Nghiên cứu về Binance Futures Multi-currency Hedging Strategy Phần 4

Tác giả:Tốt, Tạo: 2020-05-14 15:18:56, Cập nhật: 2023-11-04 19:51:33

Binance tương lai chiến lược phòng hộ đa tiền tệ

Ba báo cáo nghiên cứu về chiến lược phòng hộ đa tiền tệ của Binance đã được xuất bản, đây là báo cáo thứ tư.

Nghiên cứu về Binance Futures Chiến lược phòng hộ đa loại tiền tệ Phần 1:https://www.fmz.com/digest-topic/5584

Nghiên cứu về Binance Futures Chiến lược phòng hộ đa tiền tệ Phần 2:https://www.fmz.com/digest-topic/5588

Nghiên cứu về Binance Futures Chiến lược phòng hộ đa tiền tệ Phần 3:https://www.fmz.com/digest-topic/5605

Bài viết này là để xem xét tình hình thị trường thực tế trong tuần gần đây, và tóm tắt lợi nhuận và tổn thất. Kể từ khi thu thập dữ liệu đường K phút của Binance Futures trong hai tháng qua, kết quả backtest đường 1h K ban đầu có thể được cập nhật, có thể giải thích tốt hơn ý nghĩa của một số cài đặt tham số.

# Libraries to import

import pandas as pd

import requests

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

%matplotlib inline

symbols = ['BTC','ETH', 'BCH', 'XRP', 'EOS', 'LTC', 'TRX', 'ETC', 'LINK', 'XLM', 'ADA', 'XMR', 'DASH', 'ZEC', 'XTZ', 'BNB', 'ATOM', 'ONT', 'IOTA', 'BAT', 'VET', 'NEO', 'QTUM', 'IOST']

Dữ liệu dòng K cấp phút

Dữ liệu từ ngày 21 tháng 2 đến ngày 15 tháng 4 lúc 2 giờ chiều, tổng cộng 77160 * 24, làm giảm đáng kể tốc độ backtest của chúng tôi, công cụ backtest không đủ hiệu quả, bạn có thể tự tối ưu hóa nó.

price_usdt = pd.read_csv('https://www.fmz.com/upload/asset/2b1fa7ab641385067ad.csv',index_col = 0)

price_usdt.shape

(77160, 24)

price_usdt.index = pd.to_datetime(price_usdt.index,unit='ms')

price_usdt_norm = price_usdt/price_usdt.fillna(method='bfill').iloc[0,]

price_usdt_btc = price_usdt.divide(price_usdt['BTC'],axis=0)

price_usdt_btc_norm = price_usdt_btc/price_usdt_btc.fillna(method='bfill').iloc[0,]

class Exchange:

def __init__(self, trade_symbols, leverage=20, commission=0.00005, initial_balance=10000, log=False):

self.initial_balance = initial_balance # Initial asset

self.commission = commission

self.leverage = leverage

self.trade_symbols = trade_symbols

self.date = ''

self.log = log

self.df = pd.DataFrame(columns=['margin','total','leverage','realised_profit','unrealised_profit'])

self.account = {'USDT':{'realised_profit':0, 'margin':0, 'unrealised_profit':0, 'total':initial_balance, 'leverage':0, 'fee':0}}

for symbol in trade_symbols:

self.account[symbol] = {'amount':0, 'hold_price':0, 'value':0, 'price':0, 'realised_profit':0, 'margin':0, 'unrealised_profit':0,'fee':0}

def Trade(self, symbol, direction, price, amount, msg=''):

if self.date and self.log:

print('%-20s%-5s%-5s%-10.8s%-8.6s %s'%(str(self.date), symbol, 'buy' if direction == 1 else 'sell', price, amount, msg))

cover_amount = 0 if direction*self.account[symbol]['amount'] >=0 else min(abs(self.account[symbol]['amount']), amount)

open_amount = amount - cover_amount

self.account['USDT']['realised_profit'] -= price*amount*self.commission # Minus handling fee

self.account['USDT']['fee'] += price*amount*self.commission

self.account[symbol]['fee'] += price*amount*self.commission

if cover_amount > 0: # close position first

self.account['USDT']['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount # profit

self.account['USDT']['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage # Free margin

self.account[symbol]['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount

self.account[symbol]['amount'] -= -direction*cover_amount

self.account[symbol]['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage

self.account[symbol]['hold_price'] = 0 if self.account[symbol]['amount'] == 0 else self.account[symbol]['hold_price']

if open_amount > 0:

total_cost = self.account[symbol]['hold_price']*direction*self.account[symbol]['amount'] + price*open_amount

total_amount = direction*self.account[symbol]['amount']+open_amount

self.account['USDT']['margin'] += open_amount*price/self.leverage

self.account[symbol]['hold_price'] = total_cost/total_amount

self.account[symbol]['amount'] += direction*open_amount

self.account[symbol]['margin'] += open_amount*price/self.leverage

self.account[symbol]['unrealised_profit'] = (price - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = price

