Estocástico + RSI, doble estrategia

El autor:¿ Qué pasa?, Fecha: 2022-05-25 16:12:14Las etiquetas:STOCHIndicador de riesgo

Esta estrategia combina la estrategia clásica de RSI para vender cuando el RSI supera los 70 (o para comprar cuando cae por debajo de 30), con la estrategia clásica de Stochastic Slow para vender cuando el oscilador estocástico supera el valor de 80 (y para comprar cuando este valor es inferior a 20).

Esta estrategia simple solo se activa cuando tanto el RSI como el Estocástico están juntos en una condición de sobrecompra o sobreventa.

Por cierto, esta estrategia no debe confundirse con el

Todas las operaciones implican un alto riesgo; el rendimiento pasado no es necesariamente indicativo de resultados futuros.

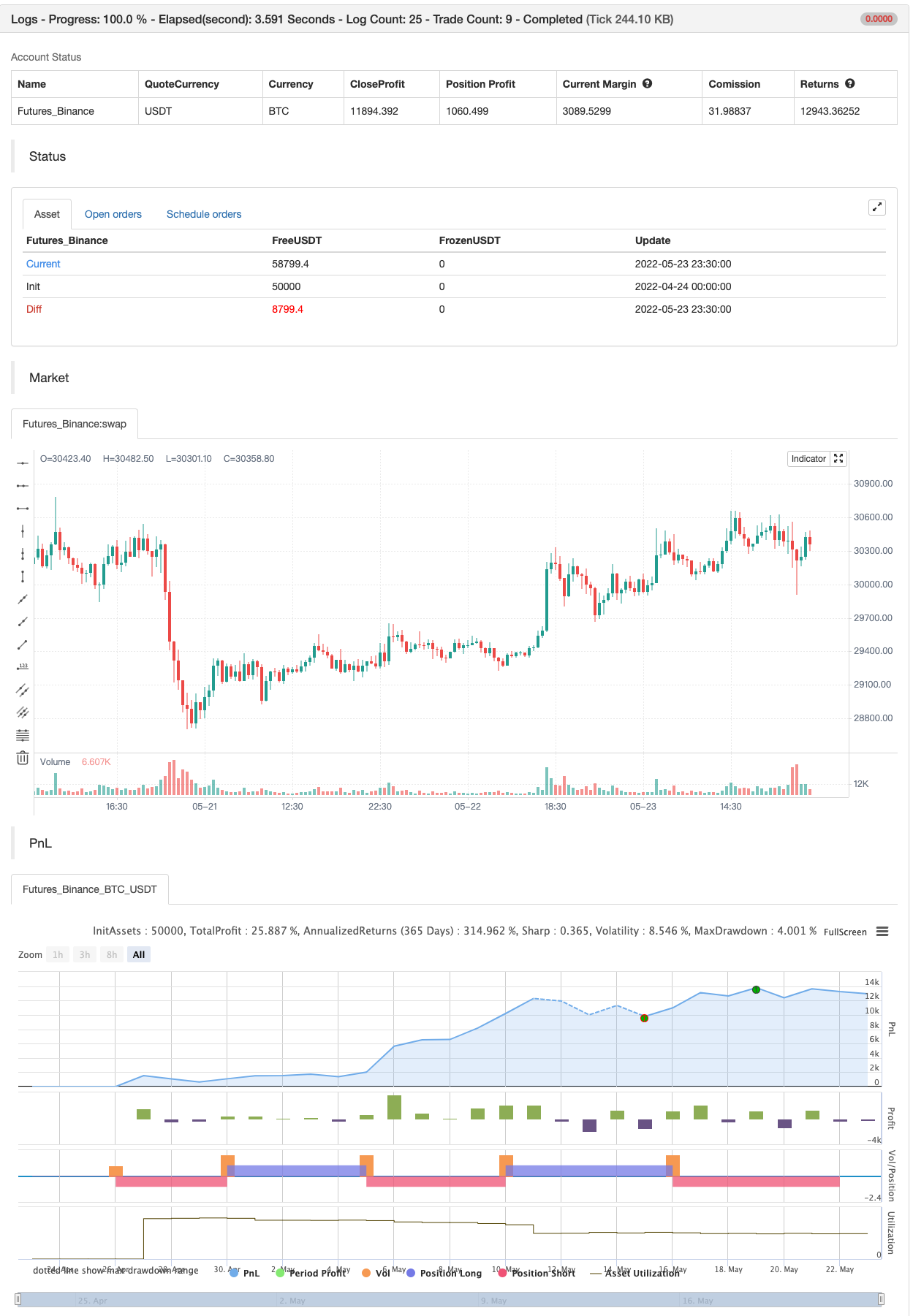

Prueba posterior

/*backtest

start: 2022-04-24 00:00:00

end: 2022-05-23 23:59:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Stochastic + RSI, Double Strategy (by ChartArt)", shorttitle="CA_-_RSI_Stoch_Strat", overlay=true)

// ChartArt's Stochastic Slow + Relative Strength Index, Double Strategy

//

// Version 1.0

// Idea by ChartArt on October 23, 2015.

//

// This strategy combines the classic RSI

// strategy to sell when the RSI increases

// over 70 (or to buy when it falls below 30),

// with the classic Stochastic Slow strategy

// to sell when the Stochastic oscillator

// exceeds the value of 80 (and to buy when

// this value is below 20).

//

// This simple strategy only triggers when

// both the RSI and the Stochastic are together

// in overbought or oversold conditions.

//

// List of my work:

// https://www.tradingview.com/u/ChartArt/

///////////// Stochastic Slow

Stochlength = input(14, minval=1, title="lookback length of Stochastic")

StochOverBought = input(80, title="Stochastic overbought condition")

StochOverSold = input(20, title="Stochastic oversold condition")

smoothK = input(3, title="smoothing of Stochastic %K ")

smoothD = input(3, title="moving average of Stochastic %K")

k = sma(stoch(close, high, low, Stochlength), smoothK)

d = sma(k, smoothD)

///////////// RSI

