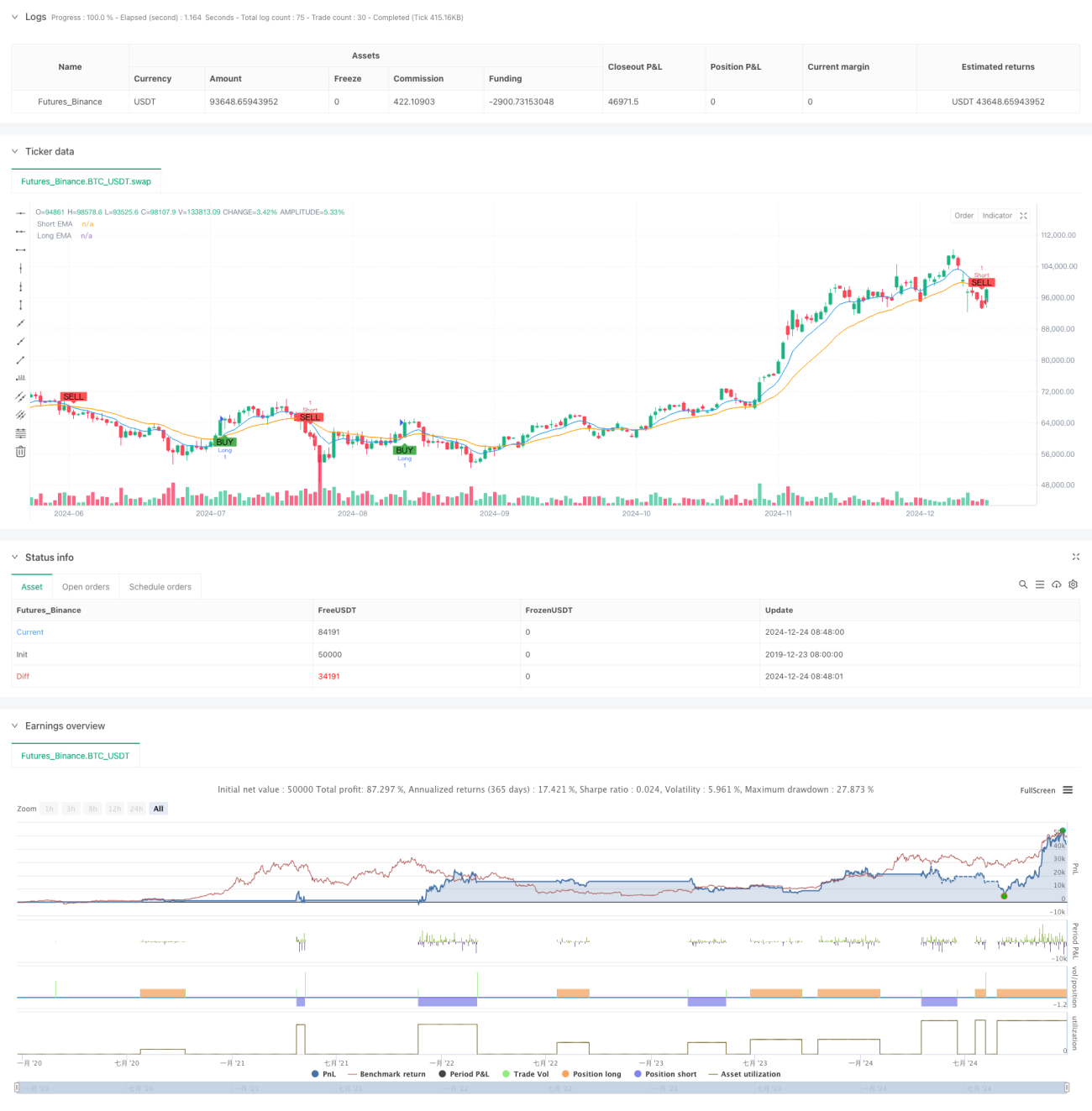

Overview

This is a high-frequency range trading strategy based on multiple technical indicators. The strategy combines signals from Exponential Moving Average (EMA), Relative Strength Index (RSI), volume analysis, and N-period price pattern recognition to identify optimal entry points in short-term trading. It implements strict risk management through predefined take-profit and stop-loss levels.

Strategy Principle

The core logic relies on multi-dimensional signal confirmation:

- Uses 8-period and 21-period EMA crossovers to determine short-term trend direction

- Validates market momentum using 14-period RSI, with RSI>50 confirming bullish momentum and RSI<50 confirming bearish momentum

- Compares current volume with 20-period average volume to ensure market activity

- Identifies potential reversal patterns by comparing the last 5 candles with the previous 10 candles

Trading signals are generated only when all conditions align. Long positions are opened at market price for bullish signals, and short positions for bearish signals. Risk is controlled through 1.5% take-profit and 0.7% stop-loss levels.

Strategy Advantages

- Multi-dimensional signal cross-validation significantly reduces false signals

- Combines benefits of trend-following and momentum trading for improved adaptability

- Volume confirmation prevents trading during illiquid periods

- N-period pattern recognition enables timely detection of market reversals

- Reasonable profit/loss ratios for effective risk control

- Clear logic facilitates continuous optimization and parameter adjustment

Strategy Risks

- Frequent stop-losses may occur in highly volatile markets

- Sensitive to market maker quote delays

- Relatively few opportunities when all indicators align

- Consecutive losses possible in ranging markets

Mitigation measures:

- Dynamically adjust profit/loss ratios based on market volatility

- Trade during periods of high liquidity

- Optimize parameters to balance signal quantity and quality

- Implement trailing stops to improve profitability

Optimization Directions

- Introduce adaptive parameter adjustment mechanisms for automatic optimization based on market conditions

- Add volatility filters to pause trading in excessive volatility

- Develop more sophisticated N-period pattern recognition algorithms

- Implement position sizing based on account equity

- Add multiple timeframe confirmation for increased signal reliability

Summary

The strategy identifies quality trading opportunities in high-frequency trading through multi-dimensional technical indicator collaboration. It considers trend, momentum, and volume characteristics while ensuring stability through strict risk control. While there is room for optimization, it represents a logically sound and practical trading approach.

- 1