Estratégia de grade simples na versão Python

Autora:Lydia., Criado: 2022-12-23 21:00:45, Atualizado: 2023-09-20 11:17:48

Estratégia de grade simples na versão Python

Não há muitas estratégias Python no quadrado de estratégia. Uma versão Python da estratégia de grade é escrita aqui. O princípio da estratégia é muito simples. Uma série de nós de grade são gerados por uma distância de preço fixo dentro de uma faixa de preços. Quando o mercado muda e o preço atinge uma posição de preço de nodo de grade, uma ordem de compra é colocada. Quando a ordem é fechada, ou seja, de acordo com o preço da ordem pendente mais o spread de lucro, uma ordem de venda é pendente para fechar a posição. Capture flutuações dentro da faixa de preço definida.

É claro que o risco da estratégia de grade é que qualquer estratégia de tipo grade é uma aposta de que o preço flutua em uma certa faixa. Uma vez que o preço sai da faixa de grade, pode causar sérias perdas flutuantes. Portanto, o propósito de escrever esta estratégia é fornecer referência para ideias de estratégia Python ou design de programa. Esta estratégia é usada apenas para aprendizado e pode ser arriscada no bot real.

A explicação das ideias de estratégia está escrita directamente nos comentários do código de estratégia.

Código de estratégia

'''backtest

start: 2019-07-01 00:00:00

end: 2020-01-03 00:00:00

period: 1m

exchanges: [{"eid":"OKEX","currency":"BTC_USDT"}]

'''

import json

# Parameters

beginPrice = 5000 # Grid interval begin price

endPrice = 8000 # Grid interval end price

distance = 20 # Price distance of each grid node

pointProfit = 50 # Profit spread per grid node

amount = 0.01 # Number of pending orders per grid node

minBalance = 300 # Minimum fund balance of the account (at the time of purchase)

# Global variables

arrNet = []

arrMsg = []

acc = None

def findOrder (orderId, NumOfTimes, ordersList = []) :

for j in range(NumOfTimes) :

orders = None

if len(ordersList) == 0:

orders = _C(exchange.GetOrders)

else :

orders = ordersList

for i in range(len(orders)):

if orderId == orders[i]["Id"]:

return True

Sleep(1000)

return False

def cancelOrder (price, orderType) :

orders = _C(exchange.GetOrders)

for i in range(len(orders)) :

if price == orders[i]["Price"] and orderType == orders[i]["Type"]:

exchange.CancelOrder(orders[i]["Id"])

Sleep(500)

def checkOpenOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "pending" :

orderId = exchange.Sell(arrNet[i]["coverPrice"], arrNet[i]["amount"], arrNet[i], ticker)

if orderId :

arrNet[i]["state"] = "cover"

arrNet[i]["id"] = orderId

else :

# Cancel

cancelOrder(arrNet[i]["coverPrice"], ORDER_TYPE_SELL)

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

def checkCoverOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "cover" :

arrNet[i]["id"] = -1

arrNet[i]["state"] = "idle"

Log(arrNet[i], "The node closes the position and resets to the idle state.", "#FF0000")

def onTick () :

global arrNet, arrMsg, acc

ticker = _C(exchange.GetTicker) # Get the latest current ticker every time

for i in range(len(arrNet)): # Iterate through all grid nodes, find out the position where you need to pend a buy order according to the current market, and pend a buy order.

if i != len(arrNet) - 1 and arrNet[i]["state"] == "idle" and ticker.Sell > arrNet[i]["price"] and ticker.Sell < arrNet[i + 1]["price"]:

acc = _C(exchange.GetAccount)

if acc.Balance < minBalance : # If there is not enough money left, you can only jump out and do nothing.

arrMsg.append("Insufficient funds" + json.dumps(acc) + "!" + ", time:" + _D())

break

orderId = exchange.Buy(arrNet[i]["price"], arrNet[i]["amount"], arrNet[i], ticker) # Pending buy orders

if orderId :

arrNet[i]["state"] = "pending" # Update the grid node status and other information if the buy order is successfully pending

arrNet[i]["id"] = orderId

else :

# Cancel h/the order

cancelOrder(arrNet[i]["price"], ORDER_TYPE_BUY) # Cancel orders by using the cancel function

arrMsg.append("Pending order failed!" + json.dumps(arrNet[i]) + ", time:" + _D())

Sleep(1000)

orders = _C(exchange.GetOrders)

checkOpenOrders(orders, ticker) # Check the status of all buy orders and process them according to the changes.

Sleep(1000)

orders = _C(exchange.GetOrders)

checkCoverOrders(orders, ticker) # Check the status of all sell orders and process them according to the changes.

