Es el asesino de los BTC.

El autor:¿ Qué pasa?, Fecha: 2022-05-17 11:23:58Las etiquetas:La SMAEl ATRADX

¡ Hola!

Hice una buena estrategia con una ganancia increíble con solo órdenes largas y cortas Bueno, esta estrategia es para ------->>> BINANCE:BTCUSDT

La lógica de la estrategia es bastante simple.

Estrategia que utiliza 3 SMA diferentes (7,21,55) para encontrar una tendencia correcta Para evitar muchas señales erróneas añadí dos indicadores como:

ADX - Es uno de los indicadores de tendencia más poderosos y precisos. ADX mide cuán fuerte es una tendencia y puede dar información valiosa sobre si hay una oportunidad comercial potencial. CLOUD - Este es uno de los indicadores que estoy usando. Este indicador ayuda a la estrategia, este indicador está diseñado para indicar la tendencia correcta del mercado. Al aplicar la gran longitud de este indicador, puedo notar un cambio en la tendencia un poco más tarde, pero con mayor precisión.

Adicionalmente añadí el stop-loss de seguimiento a la máxima seguridad

Para ser honesto esta estrategia se ve muy bien, un montón de operaciones, alta ganancia y una pequeña cantidad de indicadores, las ganancias futuras podrían ser similares

Usando esta combinación de SMA me da cambios rápidos increíbles mientras que la tendencia también está cambiando rápido como aquí:

instantáneo

Desafortunadamente no pude eliminar el 100% de señales erróneas en el gráfico plano como aquí:

instantáneo

Espero que esta estrategia sea útil para cualquiera ;)

El culo siempre

¡ Disfruta!