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*price

return True

def Buy(self, symbol, price, amount, msg=''):

self.Trade(symbol, 1, price, amount, msg)

def Sell(self, symbol, price, amount, msg=''):

self.Trade(symbol, -1, price, amount, msg)

def Update(self, date, close_price): # Update assets

self.date = date

self.close = close_price

self.account['USDT']['unrealised_profit'] = 0

for symbol in self.trade_symbols:

if np.isnan(close_price[symbol]):

continue

self.account[symbol]['unrealised_profit'] = (close_price[symbol] - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = close_price[symbol]

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*close_price[symbol]

self.account['USDT']['unrealised_profit'] += self.account[symbol]['unrealised_profit']

self.account['USDT']['total'] = round(self.account['USDT']['realised_profit'] + self.initial_balance + self.account['USDT']['unrealised_profit'],6)

self.account['USDT']['leverage'] = round(self.account['USDT']['margin']/self.account['USDT']['total'],4)*self.leverage

self.df.loc[self.date] = [self.account['USDT']['margin'],self.account['USDT']['total'],self.account['USDT']['leverage'],self.account['USDT']['realised_profit'],self.account['USDT']['unrealised_profit']]

Đánh giá tuần trước

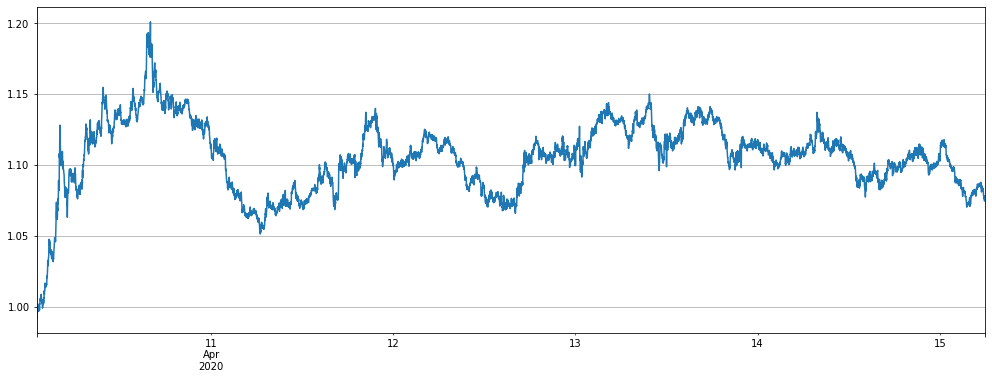

Mã chiến lược được phát hành trong nhóm WeChat vào ngày 10 tháng Tư. Ban đầu, một nhóm người chạy chiến lược 2 ((nâng cao quá ngắn và giảm quá dài). Trong ba ngày đầu tiên, lợi nhuận rất tốt, và sự thoái lui rất thấp. trong những ngày tiếp theo, một số nhà giao dịch đã phóng đại đòn bẩy, một số thậm chí sử dụng toàn bộ số tiền của họ để hoạt động, và lợi nhuận đạt 10% trong một ngày. Strategy Square cũng phát hành rất nhiều chiến lược thị trường thực tế, nhiều người bắt đầu không hài lòng với các thông số khuyến nghị bảo thủ, và đã khuếch đại khối lượng giao dịch. Sau ngày 13 tháng Tư, do xu hướng độc lập của BNB

