스토카스틱 + RSI, 이중 전략

저자:차오장, 날짜: 2022-05-25 16:12:14태그:스톡RSI

이 전략은 고전적인 RSI 전략을 결합하여 RSI가 70보다 높을 때 판매 (또는 30 이하로 떨어지면 구매) 하고, 고전적인 스토카스틱 슬로우 전략을 결합하여 스토카스틱 오시레이터가 80의 값을 초과할 때 판매 (그리고 이 값이 20 이하일 때 구매) 합니다.

이 간단한 전략은 RSI와 스토카스틱이 모두 과잉 구매 또는 과잉 판매 상태에서 함께 있을 때만 작동합니다. S&P 500의 한 시간 차트는 최근에 이 두 가지 전략으로 꽤 잘 작동했습니다.

이 전략은

모든 거래는 높은 위험을 포함하고 있습니다. 과거의 성과가 반드시 미래의 결과를 나타내는 것은 아닙니다.

백테스트

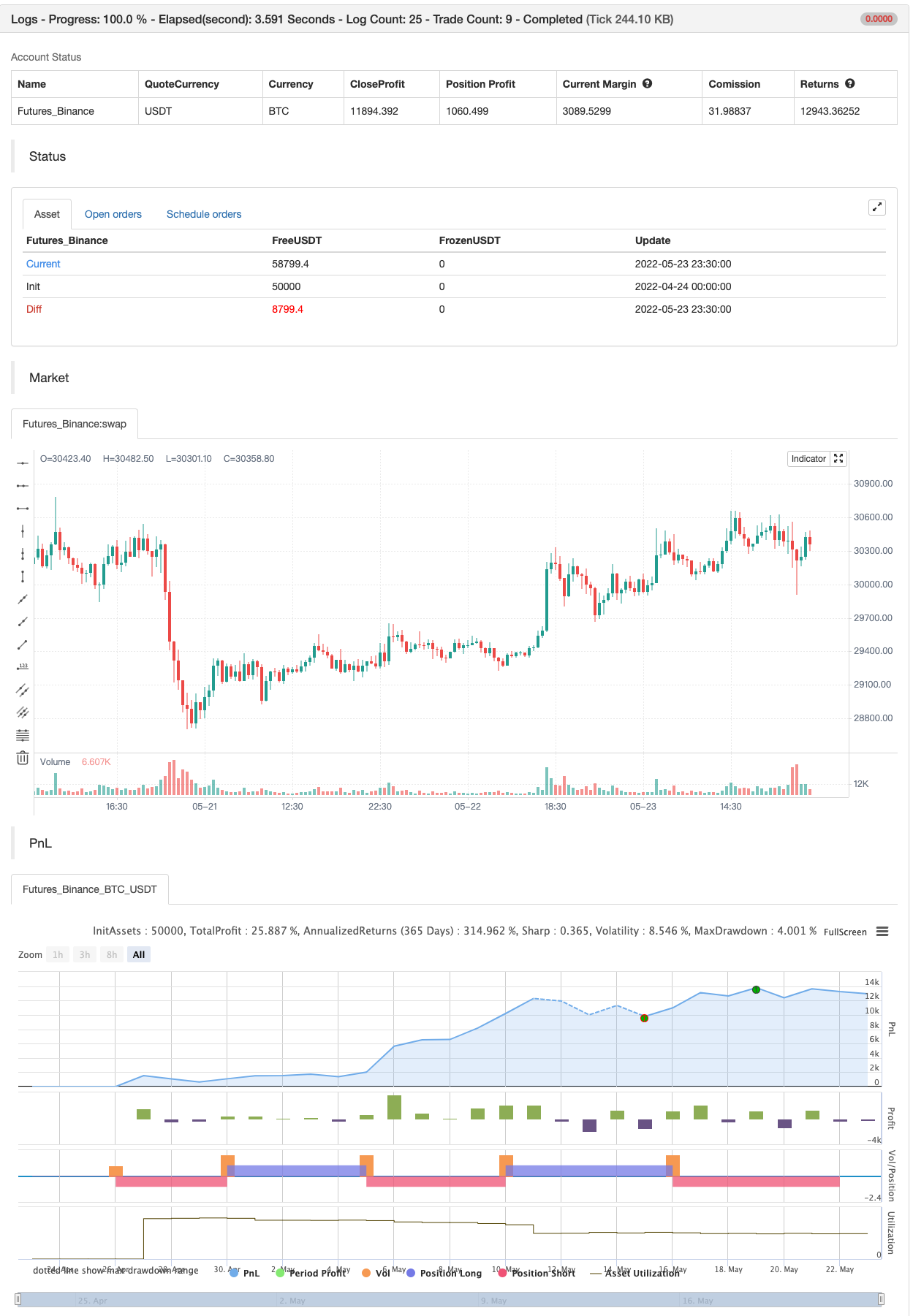

/*backtest

start: 2022-04-24 00:00:00

end: 2022-05-23 23:59:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Stochastic + RSI, Double Strategy (by ChartArt)", shorttitle="CA_-_RSI_Stoch_Strat", overlay=true)

// ChartArt's Stochastic Slow + Relative Strength Index, Double Strategy

//

// Version 1.0

// Idea by ChartArt on October 23, 2015.

//

// This strategy combines the classic RSI

// strategy to sell when the RSI increases

// over 70 (or to buy when it falls below 30),

// with the classic Stochastic Slow strategy

// to sell when the Stochastic oscillator

// exceeds the value of 80 (and to buy when

// this value is below 20).

//

// This simple strategy only triggers when

// both the RSI and the Stochastic are together

// in overbought or oversold conditions.

//

// List of my work:

// https://www.tradingview.com/u/ChartArt/

///////////// Stochastic Slow

Stochlength = input(14, minval=1, title="lookback length of Stochastic")

StochOverBought = input(80, title="Stochastic overbought condition")

StochOverSold = input(20, title="Stochastic oversold condition")