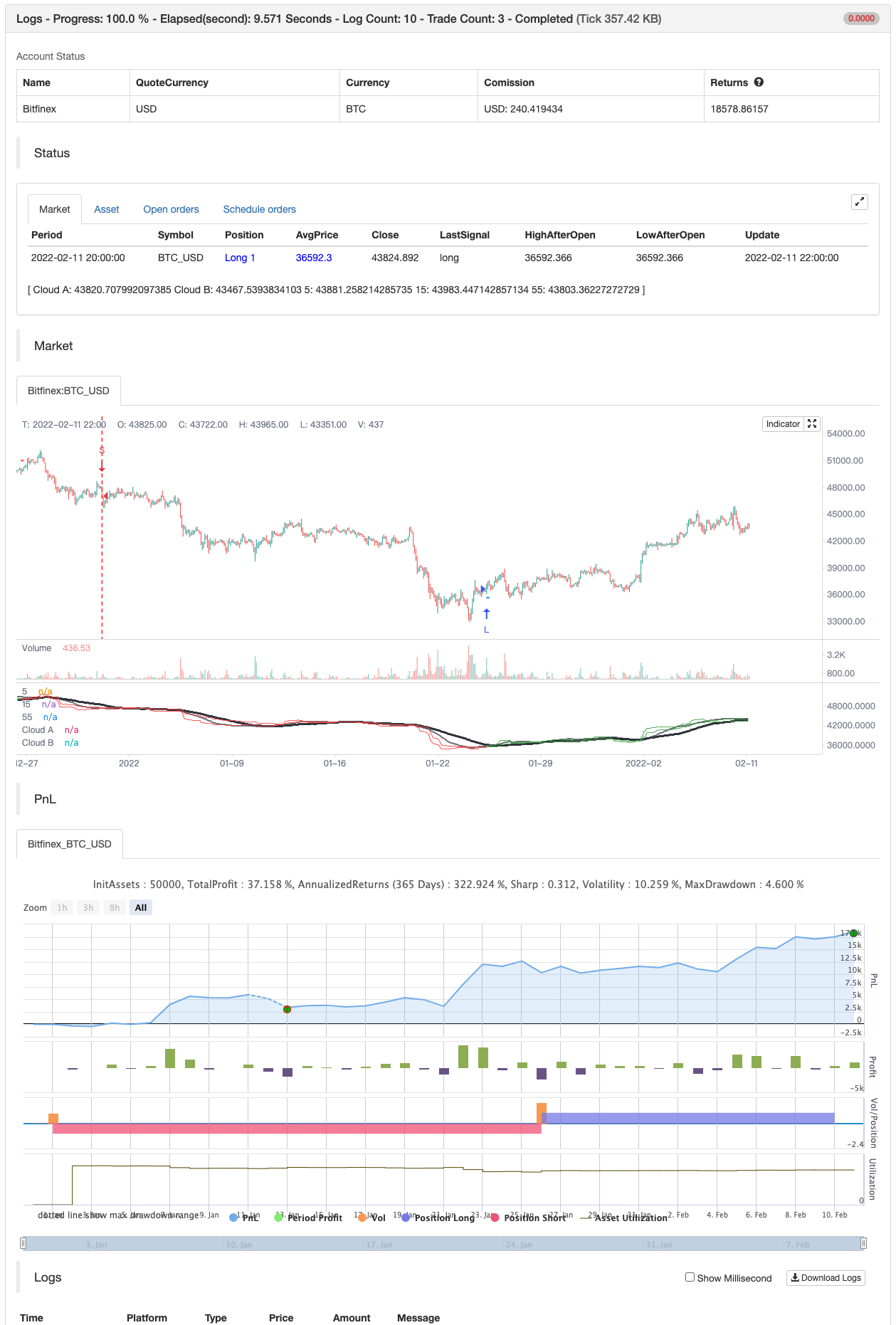

Prueba posterior

/*backtest

start: 2022-01-01 00:00:00

end: 2022-02-11 23:59:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Bitfinex","currency":"BTC_USD"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © wielkieef

//@version=4

src = close

//strategy("Sma BTC killer [60MIN]", overlay = true, pyramiding=1,initial_capital = 10000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.04)

//SMAs -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Length1 = input(14, title=" 1-SMA Lenght", minval=1)

Length2 = input(28, title=" 2-SMA Lenght", minval=1)

Length3 = input(55, title=" 3-SMA Lenght", minval=1)

xPrice = close

SMA1 = sma(xPrice, Length1)

SMA2 = sma(xPrice, Length2)

SMA3 = sma(xPrice, Length3)

//Indicators Inputs -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

ADX_options = input("MASANAKAMURA", title=" Adx Type", options = ["CLASSIC", "MASANAKAMURA"], group="Average Directional Index")

ADX_len = input(29, title=" Adx Lenght", type=input.integer, minval = 1, group="Average Directional Index")

th = input(21, title=" Adx Treshold", type=input.integer, minval = 0, group="Average Directional Index")

len = input(11, title="Cloud Length", group="Cloud")

// ATR Inputs -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

prd = input(18, title=" PP period", group="Average True Range")

Factor = input(5, title=" ATR Factor", group="Average True Range")

Pd = input(6, title=" ATR Period", group="Average True Range")

//Indicators -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

calcADX(_len) =>

up = change(high)

down = -change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

truerange = rma(tr, _len)

_plus = fixnan(100 * rma(plusDM, _len) / truerange)

_minus = fixnan(100 * rma(minusDM, _len) / truerange)

sum = _plus + _minus

_adx = 100 * rma(abs(_plus - _minus) / (sum == 0 ? 1 : sum), _len)

[_plus,_minus,_adx]

calcADX_Masanakamura(_len) =>

SmoothedTrueRange = 0.0

SmoothedDirectionalMovementPlus = 0.0

SmoothedDirectionalMovementMinus = 0.0

TrueRange = max(max(high - low, abs(high - nz(close[1]))), abs(low - nz(close[1])))

DirectionalMovementPlus = high - nz(high[1]) > nz(low[1]) - low ? max(high - nz(high[1]), 0) : 0