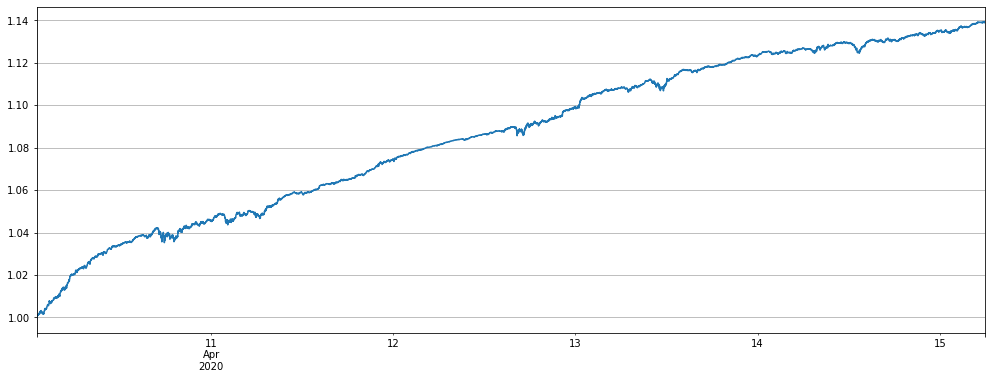

Chúng ta hãy xem xét toàn bộ tiền tệ backtest của Chiến lược 2. Ở đây, vì nó là một cập nhật cấp phút, các thông số Alpha cần phải được điều chỉnh. Từ một thị trường thực sự quan điểm, xu hướng đường cong là phù hợp, cho thấy rằng backtest của chúng tôi có thể được sử dụng như một tham chiếu mạnh mẽ. Giá trị ròng đã đạt đến đỉnh của giá trị ròng từ 4.13 trở đi và đã ở trong giai đoạn thu hồi và bên.

Alpha = 0.001

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 300

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 0.5*trade_value:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -0.5*trade_value:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2a = e

(stragey_2a.df['total']/stragey_2d.initial_balance).plot(figsize=(17,6),grid = True);

Chiến lược 1, chiến lược altcoin ngắn đạt được lợi nhuận tích cực

trade_symbols = list(set(symbols)-set(['LINK','BTC','XTZ','BCH', 'ETH'])) # Selling short currencies

e = Exchange(trade_symbols+['BTC'],initial_balance=10000,commission=0.00075,log=False)

trade_value = 2000

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

if e.account[symbol]['value'] - trade_value < -120 :

e.Sell(symbol, price, round((trade_value-e.account[symbol]['value'])/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if e.account[symbol]['value'] - trade_value > 120 :

e.Buy(symbol, price, round((e.account[symbol]['value']-trade_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

empty_value += e.account[symbol]['value']

price = row[1]['BTC']

if e.account['BTC']['value'] - empty_value < -120:

e.Buy('BTC', price, round((empty_value-e.account['BTC']['value'])/price,6),round(e.account['BTC']['realised_profit']+e.account['BTC']['unrealised_profit'],2))

if e.account['BTC']['value'] - empty_value > 120:

e.Sell('BTC', price, round((e.account['BTC']['value']-empty_value)/price,6),round(e.account['BTC']['realised_profit']+e.account['BTC']['unrealised_profit'],2))

stragey_1 = e

(stragey_1.df['total']/stragey_1.initial_balance).plot(figsize=(17,6),grid = True);

