Melaksanakan Strategi Dagangan Kuantitatif Mata Wang Digital Dual Thrust di Python

Penulis:Lydia, Dicipta: 2023-01-10 17:07:49, Dikemas kini: 2023-09-20 10:53:48

Melaksanakan Strategi Dagangan Kuantitatif Mata Wang Digital Dual Thrust di Python

Pengenalan kepada algoritma dagangan Dual Thrust

Algoritma perdagangan dorongan berganda adalah strategi perdagangan kuantitatif yang terkenal yang dibangunkan oleh Michael Chalek. Ia biasanya digunakan dalam niaga hadapan, pertukaran asing dan pasaran saham. Konsep dorongan berganda adalah sistem perdagangan terobosan biasa. Ia menggunakan sistem

Dalam artikel ini, kami memberikan butiran logik terperinci strategi ini dan menunjukkan cara melaksanakan algoritma ini di platform FMZ Quant. Pertama sekali, kita perlu memilih harga sejarah subjek yang akan didagangkan. Julat ini dikira berdasarkan harga penutupan, harga tertinggi dan harga terendah N hari terakhir. Apabila pasaran bergerak dalam julat tertentu dari harga pembukaan, buka kedudukan.

Kami menguji strategi ini dengan pasangan perdagangan tunggal di bawah dua keadaan pasaran biasa, iaitu pasaran trend dan pasaran kejutan. Hasilnya menunjukkan bahawa sistem perdagangan momentum berfungsi dengan lebih baik di pasaran trend dan ia akan mencetuskan beberapa isyarat perdagangan yang tidak sah di pasaran yang tidak menentu. Di pasaran selang, kami dapat menyesuaikan parameter untuk mendapatkan pulangan yang lebih baik. Sebagai perbandingan sasaran perdagangan rujukan individu, kami juga menguji pasaran niaga hadapan komoditi domestik. Hasilnya menunjukkan bahawa strategi lebih baik daripada prestasi purata.

Prinsip strategi DT

Prototype logiknya adalah strategi perdagangan intraday yang biasa. Strategi terobosan julat pembukaan adalah berdasarkan harga pembukaan hari ini ditambah atau dikurangkan peratusan tertentu dari julat semalam untuk menentukan trek atas dan bawah. Apabila harga melintasi trek atas, ia akan membuka posisinya untuk membeli, dan apabila ia memecahkan trek bawah, ia akan membuka posisinya untuk pergi pendek.

Prinsip strategi

-

Selepas penutupan, dua nilai dikira: harga tertinggi - harga penutupan, dan harga penutupan - harga terendah. Kemudian ambil nilai yang lebih besar daripada kedua-dua nilai dan kalikan nilai dengan 0.7.

-

Selepas pasaran dibuka keesokan harinya, catat harga pembukaan, dan beli segera apabila harga melebihi (harga pembukaan + nilai pencetus), atau jual kedudukan pendek apabila harga lebih rendah daripada (harga pembukaan - nilai pencetus).

-

Strategi ini tidak mempunyai stop loss yang jelas. Sistem ini adalah sistem terbalik, iaitu, jika terdapat pesanan kedudukan pendek apabila harga melebihi (harga pembukaan + nilai pencetus), ia akan menghantar dua pesanan beli (satu menutup kedudukan yang salah, yang lain membuka kedudukan yang betul). Untuk sebab yang sama, jika harga kedudukan panjang lebih rendah daripada (harga pembukaan - nilai pencetus), ia akan menghantar dua pesanan jual.

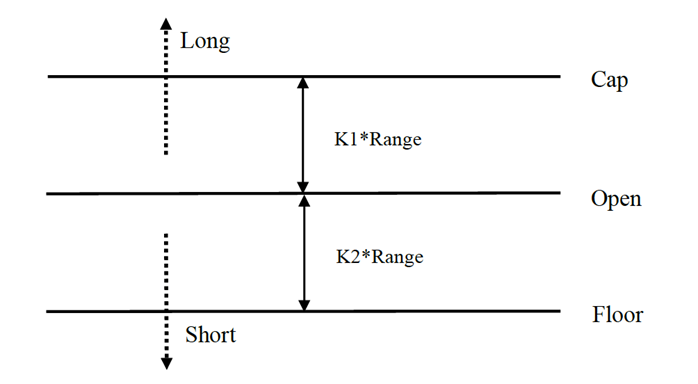

Ekspresi matematik strategi DT

Julat = maksimum (HH-LC, HC-LL)

Kaedah pengiraan isyarat kedudukan panjang ialah:

cap = terbuka + K1 × Rangecap = terbuka + K1 × Range

Kaedah pengiraan isyarat kedudukan pendek ialah:

lantai = terbuka

Di mana K1 dan K2 adalah parameter. Apabila K1 lebih besar daripada K2, isyarat kedudukan panjang dicetuskan, dan sebaliknya. Untuk demonstrasi, kita memilih K1 = K2 = 0.5. Dalam transaksi sebenar, kita masih boleh menggunakan data sejarah untuk mengoptimumkan parameter ini atau menyesuaikan parameter mengikut trend pasaran. Jika anda bullish, K1 harus kurang daripada K2. Jika anda bearish, K1 harus lebih besar daripada K2.