# The following information about the construction status bar can be found in the FMZ API documentation.

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

while len(arrMsg) > 20 :

arrMsg.pop(0)

for i in range(len(arrMsg)) :

errTbl["rows"].append([i, json.dumps(arrMsg[i])])

for i in range(len(orders)) :

orderTbl["rows"].append([i, json.dumps(orders[i])])

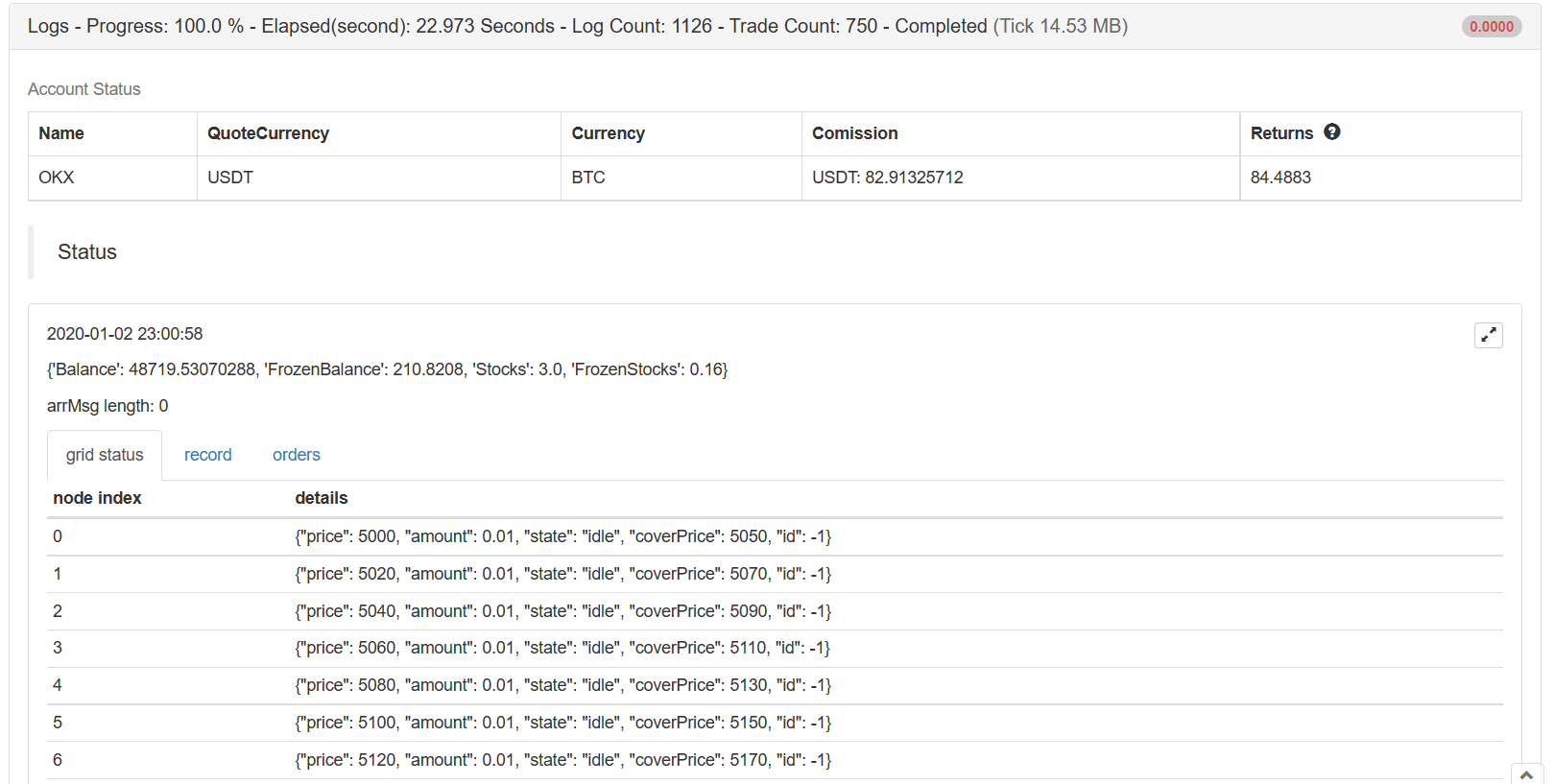

LogStatus(_D(), "\n", acc, "\n", "arrMsg length:", len(arrMsg), "\n", "`" + json.dumps([tbl, errTbl, orderTbl]) + "`")

def main (): # Strategy execution starts here

global arrNet

for i in range(int((endPrice - beginPrice) / distance)): # The for loop constructs a data structure for the grid based on the parameters, a list that stores each grid node, with the following information for each grid node:

arrNet.append({

"price" : beginPrice + i * distance, # Price of the node

"amount" : amount, # Number of orders

"state" : "idle", # pending / cover / idle # Node Status

"coverPrice" : beginPrice + i * distance + pointProfit, # Node closing price

"id" : -1, # ID of the current order related to the node

})