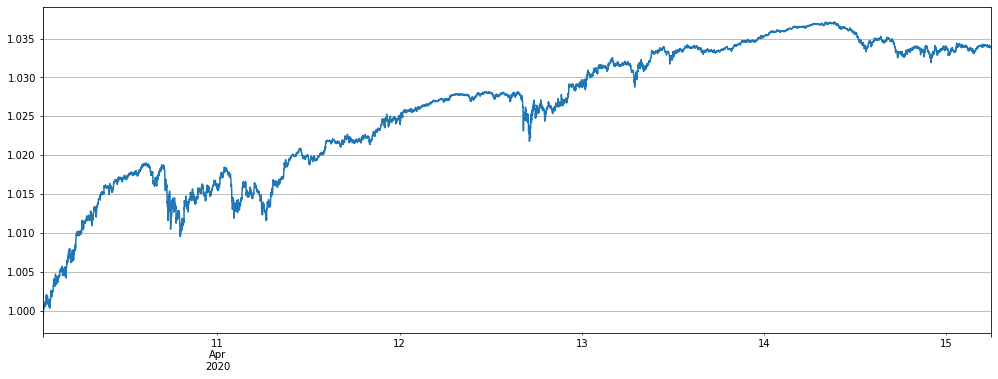

Chiến lược 2 mua quá mức giảm và bán quá mức tăng ngắn phân tích lợi nhuận

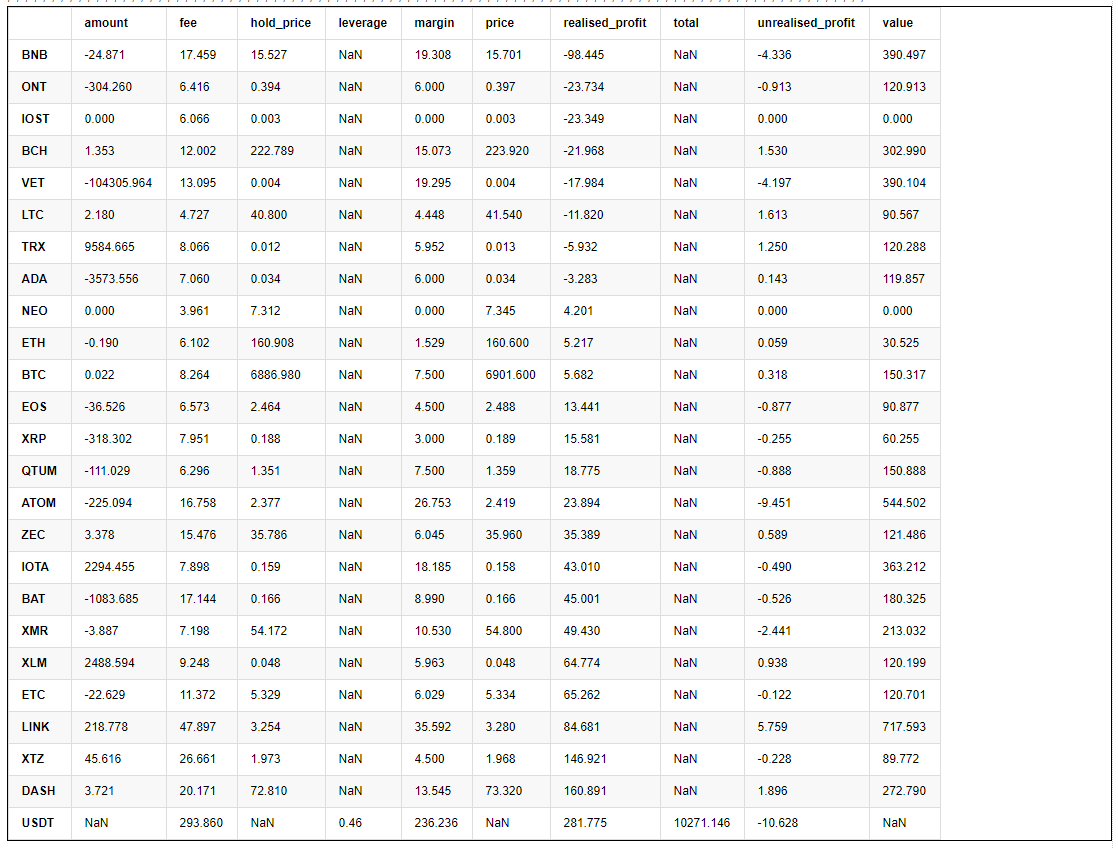

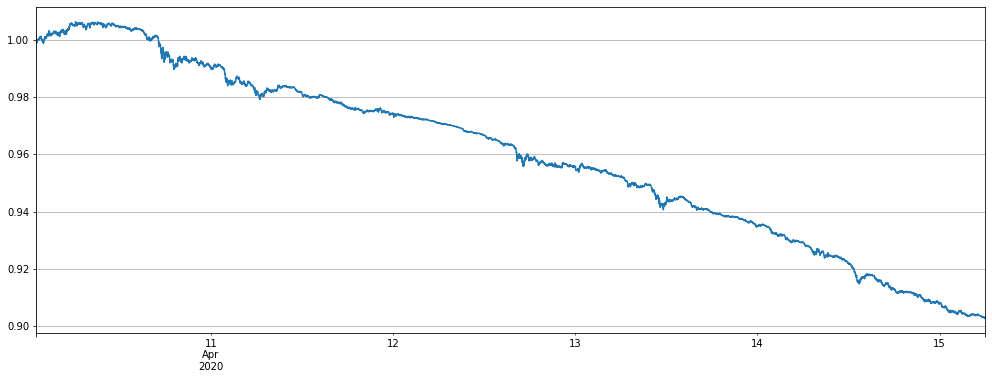

Việc in ra thông tin tài khoản cuối cùng cho thấy hầu hết các loại tiền tệ đều mang lại lợi nhuận, và BNB đã chịu thiệt hại nhiều nhất.