DirectionalMovementMinus = nz(low[1]) - low > high - nz(high[1]) ? max(nz(low[1]) - low, 0) : 0

SmoothedTrueRange := nz(SmoothedTrueRange[1]) - (nz(SmoothedTrueRange[1]) /_len) + TrueRange

SmoothedDirectionalMovementPlus := nz(SmoothedDirectionalMovementPlus[1]) - (nz(SmoothedDirectionalMovementPlus[1]) / _len) + DirectionalMovementPlus

SmoothedDirectionalMovementMinus := nz(SmoothedDirectionalMovementMinus[1]) - (nz(SmoothedDirectionalMovementMinus[1]) / _len) + DirectionalMovementMinus

DIP = SmoothedDirectionalMovementPlus / SmoothedTrueRange * 100

DIM = SmoothedDirectionalMovementMinus / SmoothedTrueRange * 100

DX = abs(DIP-DIM) / (DIP+DIM)*100

adx = sma(DX, _len)

[DIP,DIM,adx]

[DIPlusC,DIMinusC,ADXC] = calcADX(ADX_len)

[DIPlusM,DIMinusM,ADXM] = calcADX_Masanakamura(ADX_len)

DIPlus = ADX_options == "CLASSIC" ? DIPlusC : DIPlusM

DIMinus = ADX_options == "CLASSIC" ? DIMinusC : DIMinusM

ADX = ADX_options == "CLASSIC" ? ADXC : ADXM

L_adx = DIPlus > DIMinus and ADX > th

S_adx = DIPlus < DIMinus and ADX > th

ADX_COLOR = L_adx ? color.lime : S_adx ? color.red : color.orange

PI = 2 * asin(1)

hilbertTransform(src) =>

0.0962 * src + 0.5769 * nz(src[2]) - 0.5769 * nz(src[4]) - 0.0962 * nz(src[6])

computeComponent(src, mesaPeriodMult) =>

hilbertTransform(src) * mesaPeriodMult

computeAlpha(src, fastLimit, slowLimit) =>

mesaPeriod = 0.0

mesaPeriodMult = 0.075 * nz(mesaPeriod[1]) + 0.54

smooth = 0.0

smooth := (4 * src + 3 * nz(src[1]) + 2 * nz(src[2]) + nz(src[3])) / 10

detrender = 0.0

detrender := computeComponent(smooth, mesaPeriodMult)

I1 = nz(detrender[3])

Q1 = computeComponent(detrender, mesaPeriodMult)

jI = computeComponent(I1, mesaPeriodMult)

jQ = computeComponent(Q1, mesaPeriodMult)

I2 = 0.0

Q2 = 0.0

I2 := I1 - jQ

Q2 := Q1 + jI

I2 := 0.2 * I2 + 0.8 * nz(I2[1])

Q2 := 0.2 * Q2 + 0.8 * nz(Q2[1])

Re = I2 * nz(I2[1]) + Q2 * nz(Q2[1])

Im = I2 * nz(Q2[1]) - Q2 * nz(I2[1])

Re := 0.2 * Re + 0.8 * nz(Re[1])

Im := 0.2 * Im + 0.8 * nz(Im[1])

if Re != 0 and Im != 0

mesaPeriod := 2 * PI / atan(Im / Re)

if mesaPeriod > 1.5 * nz(mesaPeriod[1])

mesaPeriod := 1.5 * nz(mesaPeriod[1])

if mesaPeriod < 0.67 * nz(mesaPeriod[1])

mesaPeriod := 0.67 * nz(mesaPeriod[1])

if mesaPeriod < 6

mesaPeriod := 6

if mesaPeriod > 50

mesaPeriod := 50

mesaPeriod := 0.2 * mesaPeriod + 0.8 * nz(mesaPeriod[1])

phase = 0.0

if I1 != 0

phase := (180 / PI) * atan(Q1 / I1)

deltaPhase = nz(phase[1]) - phase

if deltaPhase < 1

deltaPhase := 1

alpha = fastLimit / deltaPhase

if alpha < slowLimit

alpha := slowLimit

[alpha,alpha/2.0]

er = abs(change(src,len)) / sum(abs(change(src)),len)