Sistem ini adalah sistem pembalikan. Oleh itu, jika pelabur memegang kedudukan pendek apabila harga melintasi trek atas, mereka harus menutup kedudukan pendek sebelum membuka kedudukan panjang. Jika pelabur memegang kedudukan panjang apabila harga memecahkan trek bawah, mereka harus menutup kedudukan panjang sebelum membuka kedudukan pendek baru.

Penambahbaikan strategi DT:

Dalam tetapan julat, empat titik harga (tinggi, terbuka, rendah dan ditutup) dari N hari sebelumnya diperkenalkan untuk menjadikan julat agak stabil dalam tempoh tertentu, yang boleh digunakan untuk mengesan trend harian.

Syarat pemicu pembukaan kedudukan panjang dan pendek strategi, memandangkan julat asimetrik, julat rujukan urus niaga panjang dan pendek harus memilih bilangan tempoh yang berbeza, yang juga boleh ditentukan oleh parameter K1 dan K2. Apabila K1 < K2, isyarat kedudukan panjang agak mudah dipicu, manakala apabila K1 > K2, isyarat kedudukan pendek agak mudah dipicu.

Oleh itu, apabila menggunakan strategi ini, di satu pihak, anda boleh merujuk kepada parameter terbaik backtesting data sejarah. Di sisi lain, anda boleh menyesuaikan K1 dan K2 secara berperingkat mengikut penilaian anda tentang masa depan atau indikator teknikal tempoh utama yang lain.

Ini adalah kaedah perdagangan biasa menunggu isyarat, memasuki pasaran, arbitrage, dan kemudian meninggalkan pasaran, tetapi kesannya sangat baik.

Menerbitkan strategi DT pada platform FMZ Quant

Kita buka.FMZ.COM, log masuk ke akaun, klik Dashboard, dan menggunakan docker dan robot.

Sila rujuk artikel saya sebelum ini mengenai cara menggunakan docker dan robot:https://www.fmz.com/bbs-topic/9864.

Pembaca yang ingin membeli pelayan pengkomputeran awan mereka sendiri untuk menggunakan pelabuhan boleh merujuk artikel ini:https://www.fmz.com/digest-topic/5711.