pd.DataFrame(stragey_2a.account).T.apply(lambda x:round(x,3)).sort_values(by='realised_profit')

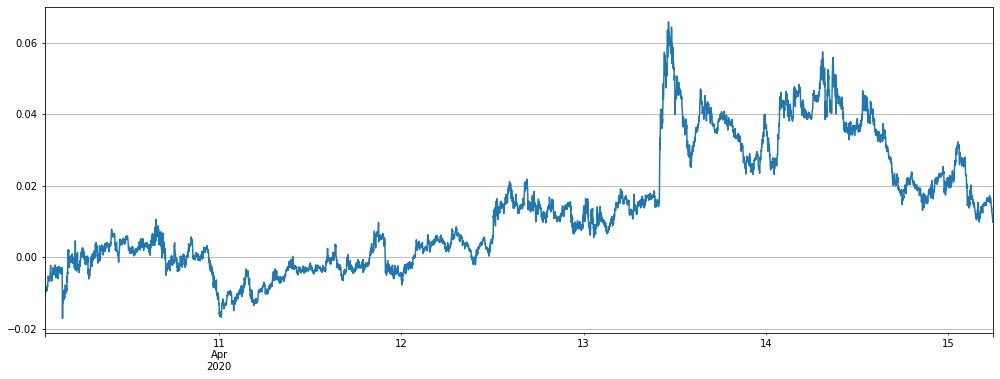

# BNB deviation

(price_usdt_btc_norm2.iloc[-7500:].BNB-price_usdt_btc_norm_mean[-7500:]).plot(figsize=(17,6),grid = True);

#price_usdt_btc_norm_mean[-7500:].plot(figsize=(17,6),grid = True);

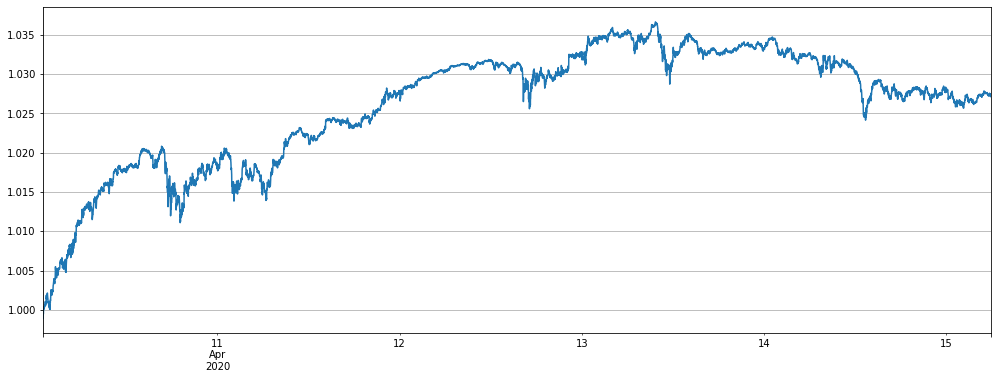

Nếu BNB và ATOM bị loại bỏ, kết quả sẽ tốt hơn, nhưng chiến lược sẽ vẫn ở giai đoạn khôi phục gần đây.

Alpha = 0.001

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols)-set(['BNB','ATOM']))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 300

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 0.5*trade_value:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -0.5*trade_value:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2b = e

(stragey_2b.df['total']/stragey_2b.initial_balance).plot(figsize=(17,6),grid = True);