while True: # After the grid data structure is constructed, enter the main strategy loop

onTick() # Processing functions on the main loop, the main processing logic

Sleep(500) # Control polling frequency

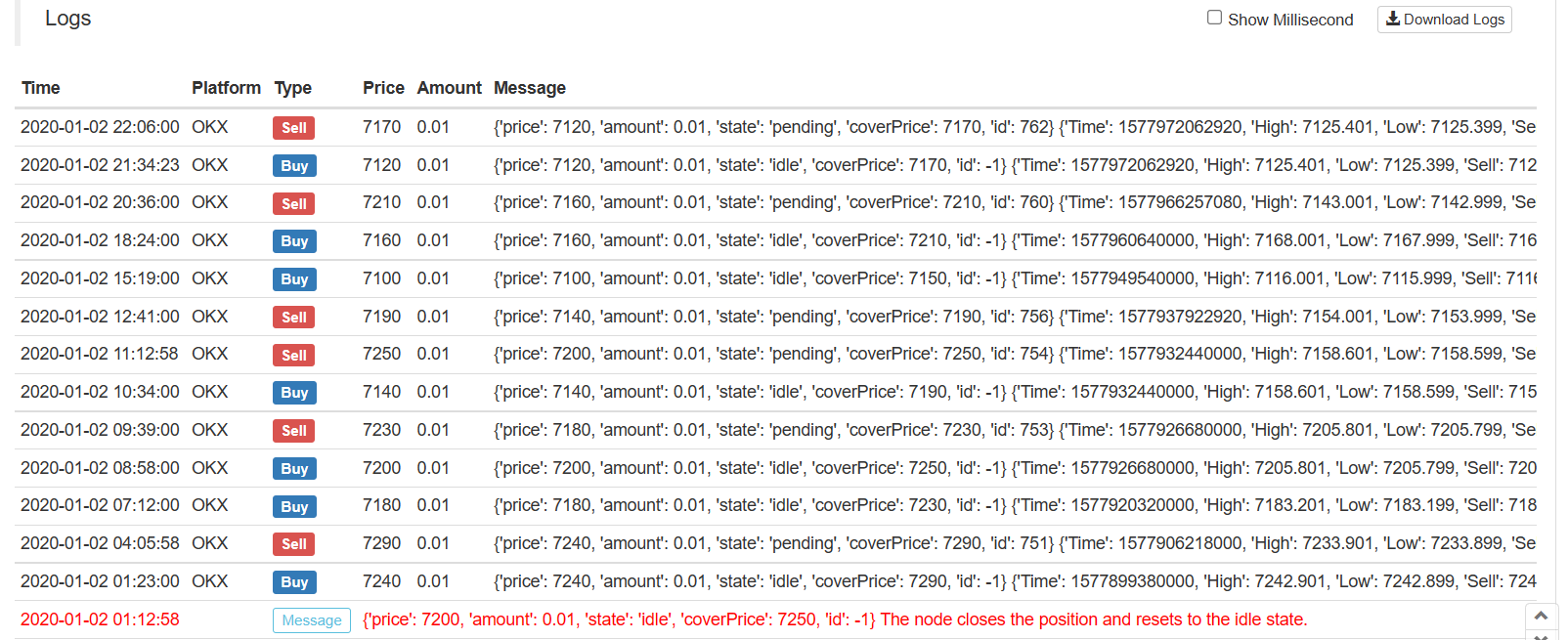

A principal ideia de conceção da estratégia consiste em comparar a lista actual de ordens pendentes devolvidas peloGetOrdersAnalise as alterações de ordens pendentes (se estão fechadas ou não), atualize a estrutura de dados da grade e faça operações subsequentes. Além disso, as ordens pendentes não serão canceladas até que a transação seja concluída, mesmo que o preço se desvie, porque o mercado de moeda digital muitas vezes tem a situação de pinos, essas ordens pendentes também podem receber as ordens de pinos (se o número de ordens pendentes for limitado na bolsa, ele será ajustado).

A visualização de dados de estratégia utiliza oLogStatusFunção para exibir dados na barra de estado em tempo real.

tbl = {

"type" : "table",

"title" : "grid status",

"cols" : ["node index", "details"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "record",

"cols" : ["node index", "details"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["node index", "details"],

"rows" : [],

}

Três tabelas são construídas. A primeira tabela exibe as informações de cada nó na estrutura de dados da grade atual, a segunda tabela exibe informações anormais e a terceira tabela exibe as informações reais de listagem da troca.