[a,b] = computeAlpha(src, er, er*0.1)

mama = 0.0

mama := a * src + (1 - a) * nz(mama[1])

fama = 0.0

fama := b * mama + (1 - b) * nz(fama[1])

alpha = pow((er * (b - a)) + a, 2)

kama = 0.0

kama := alpha * src + (1 - alpha) * nz(kama[1])

L_cloud = kama > kama[1]

S_cloud = kama < kama[1]

float ph = pivothigh(prd, prd)

float pl = pivotlow(prd, prd)

var float center = na

float lastpp = ph ? ph : pl ? pl : na

if lastpp

if na(center)

center := lastpp

else

center := (center * 2 + lastpp) / 3

Up = center - (Factor * atr(Pd))

Dn = center + (Factor * atr(Pd))

float TUp = na

float TDown = na

Trend = 0

TUp := close[1] > TUp[1] ? max(Up, TUp[1]) : Up

TDown := close[1] < TDown[1] ? min(Dn, TDown[1]) : Dn

Trend := close > TDown[1] ? 1: close < TUp[1]? -1: nz(Trend[1], 1)

Trailingsl = Trend == 1 ? TUp : TDown

bsignal = Trend == 1 and Trend[1] == -1

ssignal = Trend == -1 and Trend[1] == 1

L_ATR = Trend == 1

S_ATR = Trend == -1

// Strategy logic ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

var bool longCond = na, var bool shortCond = na

var int CondIni_long = 0, var int CondIni_short = 0

var bool _Final_longCondition = na, var bool _Final_shortCondition = na

var float last_open_longCondition = na, var float last_open_shortCondition = na

var int last_longCondition = na, var int last_shortCondition = na

var int last_Final_longCondition = na, var int last_Final_shortCondition = na

var int nLongs = na, var int nShorts = na

Long_MA =L_adx and L_cloud and (SMA1 < close and SMA2 < close and SMA3 < close )

Short_MA =S_adx and S_cloud and (SMA1 > close and SMA2 > close and SMA3 > close )

longCond := Long_MA

shortCond := Short_MA

CondIni_long := longCond[1] ? 1 : shortCond[1] ? -1 : nz(CondIni_long[1] )

CondIni_short := longCond[1] ? 1 : shortCond[1] ? -1 : nz(CondIni_short[1] )

longCondition = (longCond[1] and nz(CondIni_long[1]) == -1 )

shortCondition = (shortCond[1] and nz(CondIni_short[1]) == 1 )

var float sum_long = 0.0, var float sum_short = 0.0

var float Position_Price = 0.0

var bool Final_long_BB = na, var bool Final_short_BB = na

var int last_long_BB = na, var int last_short_BB = na

last_open_longCondition := longCondition or Final_long_BB[1] ? close[1] : nz(last_open_longCondition[1] )

last_open_shortCondition := shortCondition or Final_short_BB[1] ? close[1] : nz(last_open_shortCondition[1] )

last_longCondition := longCondition or Final_long_BB[1] ? time : nz(last_longCondition[1] )

last_shortCondition := shortCondition or Final_short_BB[1] ? time : nz(last_shortCondition[1] )

in_longCondition = last_longCondition > last_shortCondition

in_shortCondition = last_shortCondition > last_longCondition

last_Final_longCondition := longCondition ? time : nz(last_Final_longCondition[1] )

last_Final_shortCondition := shortCondition ? time : nz(last_Final_shortCondition[1] )

nLongs := nz(nLongs[1] )

nShorts := nz(nShorts[1] )

if longCondition or Final_long_BB

nLongs := nLongs + 1

nShorts := 0

sum_long := nz(last_open_longCondition) + nz(sum_long[1])

sum_short := 0.0

if shortCondition or Final_short_BB

nLongs := 0

nShorts := nShorts + 1

sum_short := nz(last_open_shortCondition)+ nz(sum_short[1])

sum_long := 0.0

Position_Price := nz(Position_Price[1])