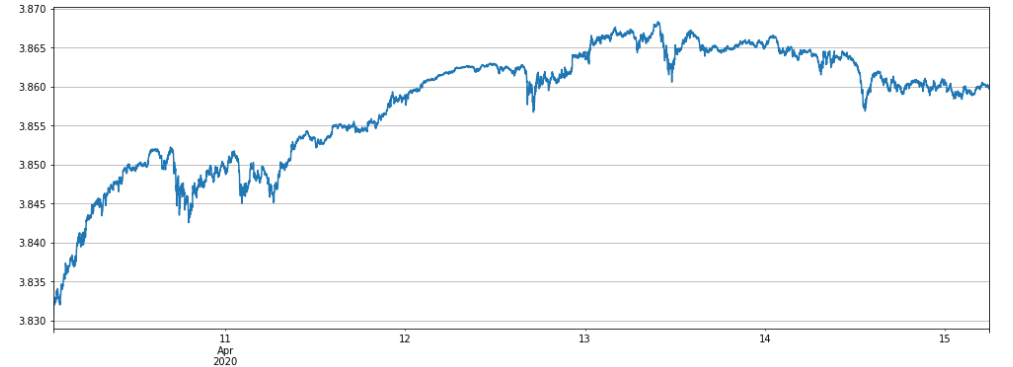

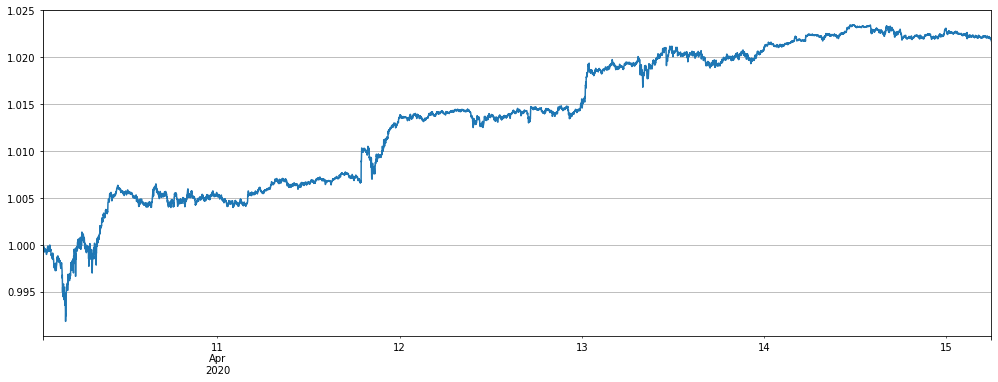

Trong hai ngày qua, nó đã trở nên phổ biến để chạy các chiến lược tiền tệ chính thống. Hãy kiểm tra lại chiến lược này. Do sự sụt giảm sự đa dạng tiền tệ, trade_value đã được tăng 4 lần để so sánh, và kết quả hoạt động tốt, đặc biệt là kể từ khi việc khôi phục gần đây là nhỏ.

Cần lưu ý rằng chỉ có đồng tiền chính không tốt như đồng tiền đầy đủ trong thời gian dài hơn, và có nhiều sự hồi phục. Bạn có thể làm backtest của riêng bạn trên đường hàng giờ bên dưới, chủ yếu là vì đồng tiền ít phân tán và biến động tăng thay vào đó.

Alpha = 0.001

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = ['ETH','LTC','EOS','XRP','BCH']

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 1200

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 0.5*trade_value:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -0.5*trade_value:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2c = e

(stragey_2c.df['total']/e.initial_balance).plot(figsize=(17,6),grid = True);

Phân tích các thông số về phí xử lý và chiến lược

Vì vài báo cáo đầu tiên sử dụng đường k cấp giờ, và các tham số thực tế rất khác với tình hình thị trường thực tế, bây giờ với đường k cấp phút, bạn có thể xem cách thiết lập một số tham số.

-

Alpha = 0.03 Các tham số Alpha của đường trung bình động theo cấp số nhân. Càng lớn thiết lập, càng nhạy cảm theo dõi giá chuẩn và ít giao dịch hơn. Vị trí nắm giữ cuối cùng cũng sẽ thấp hơn, làm giảm đòn bẩy, nhưng cũng sẽ làm giảm lợi nhuận và khôi phục tối đa.

-

Update_base_price_time_interval = 30 * 60 Bao nhiêu lần để cập nhật giá cơ sở, trong giây, liên quan đến tham số Alpha, nhỏ hơn cài đặt Alpha, nhỏ hơn khoảng thời gian có thể được đặt

-

Trade_value: Mỗi 1% giá altcoin (được mệnh giá bằng BTC) lệch so với giá trị nắm giữ chỉ số, cần được xác định theo tổng số tiền đầu tư và ưu tiên rủi ro. Bạn có thể xem xét kích thước đòn bẩy thông qua kiểm tra hậu trường của môi trường nghiên cứu. Trade_value có thể nhỏ hơn Adjust_value, chẳng hạn như một nửa giá trị Adjust_value, tương đương với giá trị nắm giữ 2% từ chỉ số.