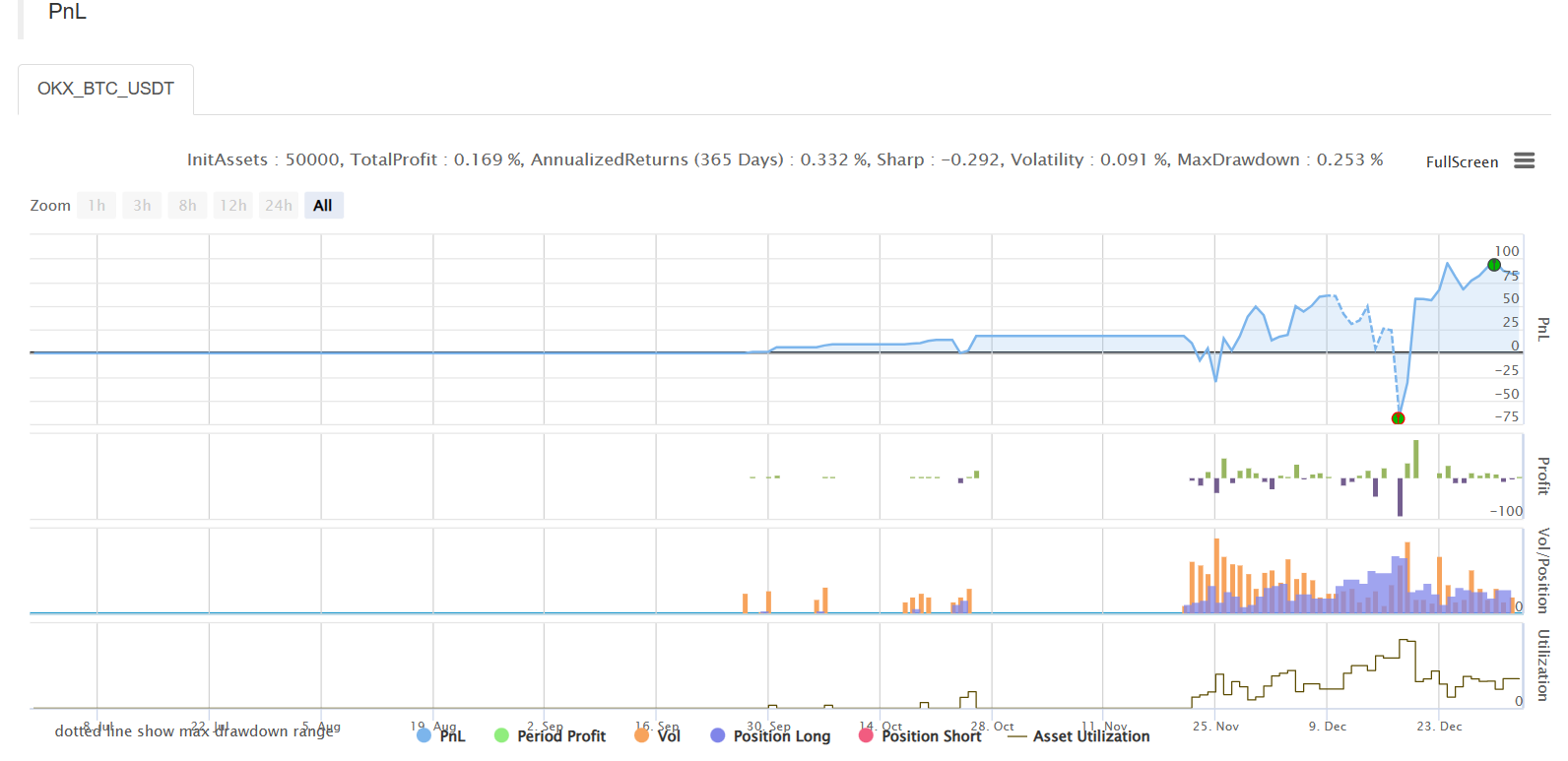

Teste de retrocesso

Endereço da estratégia

A estratégia é para aprendizagem e backtesting propósito apenas, e ele pode ser otimizado e atualizado se você estiver interessado.

- Quantificar a análise fundamental no mercado de criptomoedas: deixe os dados falarem por si mesmos!

- A pesquisa quantitativa básica do círculo monetário - deixe de acreditar em todos os professores de matemática loucos, os dados são objetivos!

- Uma ferramenta indispensável no campo da transação quantitativa - inventor do módulo de exploração de dados quantitativos

- Dominar tudo - Introdução ao FMZ Nova versão do Terminal de Negociação (com TRB Arbitrage Source Code)

- Conheça tudo sobre a nova versão do terminal de negociação da FMZ

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (II)

- Como explorar robôs de venda sem cérebro com uma estratégia de alta frequência em 80 linhas de código

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (II)

- Como usar estratégias de 80 linhas de código de alta frequência para explorar robôs sem cérebro para venda

- FMZ Quant: Análise de Exemplos de Design de Requisitos Comuns no Mercado de Criptomoedas (I)

- Quantificação FMZ: Análise de casos de design de necessidades comuns do mercado de criptomoedas (I)