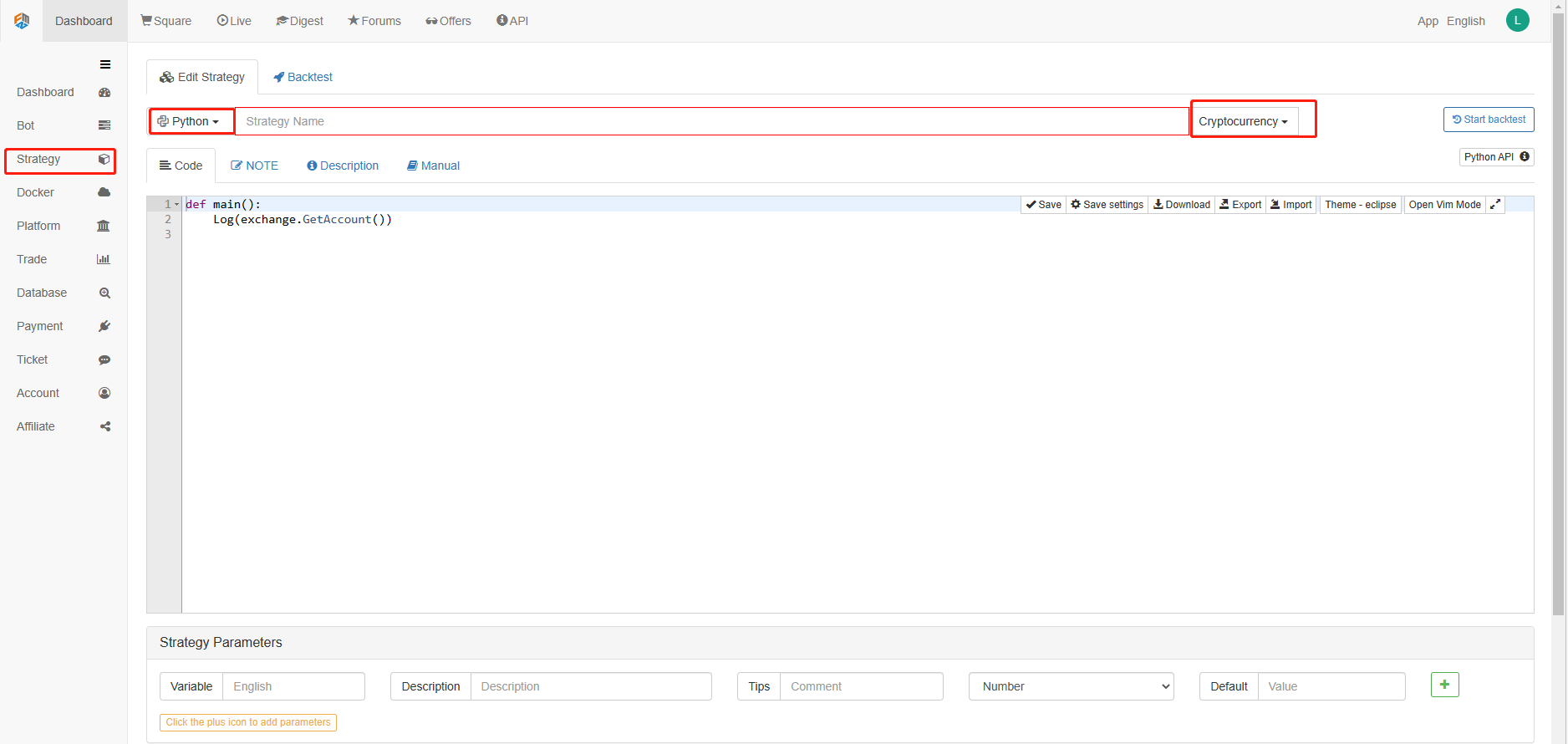

Seterusnya, kita klik pada Perpustakaan Strategi di lajur kiri dan klik pada Tambah strategi.

Ingat untuk memilih bahasa pengaturcaraan sebagai Python di sudut kanan atas halaman penyuntingan strategi, seperti yang ditunjukkan dalam gambar:

Seterusnya, kita akan menulis kod Python ke dalam halaman penyuntingan kod. Kod berikut mempunyai komen baris demi baris yang sangat terperinci, anda boleh mengambil masa anda untuk memahami.

Kami akan menggunakan niaga hadapan OKCoin untuk menguji strategi:

import time # Here we need to introduce the time library that comes with python, which will be used later in the program.

class Error_noSupport(BaseException): # We define a global class named ChartCfg to initialize the strategy chart settings. Object has many attributes about the chart function. Chart library: HighCharts.

def __init__(self): # log out prompt messages

Log("Support OKCoin Futures only! #FF0000")

class Error_AtBeginHasPosition(BaseException):

def __init__(self):

Log("Start with a futures position! #FF0000")

ChartCfg = {

'__isStock': True, # This attribute is used to control whether to display a single control data series (you can cancel the display of a single data series on the chart). If you specify __isStock: false, it will be displayed as a normal chart.

'title': { # title is the main title of the chart

'text': 'Dual Thrust upper and bottom track chart' # An attribute of the title text is the text of the title, here set to 'Dual Thrust upper and bottom track chart' the text will be displayed in the title position.

},

'yAxis': { # Settings related to the Y-axis of the chart coordinate.

'plotLines': [{ # Horizontal lines on the Y-axis (perpendicular to the Y-axis), the value of this attribute is an array, i.e. the setting of multiple horizontal lines.

'value': 0, # Coordinate value of horizontal line on Y-axis

'color': 'red', # Color of horizontal line

'width': 2, # Line width of horizontal line

'label': { # Labels on the horizontal line

'text': 'Upper track', # Text of the label

'align': 'center' # The display position of the label, here set to center (i.e.: 'center')

},

}, { # The second horizontal line ([{...} , {...}] the second element in the array)

'value': 0, # Coordinate value of horizontal line on Y-axis

'color': 'green', # Color of horizontal line

'width': 2, # Line width of horizontal line

'label': { # Label

'text': 'bottom track',

'align': 'center'

},

}]

},

'series': [{ # Data series, that is, data used to display data lines, K-lines, tags, and other contents on the chart. It is also an array whose first index is 0.

'type': 'candlestick', # Type of data series with index 0: 'candlestick' indicates a K-line chart.

'name': 'Current period', # Name of the data series

'id': 'primary', # The ID of the data series, which is used for the related settings of the next data series.

'data': [] # An array of data series to store specific K-line data

}, {

'type': 'flags', # Data series, type: 'flags', display labels on the chart, indicating going long and going short. Index is 1.

'onSeries': 'primary', # This attribute indicates that the label is displayed on id 'primary'.

'data': [] # The array that holds the label data.

}]

}

STATE_IDLE = 0 # Status constants, indicating idle

STATE_LONG = 1 # Status constants, indicating long positions

STATE_SHORT = 2 # Status constants, indicating short positions

State = STATE_IDLE # Indicates the current program status, assigned as idle initially

LastBarTime = 0 # The time stamp of the last column of the K-line (in milliseconds, 1000 milliseconds is equal to 1 second, and the timestamp is the number of milliseconds from January 1, 1970 to the present time is a large positive integer).

UpTrack = 0 # Upper track value

BottomTrack = 0 # Bottom track value

chart = None # It is used to accept the chart control object returned by the Chart API function. Use this object (chart) to call its member function to write data to the chart.

InitAccount = None # Initial account status

LastAccount = None # Latest account status

Counter = { # Counters for recording profit and loss counts

'w': 0, # Number of wins

'l': 0 # Number of losses

}

def GetPosition(posType): # Define a function to store account position information

positions = exchange.GetPosition() # exchange.GetPosition() is the FMZ Quant official API. For its usage, please refer to the official API document: https://www.fmz.com/api.

return [{'Price': position['Price'], 'Amount': position['Amount']} for position in positions if position['Type'] == posType] # Return to various position information

def CancelPendingOrders(): # Define a function specifically for withdrawing orders

while True: # Loop check

orders = exchange.GetOrders() # If there is a position

[exchange.CancelOrder(order['Id']) for order in orders if not Sleep(500)] # Withdrawal statement

if len(orders) == 0: # Logical judgment

break

def Trade(currentState,nextState): # Define a function to determine the order placement logic.

