適応的ボラティリティに基づく有限体積要素戦略

1

Follow

1802

Followers

概要

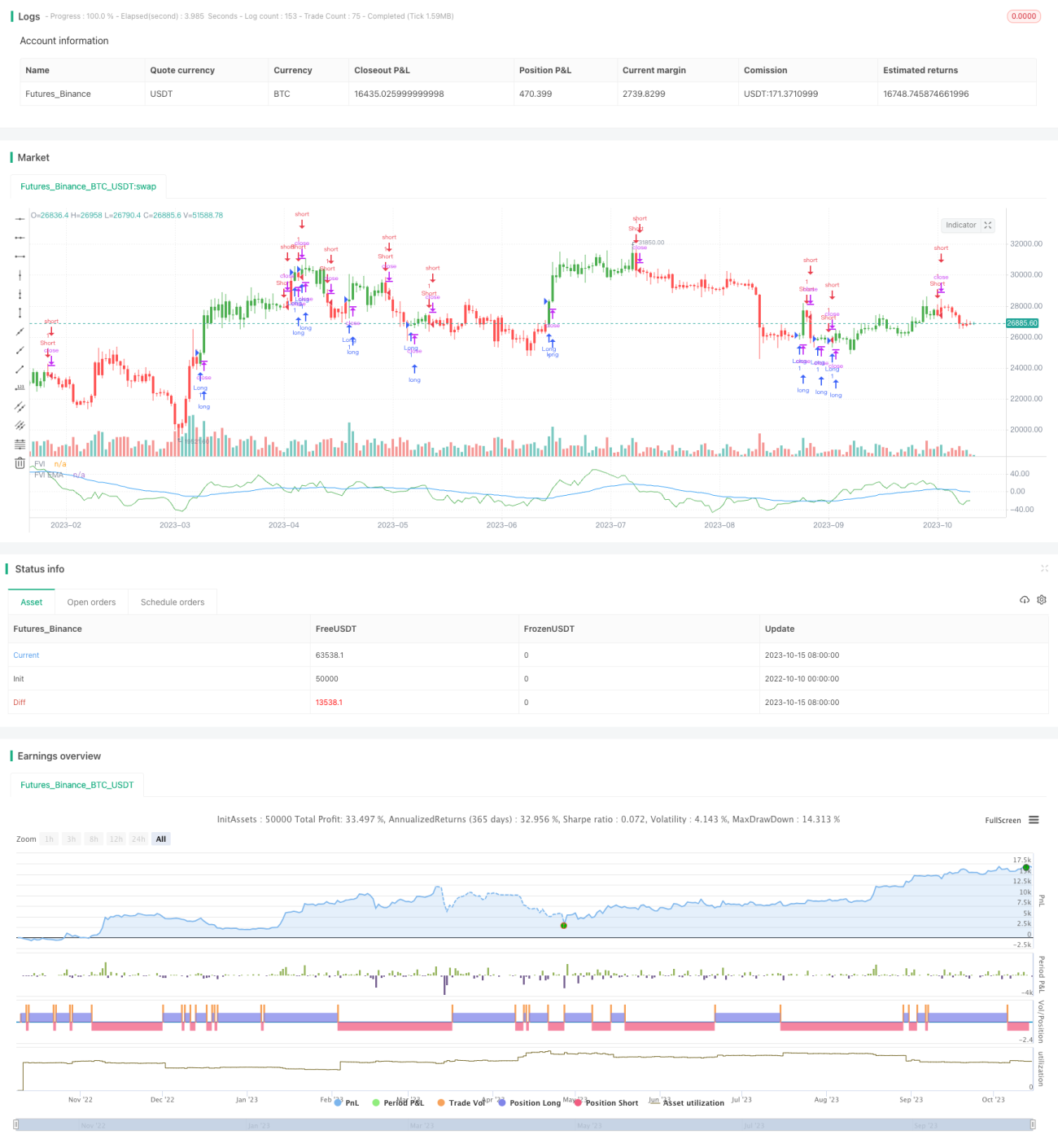

本戦略は有限体積要素法と適応的ボラティリティ計測を組み合わせ、価格変動に対する買い・売りの判断を行うトレンドフォロー型戦略です。様々な時間足に対応し、パラメータを自動調整して異なるボラティリティレベルに適応します。

原理

まず、直近N本のローソク足の高値・安値の平均価格、終値の平均価格、およびその前のローソク足の高値・安値・終値の平均価格を計算します。次に、現在のローソク足と前のローソク足の対数収益率 Intra および Inter を算出します。同時に、Intra と Inter のボラティリティ Vintra および Vinter を計算します。

ボラティリティの水準と調整可能なパラメータに基づき、適応的なカットオフ係数 CutOff を計算します。価格変動が CutOff を超えた場合、買い・売りのシグナルを生成します。具体的には、現在のローソク足の終値と高値・安値の平均価格の差 MF を計算し、MF が CutOff より大きい場合は買いシグナル、MF が CutOff の負値より小さい場合は売りシグナルとします。

最後にシグナルに基づいて資金フローを計算し、シグナル pos を出力し、有限体積要素曲線 FVE を描画します。

長所

- パラメータが適応的であり、異なる時間足やボラティリティレベルに対応するため、人手による調整が不要。

- 価格のトレンド変化を正確に捉える。

- 有限体積要素曲線が買い・売りの勢力バランスを明確に示す。

- 資金フロー理論に基づきシグナルが比較的信頼できる。

リスク

- 市場が激しく変動する場合、誤ったシグナルが増える可能性がある。Nパラメータを適宜調整することで対策可能。

- 価格のギャップ(窓開け)を処理できない。他の指標と組み合わせて補完することを検討する。

- 資金フロー理論とテクニカル分析のシグナルが乖離する場合がある。複数のシグナルを総合的に判断することが望ましい。

最適化の方向性

- Nパラメータの異なる値が結果に与える影響をテストする。一般にNを大きめに設定することでノイズを除去できる。

- Cintra と Cinter の異なる値をテストし、最適なパラメータ組み合わせを見つける。これらのパラメータを動的に調整することも検討する。

- MACDなどの他の指標と組み合わせることで、戦略の安定性を高める。

- ストップロス機構を導入し、1回あたりの損失を抑制する。

まとめ

本戦略は全体的に信頼性が高く、原理も優れており、トレンドフォロー戦略の一部として活用できる。他の戦略と適切に組み合わせることで、より効果を発揮する。鍵となるのは最適なパラメータを見つけ、堅牢なリスク管理策を確立することである。今後さらに最適化を進めれば、非常に強力なトレンドフォロー戦略となるだろう。

Source

Pine

/*backtest

start: 2022-10-10 00:00:00

end: 2023-10-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/08/2017

// This is another version of FVE indicator that we have posted earlier Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1