-

Adjust_value: Giá trị hợp đồng (giá trị USDT) điều chỉnh giá trị lệch. Khi chỉ số lệch từ * Trade_value-current position> Adjust_value, nghĩa là sự khác biệt giữa vị trí mục tiêu và vị trí hiện tại vượt quá giá trị này, giao dịch sẽ bắt đầu. Sự điều chỉnh quá lớn chậm, giao dịch quá nhỏ thường xuyên và không thể dưới 10, nếu không thì giao dịch tối thiểu sẽ không đạt được, nên đặt nó lên hơn 40% giá trị Trade_value.

Không cần phải nói, Trade_value có liên quan trực tiếp đến lợi nhuận và rủi ro của chúng tôi.

Vì Alpha có dữ liệu tần số cao hơn lần này, rõ ràng là hợp lý hơn để cập nhật nó mỗi 1 phút.

Adjust_value luôn được đề nghị trên 40% của Trade_value. Cài đặt đường 1h K ban đầu có ít hiệu quả. Một số người muốn điều chỉnh nó rất thấp, để nó có thể gần hơn với vị trí mục tiêu. Ở đây chúng tôi sẽ phân tích lý do tại sao không nên làm như vậy.

Đầu tiên phân tích vấn đề xử lý phí

Có thể thấy rằng dưới tỷ lệ mặc định là 0,00075, phí xử lý là 293 và lợi nhuận là 270, đó là một tỷ lệ rất cao.

stragey_2a.account['USDT']

{'fee': 293.85972778530453,

'leverage': 0.45999999999999996,

'margin': 236.23559736312995,

'realised_profit': 281.77464608744435,

'total': 10271.146238,

'unrealised_profit': -10.628408369648495}

Alpha = 0.001

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0,log=False)

trade_value = 300

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 10:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < 10:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2d = e

(stragey_2d.df['total']/e.initial_balance).plot(figsize=(17,6),grid = True);

Kết quả là một đường thẳng lên, BNB chỉ mang lại một chút xoắn và xoắn, giá trị điều chỉnh thấp hơn nắm bắt mọi biến động.

Điều gì sẽ xảy ra nếu giá trị điều chỉnh là nhỏ nếu có một khoản phí xử lý nhỏ?

Alpha = 0.001

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 300

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 10:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < 10:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2e = e

(stragey_2e.df['total']/e.initial_balance).plot(figsize=(17,6),grid = True);

Kết quả là, nó cũng ra khỏi đường cong thẳng xuống. nó dễ hiểu nếu bạn nghĩ về nó, điều chỉnh thường xuyên trong một chênh lệch nhỏ sẽ chỉ mất phí xử lý.

Nhìn chung, mức phí càng thấp, giá trị Adjust_value càng nhỏ, giao dịch càng thường xuyên và lợi nhuận càng cao.

Vấn đề với cài đặt Alpha

Vì có một dòng phút, giá chuẩn sẽ được cập nhật một lần mỗi phút, ở đây chúng tôi chỉ đơn giản là backtest để xác định kích thước của alpha.

for Alpha in [0.0001, 0.0003, 0.0006, 0.001, 0.0015, 0.002, 0.004, 0.01, 0.02]:

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() #Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 300

for row in price_usdt.iloc[-7500:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 0.5*trade_value:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -0.5*trade_value:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

print(Alpha, e.account['USDT']['unrealised_profit']+e.account['USDT']['realised_profit'])

