ストカスティック+RSI,ダブル戦略

作者: リン・ハーンチャオチャン, 日時: 2022-05-25 16:12:14タグ:ストックRSI

この戦略は,RSIが70を超えると売る (または30を下回ると購入する) 伝統的なRSI戦略と,ストカスティック・スロー戦略を組み合わせて,ストカスティック・オシレーターが80を超えると売る (そして20を下回ると購入する) 伝統的なストカスティック・スロー戦略を組み合わせています.

この簡単な戦略は,RSI とストカスティックが両方が過買いまたは過売状態にある場合にのみ起動します.S&P 500の1時間チャートは最近この二重戦略でかなりうまく機能しました.

この戦略は,RSIのみを測定する"ストカスティックRSI"と混同すべきではありません.

すべての取引には高いリスクが伴う.過去の業績は必ずしも将来の結果を示すものではない.

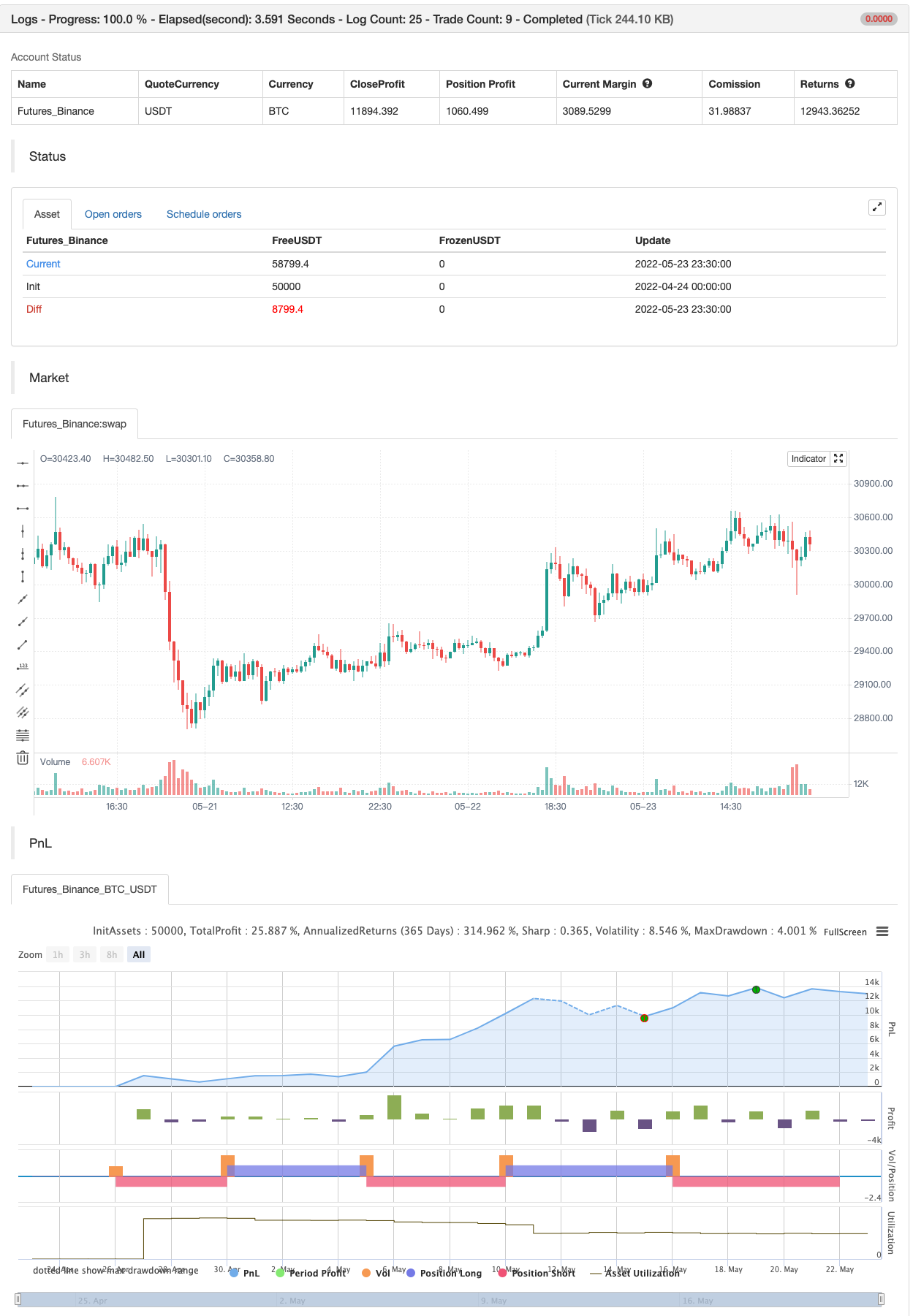

バックテスト

/*backtest

start: 2022-04-24 00:00:00

end: 2022-05-23 23:59:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Stochastic + RSI, Double Strategy (by ChartArt)", shorttitle="CA_-_RSI_Stoch_Strat", overlay=true)

// ChartArt's Stochastic Slow + Relative Strength Index, Double Strategy

//

// Version 1.0

// Idea by ChartArt on October 23, 2015.

//

// This strategy combines the classic RSI

// strategy to sell when the RSI increases

// over 70 (or to buy when it falls below 30),

// with the classic Stochastic Slow strategy

// to sell when the Stochastic oscillator

// exceeds the value of 80 (and to buy when

// this value is below 20).

//

// This simple strategy only triggers when

// both the RSI and the Stochastic are together

// in overbought or oversold conditions.

//

// List of my work:

// https://www.tradingview.com/u/ChartArt/

///////////// Stochastic Slow

Stochlength = input(14, minval=1, title="lookback length of Stochastic")

StochOverBought = input(80, title="Stochastic overbought condition")

StochOverSold = input(20, title="Stochastic oversold condition")