RSIlength = input( 14, minval=1 , title="lookback length of RSI")

RSIOverBought = input( 70 , title="RSI overbought condition")

RSIOverSold = input( 30 , title="RSI oversold condition")

RSIprice = close

vrsi = rsi(RSIprice, RSIlength)

///////////// Double strategy: RSI strategy + Stochastic strategy

if (not na(k) and not na(d))

if (crossover(k,d) and k < StochOverSold)

if (not na(vrsi)) and (crossover(vrsi, RSIOverSold))

strategy.entry("LONG", strategy.long, comment="StochLE + RsiLE")

if (crossunder(k,d) and k > StochOverBought)

if (crossunder(vrsi, RSIOverBought))

strategy.entry("SHORT", strategy.short, comment="StochSE + RsiSE")

//plot(strategy.equity, title="equity", color=red, linewidth=2, style=areabr)

Relacionados

- La estrategia de compra y venta depende de AO+Stoch+RSI+ATR

- Las bandas de Bollinger Estocástico RSI Estrategia de señal extrema

- BBSR Estrategia extrema

- RSI - Señales de compra y venta

- Estrategias de ajuste estadístico del RSI

- Las operaciones de las entidades de crédito se clasifican en el modelo de referencia.

- Estrategia del índice de fortaleza relativa del RSI

- SuperTREX

- TMA-herencia

- Bollinger + RSI, doble estrategia v1.1

Más.

- Canal SSL

- Estrategia de la suite del casco

- Parabólico SAR Comprar y vender

- El valor de las emisiones de gases de efecto invernadero es el valor de las emisiones de gases de efecto invernadero.

- Nick Rypock trasero hacia atrás (NRTR)

- ZigZag PA estrategia V4.1

- Venta y compra intradiarias

- Fractal roto: el sueño roto de alguien es su beneficio!

- Maximizador de ganancias PMax

- Una estrategia de victoria impecable

- Estrategia Swing Hull/rsi/EMA

- Instrumento de negociación de movimiento de cuero cabelludo R1-4

- La mejor estrategia de ingestión + escape

- Bollinger Awesome Alerta R1 en el momento en el que se produce el cambio

- Plugins para intercambio simultáneo

- Triángulo de interés (para obtener el precio de mercado de las monedas pequeñas)

- Grilla dinámica de contrato inverso bybit (grilla específica)

- Alertas de TradingView para MT4 MT5 + variables dinámicas NO-REPAINTING

- Serie de matrices

- Super Scalper - 5 Min 15 Min