Position_Price := longCondition or Final_long_BB ? sum_long/nLongs : shortCondition or Final_short_BB ? sum_short/nShorts : na

ATR_L_STOP = ssignal and in_longCondition

ATR_S_STOP = bsignal and in_shortCondition

// Plots and colors 010101010101010010101010101010101010101001010101010101001010101001010100101100111100101010010100110110010011100101010101010010101010101001011110011010101010101001010100101100110101010001001010101001010101001110110010101010100101010101010100111110101010101010101010100101010101100

colors = (in_longCondition ? color.green : in_shortCondition ? color.red : color.orange)

bgcolor(color=colors)

//barcolor (color = colors)

plotshape(longCondition, title="Long", style=shape.triangleup, location=location.belowbar, color=color.blue, size=size.small , transp = 0 )

plotshape(shortCondition, title="Short", style=shape.triangledown, location=location.abovebar, color=color.red, size=size.small , transp = 0 )

mama_p = plot(mama, title="Cloud A", style= plot.style_stepline, color=colors )

fama_p = plot(fama, title="Cloud B", style= plot.style_stepline, color=colors )

fill (mama_p,fama_p, color=colors )

plot(SMA1, color=color.white,style= plot.style_stepline, title="5", linewidth=1)

plot(SMA2, color=color.gray,style= plot.style_stepline, title="15", linewidth=2)

plot(SMA3, color=color.black,style= plot.style_stepline, title="55", linewidth=3)

plotshape(ATR_L_STOP, title = "ATR LONG CLOSE", style=shape.arrowdown, location=location.abovebar, color=color.red, size=size.small , text="ATR LONG CLOSE", textcolor=color.red, transp = 0 )

plotshape(ATR_S_STOP, title = "ATR SHORT CLOSE", style=shape.arrowup, location=location.belowbar, color=color.blue, size=size.small, text="ATR SHORT CLOSE", textcolor=color.blue, transp = 0 )

// Strategy -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

if Long_MA

strategy.entry ("L", strategy.long)

if Short_MA

strategy.entry ("S", strategy.short)

strategy.close_all( when = ATR_L_STOP or ATR_S_STOP)

// By wielkieef

- Obtener su tendencia

- Estrategia dinámica de DCA basada en el volumen

- Teoría de las ondas de Elliott 4-9 Detección automática de ondas de impulso Estrategia de negociación

- Bienvenido al mercado de osos.

- Estrategia de negociación de volatilidad escalable durante el día

- Supertrend+4 en movimiento

- La tendencia alfa

- Indicador de línea de seguimiento

- Concepto SuperTendencia Doble

- Comercio de tendencias en tiempo real basado en puntos de pivote y pendiente

- El RISOTTO

- Estrategia intradiaria de la nube de la EMA

- Supertendencia del punto de pivote

- Supertrend+4 en movimiento

- ZigZag basado en el impulso

- VuManChu Cifrado B + Divergencias Estrategia

- Concepto SuperTendencia Doble

- El Super Scalper

- Pruebas de retroceso - Indicador

- Tendencia

- Modelo de alertas de ML

- La progresión de Fibonacci con brechas

- Las operaciones de las entidades de crédito se clasifican en el modelo de referencia.

- Fukuiz Octa-EMA + Ichimoku

- Las entidades de crédito de las entidades de crédito incluidas en el cuadro 1 deberán tener en cuenta los siguientes elementos:

- MACD más inteligente

- Estrategia R5.1 del OCC

- Bienvenido al mercado de osos.

- Jefe del lado

- Puntos de eje Alto Bajo Marco de tiempo Multi