global InitAccount,LastAccount,OpenPrice,ClosePrice # Define the global scope

ticker = _C(exchange.GetTicker) # For the usage of _C, please refer to: https://www.fmz.com/api.

slidePrice = 1 # Define the slippage value

pfn = exchange.Buy if nextState == STATE_LONG else exchange.Sell # Buying and selling judgment logic

if currentState != STATE_IDLE: # Loop start

Log(_C(exchange.GetPosition)) # Log information

exchange.SetDirection("closebuy" if currentState == STATE_LONG else "closesell") # Adjust the order direction, especially after placing the order.

while True:

ID = pfn( (ticker['Last'] - slidePrice) if currentState == STATE_LONG else (ticker['Last'] + slidePrice), AmountOP) # Price limit order, ID=pfn (- 1, AmountOP) is the market price order, ID=pfn (AmountOP) is the market price order.

Sleep(Interval) # Take a break to prevent the API from being accessed too often and your account being blocked.

Log(exchange.GetOrder(ID)) # Log information

ClosePrice = (exchange.GetOrder(ID))['AvgPrice'] # Set the closing price

CancelPendingOrders() # Call the withdrawal function

if len(GetPosition(PD_LONG if currentState == STATE_LONG else PD_SHORT)) == 0: # Order withdrawal logic

break

account = exchange.GetAccount() # Get account information

if account['Stocks'] > LastAccount['Stocks']: # If the current account currency value is greater than the previous account currency value.

Counter['w'] += 1 # In the profit and loss counter, add one to the number of profits.

else:

Counter['l'] += 1 # Otherwise, add one to the number of losses.

Log(account) # log information

LogProfit((account['Stocks'] - InitAccount['Stocks']),"Return rates:", ((account['Stocks'] - InitAccount['Stocks']) * 100 / InitAccount['Stocks']),'%')

Cal(OpenPrice,ClosePrice)

LastAccount = account

exchange.SetDirection("buy" if nextState == STATE_LONG else "sell") # The logic of this part is the same as above and will not be elaborated.

Log(_C(exchange.GetAccount))

while True:

ID = pfn( (ticker['Last'] + slidePrice) if nextState == STATE_LONG else (ticker['Last'] - slidePrice), AmountOP)

Sleep(Interval)

Log(exchange.GetOrder(ID))

CancelPendingOrders()

pos = GetPosition(PD_LONG if nextState == STATE_LONG else PD_SHORT)

if len(pos) != 0:

Log("Average price of positions",pos[0]['Price'],"Amount:",pos[0]['Amount'])

OpenPrice = (exchange.GetOrder(ID))['AvgPrice']

Log("now account:",exchange.GetAccount())

break

def onTick(exchange): # The main function of the program, within which the main logic of the program is processed.

global LastBarTime,chart,State,UpTrack,DownTrack,LastAccount # Define the global scope

records = exchange.GetRecords() # For the usage of exchange.GetRecords(), please refer to: https://www.fmz.com/api.

if not records or len(records) <= NPeriod: # Judgment statements to prevent accidents.

return

Bar = records[-1] # Take the penultimate element of records K-line data, that is, the last bar.

if LastBarTime != Bar['Time']:

HH = TA.Highest(records, NPeriod, 'High') # Declare the HH variable, call the TA.Highest function to calculate the maximum value of the highest price in the current K-line data NPeriod period and assign it to HH.

HC = TA.Highest(records, NPeriod, 'Close') # Declare the HC variable to get the maximum value of the closing price in the NPeriod period.

LL = TA.Lowest(records, NPeriod, 'Low') # Declare the LL variable to get the minimum value of the lowest price in the NPeriod period.

LC = TA.Lowest(records, NPeriod, 'Close') # Declare LC variable to get the minimum value of the closing price in the NPeriod period. For specific TA-related applications, please refer to the official API documentation.

Range = max(HH - LC, HC - LL) # Calculate the range

UpTrack = _N(Bar['Open'] + (Ks * Range)) # The upper track value is calculated based on the upper track factor Ks of the interface parameters such as the opening price of the latest K-line bar.

DownTrack = _N(Bar['Open'] - (Kx * Range)) # Calculate the down track value

if LastBarTime > 0: # Because the value of LastBarTime initialization is set to 0, LastBarTime>0 must be false when running here for the first time. The code in the if block will not be executed, but the code in the else block will be executed.

