적응형 변동성 기반 유한 체적 요소 전략

1

Follow

1802

Followers

개요

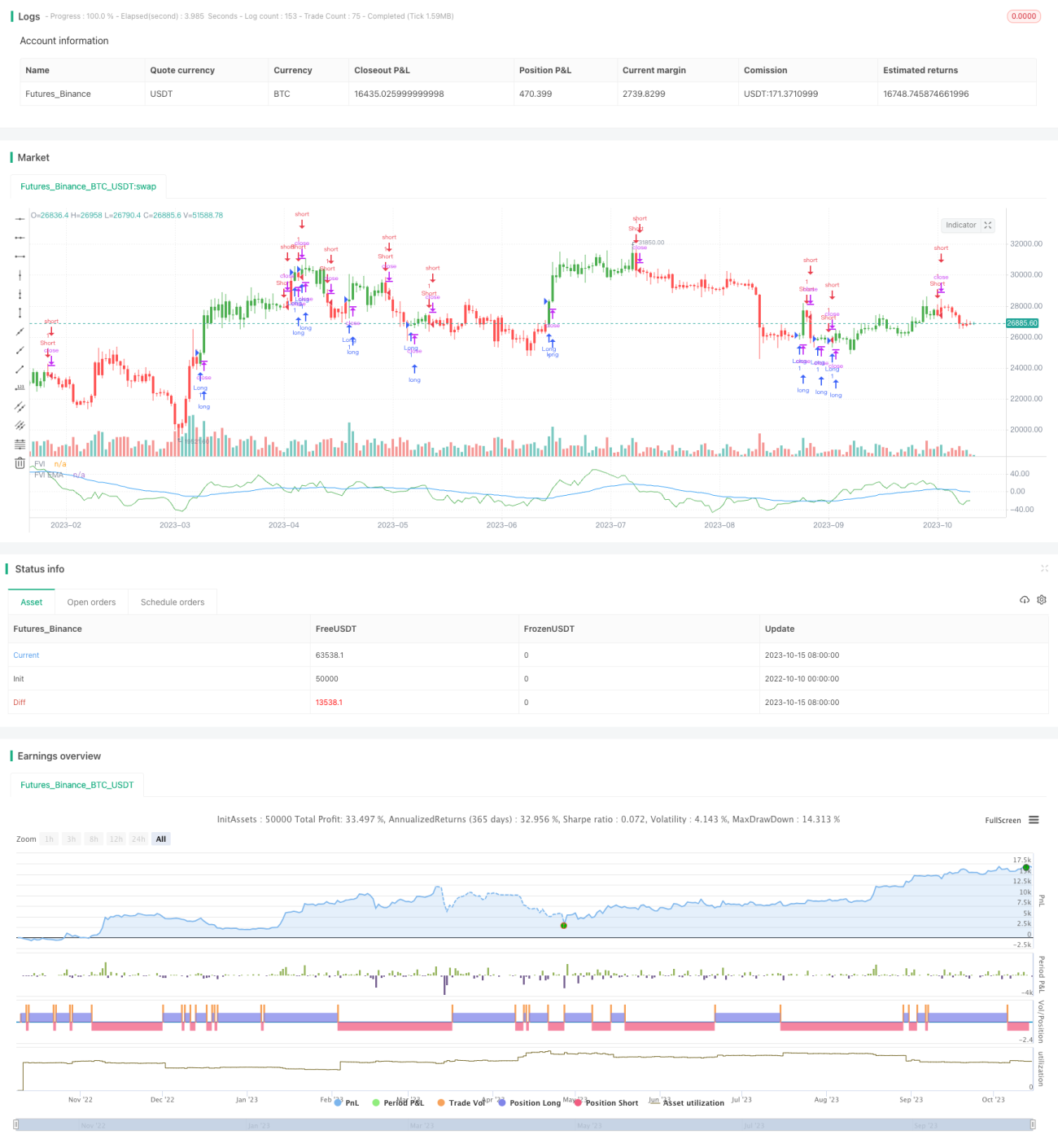

본 전략은 유한 체적 요소 방법을 활용하여 적응형 변동성 측정과 결합해 가격 변화에 대한 롱·숏 신호를 판단하는 추세 추종형 전략입니다. 전략은 모든 시간 주기에 적용 가능하며 파라미터를 자동으로 조정하여 다양한 변동성 수준에 적응합니다.

원리

전략은 먼저 최근 N개 캔들의 고가·저가 평균, 종가 평균, 그리고 직전 캔들의 고가·저가·종가 평균을 계산합니다. 그런 다음 현재 캔들과 이전 캔들의 로그 수익률 Intra 및 Inter를 계산합니다. 동시에 Intra와 Inter의 변동성 Vintra와 Vinter도 계산합니다.

변동성 수준과 조정 가능한 파라미터를 기반으로 적응형 절단 계수 CutOff를 계산합니다. 가격 변화가 CutOff를 초과하면 롱 또는 숏 신호를 생성합니다. 구체적으로 현재 캔들의 종가와 고가·저가 평균의 차이 MF를 계산하여 MF가 CutOff보다 크면 롱 신호, MF가 음의 CutOff보다 작으면 숏 신호를 생성합니다.

마지막으로 신호에 따라 자금 흐름을 계산하고, outputs 신호 pos를 출력하며 유한 체적 요소 곡선 FVE를 그립니다.

장점

- 적응형 파라미터로 다양한 주기와 변동성 수준에 적용 가능하여 수동 조정이 필요 없습니다.

- 가격 추세 변화를 정확하게 포착합니다.

- 유한 체적 요소 곡선이 롱·숏 세력 비교를 명확하게 반영합니다.

- 자금 흐름 이론이 견고하여 신호가 비교적 신뢰할 수 있습니다.

위험

- 시장이 급격하게 변동할 때 잘못된 신호가 많이 발생할 수 있습니다. N 파라미터를 적절히 조정할 수 있습니다.

- 가격 갭을 처리할 수 없습니다. 다른 지표를 추가하여 보완할 수 있습니다.

- 자금 흐름 이론과 기술적 분석 신호 간 괴리가 발생할 수 있습니다. 여러 신호를 종합적으로 판단할 수 있습니다.

최적화 방향

- 다양한 N 파라미터가 결과에 미치는 영향을 테스트할 수 있습니다. 일반적으로 N을 크게 설정하면 과도한 노이즈를 걸러낼 수 있습니다.

- Cintra와 Cinter의 다양한 값을 테스트하여 최적의 파라미터 조합을 찾을 수 있습니다. 두 파라미터를 동적으로 조정하는 것도 고려할 수 있습니다.

- MACD 등 다른 지표와 결합하여 전략의 안정성을 높일 수 있습니다.

- 손절 메커니즘을 구축하여 단일 손실을 제어할 수 있습니다.

요약

본 전략은 전반적으로 비교적 신뢰할 수 있으며 원리가 우수하여 추세 추종 전략의 구성 요소로 활용할 수 있습니다. 다른 전략과 적절히 조합하면 더 좋은 효과를 낼 수 있습니다. 핵심은 최적의 파라미터를 찾고 견고한 위험 관리 조치를 구축하는 것입니다. 추후 지속적으로 최적화된다면 매우 강력한 추세 추종 전략이 될 것입니다.

Source

Pine

/*backtest

start: 2022-10-10 00:00:00

end: 2023-10-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/08/2017

// This is another version of FVE indicator that we have posted earlier Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1