and plot the signals

bsignal = Trend == 1 and Trend[1] == -1

ssignal = Trend == -1 and Trend[1] == 1

//get S/R levels using Pivot Points

float resistance = na

float support = na

support := pl ? pl : support[1]

resistance := ph ? ph : resistance[1]

//DEMA

dema_ln = input.int(200, "DEMA Len", group = 'D-EMAs')

dema_src = input.source(close, "D-EMAs Source", group = 'D-EMAs')

ema_fd = ta.ema(dema_src, dema_ln)

dema = (2*ema_fd)-(ta.ema(ema_fd,dema_ln))

//EMA

ema1_l = input.int(21, "EMA 1 Len", group = 'D-EMAs')

ema2_l = input.int(50, "EMA 2 Len", group = 'D-EMAs')

ema3_l = input.int(200, "EMA 3 Len", group = 'D-EMAs')

ema1 = ta.ema(dema_src, ema1_l)

ema2 = ta.ema(dema_src, ema2_l)

ema3 = ta.ema(dema_src, ema3_l)

//Supertrend

Periods = input.int(21, "ST ATR Period", group = "Normal Supertrend")

src_st = input.source(hl2, "ST Supertrend Source", group = "Normal Supertrend")

Multiplier = input.float(2.0 , "ST ATR Multiplier", group = "Normal Supertrend")

changeATR= true

atr2 = ta.sma(ta.tr, Periods)

atr3= changeATR ? ta.atr(Periods) : atr2

up=src_st-(Multiplier*atr3)

up1 = nz(up[1],up)

up := close[1] > up1 ? math.max(up,up1) : up

dn=src_st+(Multiplier*atr3)

dn1 = nz(dn[1], dn)

dn := close[1] < dn1 ? math.min(dn, dn1) : dn

trend = 1

trend := nz(trend[1], trend)

trend := trend == -1 and close > dn1 ? 1 : trend == 1 and close < up1 ? -1 : trend

buySignal = trend == 1 and trend[1] == -1

sellSignal = trend == -1 and trend[1] == 1

//ATR

atr = ta.atr(14)

///CONDITIONS

//BUY

/// ema simple

ema_cond_b = if ema_b

ema1 > ema2 and ema2 > ema3

else

true

///ema angle

div_ang = if test_act == 'Forex'

0.0001

else

1

dema_angle_rad = math.atan((dema - dema[dema_a_look])/div_ang)

dema_angle = dema_angle_rad * (180/math.pi)

dema_ang_cond_b = if ema_b_ang

if dema_angle >= dema_a_filter

true

else

false

else

true

///ema distance

dema_cond_b = if dema_b

close > dema

else

true

//supertrends

///if pivot buy sig or (st buy sig and pivot. trend = 1)

pvt_cond_b = bsignal

st_cond_b = if st_sig

buySignal and Trend == 1

else

false

st_entry_cond = pvt_cond_b or st_cond_b

///stop loss tp

sl_b = if take_p

if trend == 1

up

else

close - (atr * sl_atr)

else

close - (atr * sl_atr)

tp_b = if take_p

if trend == 1

close + ((close - up) * (tp_atr / sl_atr))

else

close + (atr * tp_atr)

else

close + (atr * tp_atr)

//position size

init_cap = strategy.equity

pos_size_b = math.round((init_cap * .01) / (close - sl_b))

ent_price = strategy.opentrades.entry_price(strategy.opentrades - 1)

var sl_b_n = 0.0

var tp_b_n = 0.0

longCondition = (ema_cond_b and dema_cond_b and dema_ang_cond_b and st_entry_cond and date_range_cond and not_in_trade)

if (longCondition)

strategy.entry("Long", strategy.long, qty = pos_size_b)

sl_b_n := sl_b

tp_b_n := tp_b

ent_price := strategy.opentrades.entry_price(strategy.opentrades - 1)

if (up[1] < ent_price and up >= ent_price and trend[0] == 1)

if din_tp

strategy.close("Long", qty_percent = din_tp_qty)

if move_sl

sl_b_n := ent_price

strategy.exit("Exit", "Long", stop =sl_b_n, limit = tp_b_n)

//sell

///ema simple

ema_cond_s = if ema_b

ema1 < ema2 and ema2 < ema3

else

true

//ema distance

dema_cond_s = if dema_b

close < dema

else

true

//dema angle

dema_ang_cond_s = if ema_b_ang

if dema_angle <= -(dema_a_filter)

true

else

false

else

true

//supertrends

///if pivot buy sig or (st buy sig and pivot. trend = 1)

pvt_cond_s = ssignal

st_cond_s = if st_sig

sellSignal and Trend == -1

else

false

st_entry_cond_s = pvt_cond_s or st_cond_s

///stop loss tp

sl_s = if take_p

if trend == -1

dn

else

close + (atr * sl_atr)

else

close + (atr * sl_atr)

tp_s = if take_p

if trend == -1

close - ((dn - close) * (tp_atr / sl_atr))

else

close - (atr * tp_atr)

else

close - (atr * tp_atr)

shortCondition = (ema_cond_s and dema_cond_s and dema_ang_cond_s and date_range_cond and st_entry_cond_s and not_in_trade)

pos_size_s = math.round((init_cap * .01) / (sl_s - close))

var sl_s_n = 0.0

var tp_s_n = 0.0

if (shortCondition)

strategy.entry("Short", strategy.short, qty = pos_size_s)

sl_s_n := sl_s

tp_s_n := tp_s

if (dn[1] > ent_price and dn <= ent_price and trend[0] == -1)

if din_tp

strategy.close("Short", qty_percent = din_tp_qty)

if move_sl

sl_s_n := ent_price

strategy.exit("Exit", "Short", stop = sl_s_n, limit = tp_s_n)

관련

- ML 경고 템플릿

- SSL 하이브리드

- ESSMA

- 슈퍼 점프 턴 백 볼링거 밴드

- 슈퍼 스칼퍼

- 슈퍼 스칼퍼 - 5분 15분

- 슈퍼트렌드 이동 평균

- 이윤 극대화 PMax

- 부피 기반의 동적 DCA 전략

- 엘리엇 파동 이론 4-9 충동 파동 자동 탐지 거래 전략

더 많은

- OCC 전략 R5.1

- 곰시장에 오신 것을 환영합니다

- 시드 보스

- 회전점 높은 낮은 멀티 시간 프레임

- 유령 트렌드 추적 전략 데이터베이스

- 유령 트렌드 추적 전략 비즈니스 데이터베이스

- 유령 트렌드 추적 전략

- 레인보우 오시레이터

- 주식 곡선 위치 사이징 거래 예제

- KLineChart 데모

- 크롤의 슈퍼트렌드

- zdmre의 RSI

- FTL - 범위 필터 X2 + EMA + UO

- 브라마스트라

- 모보 밴드

- SAR + 3SMMA와 SL & TP

- SSS

- 달 발사 경고 템플릿 [지표]

- HALFTREND + HEMA + SMA (거짓 신호의 전략)

- RSI: 피보트, BB, SMA, EMA, SMMA, WMA, VWMA와의 분차