smoothK = input(3, title="smoothing of Stochastic %K ")

smoothD = input(3, title="moving average of Stochastic %K")

k = sma(stoch(close, high, low, Stochlength), smoothK)

d = sma(k, smoothD)

///////////// RSI

RSIlength = input( 14, minval=1 , title="lookback length of RSI")

RSIOverBought = input( 70 , title="RSI overbought condition")

RSIOverSold = input( 30 , title="RSI oversold condition")

RSIprice = close

vrsi = rsi(RSIprice, RSIlength)

///////////// Double strategy: RSI strategy + Stochastic strategy

if (not na(k) and not na(d))

if (crossover(k,d) and k < StochOverSold)

if (not na(vrsi)) and (crossover(vrsi, RSIOverSold))

strategy.entry("LONG", strategy.long, comment="StochLE + RsiLE")

if (crossunder(k,d) and k > StochOverBought)

if (crossunder(vrsi, RSIOverBought))

strategy.entry("SHORT", strategy.short, comment="StochSE + RsiSE")

//plot(strategy.equity, title="equity", color=red, linewidth=2, style=areabr)

関連性

- 買・売戦略は AO+Stoch+RSI+ATRに依存する

- Bollinger Bands ストカスティック RSI エクストリーム・シグナル戦略

- BBSR エクストリーム戦略

- RSI - 買って売るシグナル

- RSIの統計的な利回り戦略

- RSI MTF Ob+Os

- RSI相対強度指数戦略

- スーパートレックス

- TMA-レガシー

- ボリンガー+RSI,ダブル戦略 v1.1

もっと

- SSLチャネル

- ハル・スイート戦略

- パラボリック SAR 買って売る

- ピボットベース トレイリング マキシマ・ミニマ

- ニック・ライポック トレイリング・リバース (NRTR)

- ジグザグPA戦略 V4.1

- 日中の買い/売る

- 壊れたフラクタル: 誰かの壊れた夢はあなたの利益です!

- 利益の最大化 PMax

- 完璧 な 勝利 の 戦略

- スウィング・ハル/RSI/EMA戦略

- Scalping Swing Trading ツール R1-4

- 最良の飲み込み+脱出戦略

- Bollinger Awesome アラート R1

- マルチ取引所兼用プラグイン

- 三角利息 (小額通貨の格差)

- bybit逆契約動的格子 (特異格子)

- MT4 MT5 + ダイナミック変数へのTradingViewアラート

- マトリックスシリーズ

- スーパースカルパー - 5分 15分