PreBar = records[-2] # Declare a variable means "the previous Bar" assigns the value of the penultimate Bar of the current K-line to it.

chart.add(0, [PreBar['Time'], PreBar['Open'], PreBar['High'], PreBar['Low'], PreBar['Close']], -1) # Call the add function of the chart icon control class to update the K-line data (use the penultimate bar of the obtained K-line data to update the last bar of the icon, because a new K-line bar is generated).

else: # For the specific usage of the chart.add function, see the API documentation and the articles in the forum. When the program runs for the first time, it must execute the code in the else block. The main function is to add all the K-lines obtained for the first time to the chart at one time.

for i in range(len(records) - min(len(records), NPeriod * 3), len(records)): # Here, a for loop is executed. The number of loops uses the minimum of the K-line length and 3 times the NPeriod, which can ensure that the initial K-line will not be drawn too much and too long. Indexes vary from large to small.

b = records[i] # Declare a temporary variable b to retrieve the K-line bar data with the index of records.length - i for each loop.

chart.add(0,[b['Time'], b['Open'], b['High'], b['Low'], b['Close']]) # Call the chart.add function to add a K-line bar to the chart. Note that if the last parameter of the add function is passed in -1, it will update the last Bar (column) on the chart. If no parameter is passed in, it will add Bar to the last. After executing the loop of i=2 (i-- already, now it's 1), it will trigger i > 1 for false to stop the loop. It can be seen that the code here only processes the bar of records.length - 2, and the last Bar is not processed.

chart.add(0,[Bar['Time'], Bar['Open'], Bar['High'], Bar['Low'], Bar['Close']]) # Since the two branches of the above if do not process the bar of records.length - 1, it is processed here. Add the latest Bar to the chart.

ChartCfg['yAxis']['plotLines'][0]['value'] = UpTrack # Assign the calculated upper track value to the chart object (different from the chart control object chart) for later display.

ChartCfg['yAxis']['plotLines'][1]['value'] = DownTrack # Assign lower track value

ChartCfg['subtitle'] = { # Set subtitle

'text': 'upper tarck' + str(UpTrack) + 'down track' + str(DownTrack) # Subtitle text setting. The upper and down track values are displayed on the subtitle.

}

chart.update(ChartCfg) # Update charts with chart class ChartCfg.

chart.reset(PeriodShow) # Refresh the PeriodShow variable set according to the interface parameters, and only keep the K-line bar of the number of PeriodShow values.

LastBarTime = Bar['Time'] # The timestamp of the newly generated Bar is updated to LastBarTime to determine whether the last Bar of the K-line data acquired in the next loop is a newly generated one.

else: # If LastBarTime is equal to Bar.Time, that is, no new K-line Bar is generated. Then execute the code in {..}.

chart.add(0,[Bar['Time'], Bar['Open'], Bar['High'], Bar['Low'], Bar['Close']], -1) # Update the last K-line bar on the chart with the last Bar of the current K-line data (the last Bar of the K-line, i.e. the Bar of the current period, is constantly changing).

LogStatus("Price:", Bar["Close"], "up:", UpTrack, "down:", DownTrack, "wins:", Counter['w'], "losses:", Counter['l'], "Date:", time.time()) # The LogStatus function is called to display the data of the current strategy on the status bar.

msg = "" # Define a variable msg.

if State == STATE_IDLE or State == STATE_SHORT: # Judge whether the current state variable State is equal to idle or whether State is equal to short position. In the idle state, it can trigger long position, and in the short position state, it can trigger a long position to be closed and sell the opening position.

if Bar['Close'] >= UpTrack: # If the closing price of the current K-line is greater than the upper track value, execute the code in the if block.

msg = "Go long, trigger price:" + str(Bar['Close']) + "upper track" + str(UpTrack) # Assign a value to msg and combine the values to be displayed into a string.

Log(msg) # message

Trade(State, STATE_LONG) # Call the Trade function above to trade.

State = STATE_LONG # Regardless of opening long positions or selling the opening position, the program status should be updated to hold long positions at the moment.

chart.add(1,{'x': Bar['Time'], 'color': 'red', 'shape': 'flag', 'title': 'long', 'text': msg}) # Add a marker to the corresponding position of the K-line to show the open long position.

if State == STATE_IDLE or State == STATE_LONG: # The short direction is the same as the above, and will not be repeated. The code is exactly the same.

if Bar['Close'] <= DownTrack:

msg = "Go short, trigger price:" + str(Bar['Close']) + "down track" + str(DownTrack)

Log(msg)

Trade(State, STATE_SHORT)

State = STATE_SHORT

chart.add(1,{'x': Bar['Time'], 'color': 'green', 'shape': 'circlepin', 'title': 'short', 'text': msg})

OpenPrice = 0 # Initialize OpenPrice and ClosePrice

ClosePrice = 0

def Cal(OpenPrice, ClosePrice): # Define a Cal function to calculate the profit and loss of the strategy after it has been run.

global AmountOP,State

if State == STATE_SHORT:

Log(AmountOP,OpenPrice,ClosePrice,"Profit and loss of the strategy:", (AmountOP * 100) / ClosePrice - (AmountOP * 100) / OpenPrice, "Currencies, service charge:", - (100 * AmountOP * 0.0003), "USD, equivalent to:", _N( - 100 * AmountOP * 0.0003/OpenPrice,8), "Currencies")

Log(((AmountOP * 100) / ClosePrice - (AmountOP * 100) / OpenPrice) + (- 100 * AmountOP * 0.0003/OpenPrice))

if State == STATE_LONG:

Log(AmountOP,OpenPrice,ClosePrice,"Profit and loss of the strategy:", (AmountOP * 100) / OpenPrice - (AmountOP * 100) / ClosePrice, "Currencies, service charge:", - (100 * AmountOP * 0.0003), "USD, equivalent to:", _N( - 100 * AmountOP * 0.0003/OpenPrice,8), "Currencies")