smoothK = input(3, title="smoothing of Stochastic %K ")

smoothD = input(3, title="moving average of Stochastic %K")

k = sma(stoch(close, high, low, Stochlength), smoothK)

d = sma(k, smoothD)

///////////// RSI

RSIlength = input( 14, minval=1 , title="lookback length of RSI")

RSIOverBought = input( 70 , title="RSI overbought condition")

RSIOverSold = input( 30 , title="RSI oversold condition")

RSIprice = close

vrsi = rsi(RSIprice, RSIlength)

///////////// Double strategy: RSI strategy + Stochastic strategy

if (not na(k) and not na(d))

if (crossover(k,d) and k < StochOverSold)

if (not na(vrsi)) and (crossover(vrsi, RSIOverSold))

strategy.entry("LONG", strategy.long, comment="StochLE + RsiLE")

if (crossunder(k,d) and k > StochOverBought)

if (crossunder(vrsi, RSIOverBought))

strategy.entry("SHORT", strategy.short, comment="StochSE + RsiSE")

//plot(strategy.equity, title="equity", color=red, linewidth=2, style=areabr)

관련

- 매수 전략은 AO+Stoch+RSI+ATR에 달려 있습니다.

- 볼링거 밴드 스토카스틱 RSI 극심 신호 전략

- BBSR 극단적 전략

- RSI - 구매 판매 신호

- RSI 통계적 오프팅 전략

- RSI MTF Ob+Os

- RSI 상대적 강도 지수 전략

- 슈퍼트렉스

- TMA-레거시

- 볼링거 + RSI, 더블 전략 v1.1

더 많은

- SSL 채널

- 헬스 스위트 전략

- 파라볼 SAR 구매 및 판매

- 피보트 기반 후속 최대 & 최소

- 닉 라이팍 후속 역전 (NRTR)

- ZigZag PA 전략 V4.1

- 내일 구매/판매

- 깨진 프랙탈: 누군가의 깨진 꿈은 당신의 이익입니다!

- 이윤 극대화 PMax

- 흠 이 없는 승리 전략

- 스윙 헐/rsi/EMA 전략

- 스칼핑 스윙 거래 도구 R1-4

- 가장 좋은 삼키기 + 탈출 전략

- Bollinger Awesome 알렛 R1

- 다중 거래소 통합 플러그인

- 삼각수당 (작은 통화의 거래 가격 차이)

- bybit 역계약 동적 격자 (特異格子)

- MT4 MT5 + 동적 변수 NOT-REPAINT

- 매트릭스 시리즈

- 슈퍼 스칼퍼 - 5분 15분