0.0001 -77.80281760941007

0.0003 179.38803796199724

0.0006 218.12579924541367

0.001 271.1462377177959

0.0015 250.0014065973528

0.002 207.38692166891275

0.004 129.08021828803027

0.01 65.12410041648158

0.02 58.62356792410955

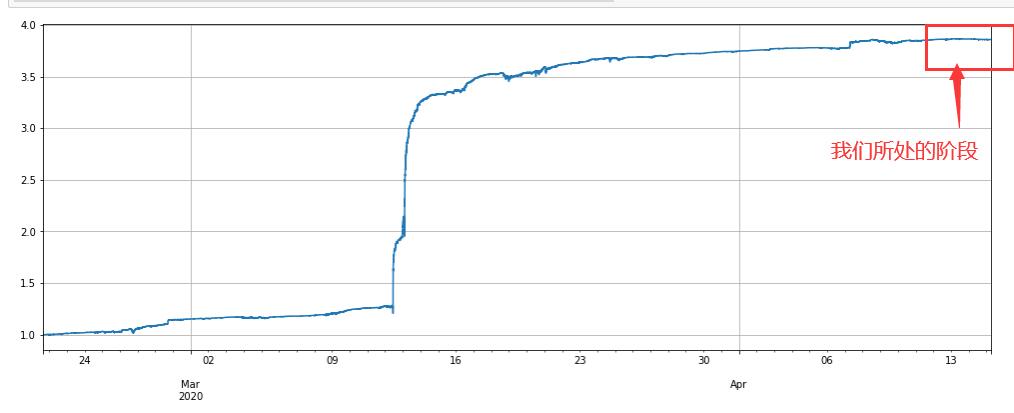

Kết quả kiểm tra ngược của đường phút trong hai tháng qua

Cuối cùng, hãy nhìn vào kết quả của một backtest thời gian dài. Ngay bây giờ, một sau một tăng, và giá trị ròng ngày hôm nay ở mức thấp mới. Hãy cho bạn sự tự tin sau đây. Bởi vì tần suất của dòng phút cao hơn, nó sẽ mở và đóng các vị trí trong vòng một giờ, vì vậy lợi nhuận sẽ cao hơn nhiều.

Một điểm khác, chúng tôi luôn luôn sử dụng một trade_value cố định, làm cho việc sử dụng các quỹ trong thời gian sau đó là không đủ, và tỷ lệ lợi nhuận thực tế vẫn có thể tăng rất nhiều.

Chúng ta đang ở đâu trong thời gian kiểm tra hai tháng?

Alpha = 0.001

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.00075,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

if aim_value - now_value > 0.5*trade_value:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -0.5*trade_value:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2f = e

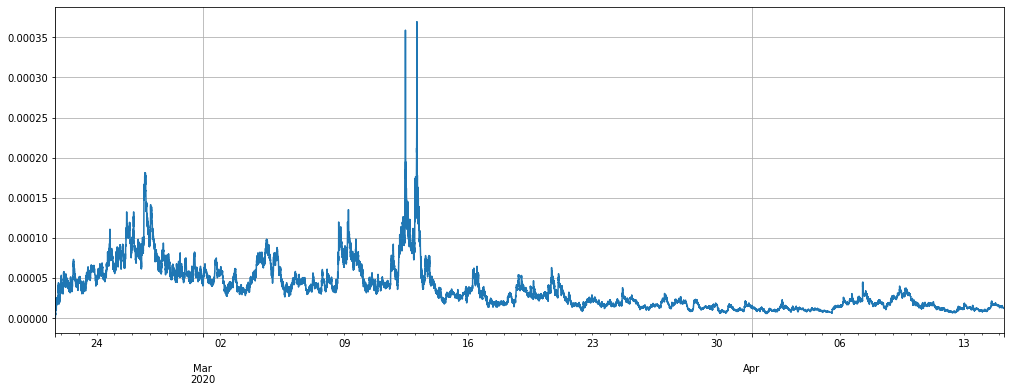

(stragey_2f.df['total']/stragey_2e.initial_balance).plot(figsize=(17,6),grid = True);

(stragey_2f.df['leverage']/stragey_2e.initial_balance).plot(figsize=(17,6),grid = True);

- Xác định số lượng phân tích cơ bản trong thị trường tiền điện tử: Hãy để dữ liệu nói cho chính nó!

- Các nghiên cứu định lượng cơ bản của vòng đồng tiền - đừng tin vào những giáo viên mờ nhạt, nói khách quan về dữ liệu!

- Một công cụ thiết yếu trong lĩnh vực giao dịch định lượng - nhà phát minh mô-đun khám phá dữ liệu định lượng

- Kiểm soát mọi thứ - giới thiệu về FMZ Phiên bản mới của Terminal giao dịch (với mã nguồn TRB Arbitrage)

- Có tất cả các thông tin về FMZ phiên bản mới của giao dịch đầu cuối (được thêm mã nguồn TRB)

- FMZ Quant: Phân tích các ví dụ thiết kế yêu cầu chung trong thị trường tiền điện tử (II)

- Làm thế nào để khai thác robot bán hàng không có não với một chiến lược tần số cao trong 80 dòng mã

- FMZ định lượng: Phân tích các trường hợp thiết kế nhu cầu phổ biến của thị trường tiền điện tử (II)

- Cách khai thác robot vô trí tuệ để bán bằng chiến lược tần số cao 80 dòng mã

- FMZ Quant: Phân tích các ví dụ thiết kế yêu cầu chung trong thị trường tiền điện tử (I)

- FMZ định lượng: Các nhu cầu phổ biến của thị trường tiền điện tử