Log(((AmountOP * 100) / OpenPrice - (AmountOP * 100) / ClosePrice) + (- 100 * AmountOP * 0.0003/OpenPrice))

def main(): # The main function of the strategy program. (entry function)

global LoopInterval,chart,LastAccount,InitAccount # Define the global scope

if exchange.GetName() != 'Futures_OKCoin': # Judge if the name of the added exchange object (obtained by the exchange.GetName function) is not equal to 'Futures_OKCoin', that is, the object added is not OKCoin futures exchange object.

raise Error_noSupport # Throw an exception

exchange.SetRate(1) # Set various parameters of the exchange.

exchange.SetContractType(["this_week","next_week","quarter"][ContractTypeIdx]) # Determine which specific contract to trade.

exchange.SetMarginLevel([10,20][MarginLevelIdx]) # Set the margin rate, also known as leverage.

if len(exchange.GetPosition()) > 0: # Set up fault tolerance mechanism.

raise Error_AtBeginHasPosition

CancelPendingOrders()

InitAccount = LastAccount = exchange.GetAccount()

LoopInterval = min(1,LoopInterval)

Log("Trading platforms:",exchange.GetName(), InitAccount)

LogStatus("Ready...")

LogProfitReset()

chart = Chart(ChartCfg)

chart.reset()

LoopInterval = max(LoopInterval, 1)

while True: # Loop the whole transaction logic and call the onTick function.

onTick(exchange)

Sleep(LoopInterval * 1000) # Take a break to prevent the API from being accessed too frequently and the account from being blocked.

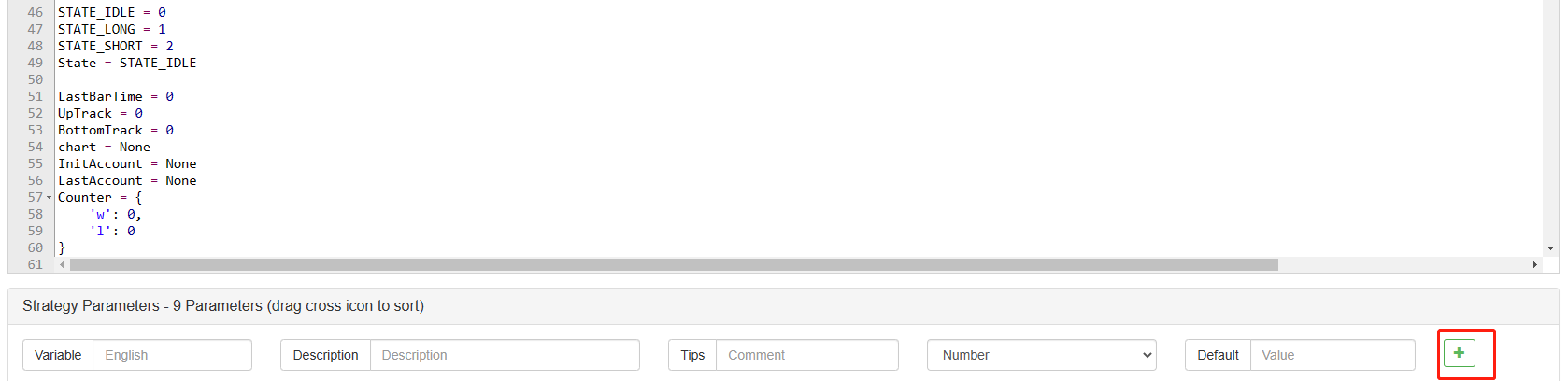

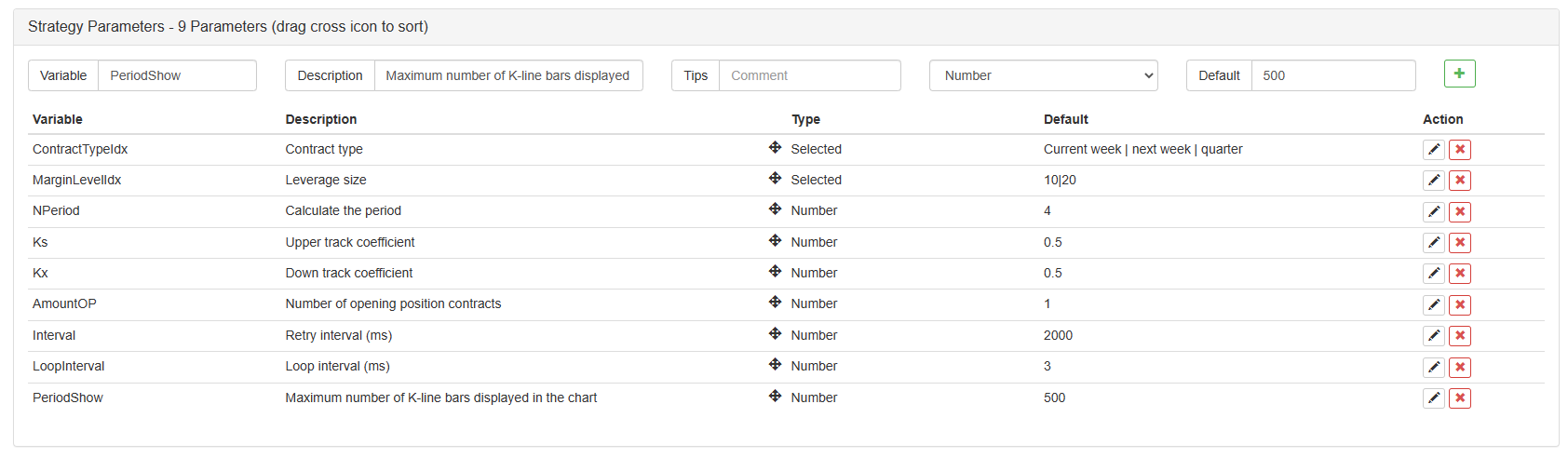

Selepas menulis kod, sila ambil perhatian bahawa kita belum menyelesaikan keseluruhan strategi. Seterusnya, kita perlu menambah parameter yang digunakan dalam strategi ke halaman penyuntingan strategi. Kaedah penambahan sangat mudah. Hanya klik tanda tambah di bahagian bawah kotak dialog penulisan strategi untuk menambah satu demi satu.

Kandungan yang akan ditambah:

Setakat ini, kita akhirnya telah menyelesaikan penulisan strategi. Seterusnya, mari kita mula menguji strategi.

Ujian belakang strategi

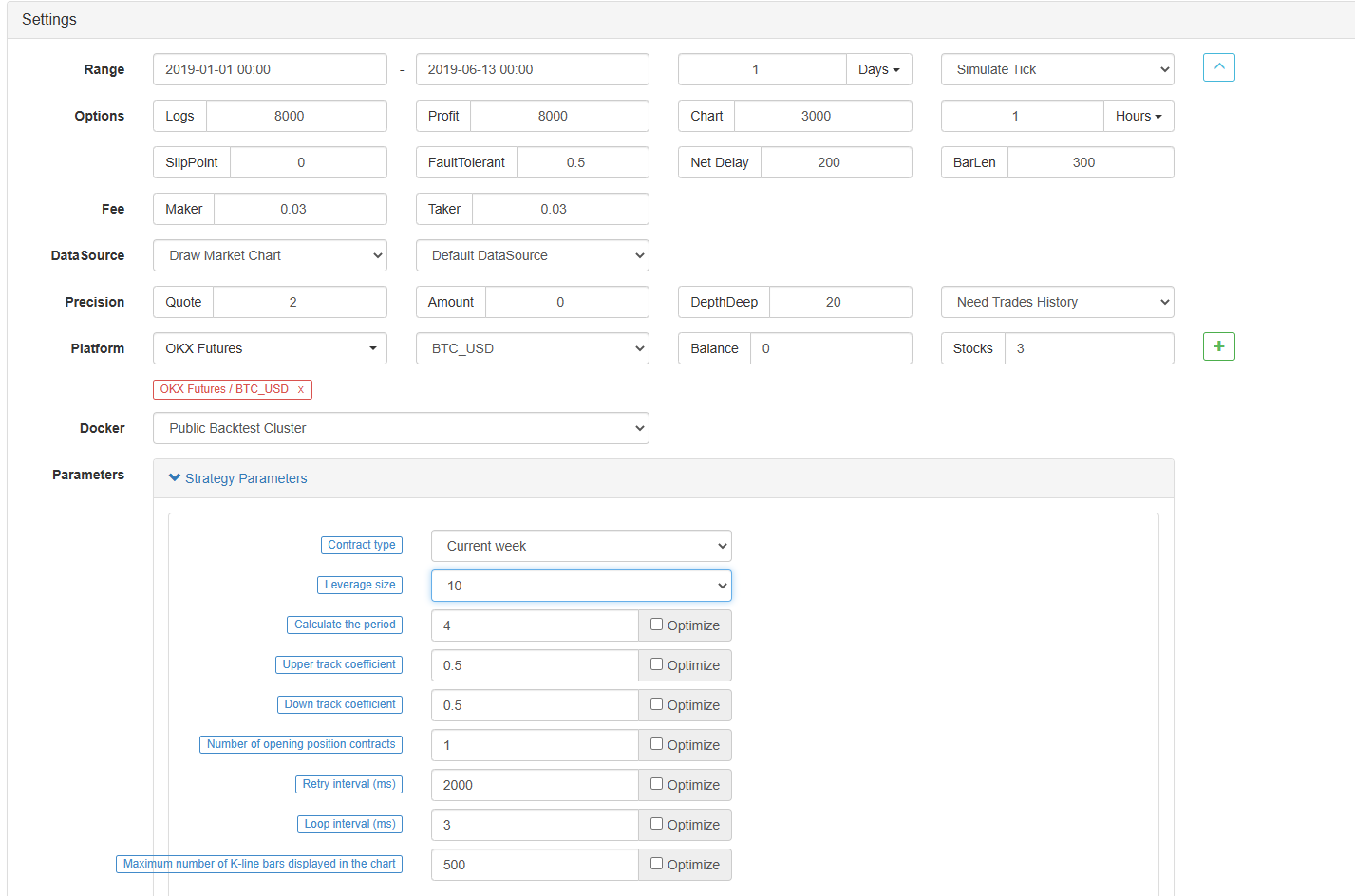

Selepas menulis strategi, perkara pertama yang perlu kita lakukan adalah mengujinya untuk melihat bagaimana ia bertindak dalam data sejarah. Tetapi sila ambil perhatian bahawa hasil backtest tidak sama dengan ramalan masa depan. Backtest hanya boleh digunakan sebagai rujukan untuk mempertimbangkan keberkesanan strategi kita. Sebaik sahaja pasaran berubah dan strategi mula mengalami kerugian besar, kita harus mencari masalah pada waktunya, dan kemudian mengubah strategi untuk menyesuaikan diri dengan persekitaran pasaran baru, seperti ambang yang disebutkan di atas. Jika strategi mempunyai kerugian lebih besar daripada 10%, kita harus segera menghentikan operasi strategi, dan kemudian mencari masalah. Kita boleh mula dengan menyesuaikan ambang.

Klik backtest di halaman penyuntingan strategi. Pada halaman backtest, penyesuaian parameter boleh dilakukan dengan mudah dan cepat mengikut keperluan yang berbeza. Terutamanya untuk strategi dengan logik yang kompleks dan banyak parameter, tidak perlu kembali ke kod sumber dan mengubahsuai satu demi satu.

Masa backtest adalah enam bulan terakhir. Klik Tambah bursa OKCoin Futures dan pilih sasaran dagangan BTC.

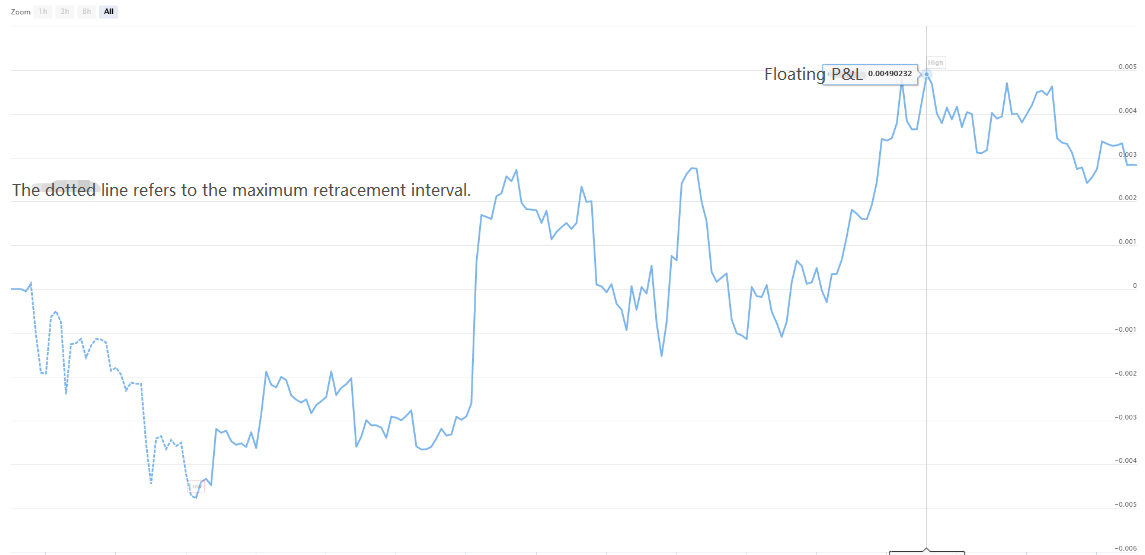

Ia dapat dilihat bahawa strategi ini telah menuai pulangan yang baik dalam tempoh enam bulan yang lalu kerana trend BTC yang sangat baik.

Jika anda mempunyai sebarang soalan, anda boleh meninggalkan mesej dihttps://www.fmz.com/bbs, sama ada mengenai strategi atau teknologi platform, platform FMZ Quant mempunyai profesional bersedia untuk menjawab soalan anda.

- Mengukur Analisis Dasar di Pasaran Cryptocurrency: Biarkan Data Bercakap Sendiri!

- Perbincangan mengenai kajian kuantitatif asas dalam lingkaran mata wang - jangan mempercayai guru-guru sihir yang bodoh, data adalah objektif!

- Alat penting dalam bidang transaksi kuantitatif - Pencipta modul pencarian data kuantitatif

- Menguasai Semuanya - Pengenalan kepada FMZ Versi Baru Terminal Dagangan (dengan Kod Sumber Arbitraj TRB)

- Menguasai segala-galanya FMZ versi baru terminal perdagangan pengenalan (tambahan kod sumber TRB suite)

- FMZ Quant: Analisis Contoh Reka Bentuk Keperluan Umum di Pasaran Cryptocurrency (II)

- Bagaimana untuk mengeksploitasi bot jualan tanpa otak dengan strategi frekuensi tinggi dalam 80 baris kod

- FMZ Kuantitatif: Penyelesaian contoh reka bentuk permintaan biasa di pasaran mata wang kripto (II)

- Bagaimana untuk mengeksploitasi robot tanpa otak yang dijual dengan strategi frekuensi tinggi 80 baris kod

- FMZ Quant: Analisis Contoh Reka Bentuk Keperluan Umum di Pasaran Cryptocurrency (I)

- FMZ Kuantitatif: Penyelesaian contoh reka bentuk permintaan biasa di pasaran mata wang kripto