FTSMA - Trend é o teu amigo

Autora:ChaoZhang, Data: 26 de Maio de 2022Tags:EMASMARMA

Esta é a minha nova estratégia sólida: se acredita que

Eu testei com muitos pares e em muitos prazos e tenho lucro com apenas pequenas mudanças nas configurações. Sugiro usá-lo para negociação intradiária.

NOTA MUITO IMPORTANTE: esta é uma estratégia de seguimento de tendências, portanto, o objetivo é permanecer no comércio o máximo possível.

Esta estratégia usa médias móveis aplicadas a ondas de Fourier para prever a direção da tendência.

Como funciona a estratégia:

- Comprar quando a MA rápida estiver acima da MA média e o preço estiver acima da MA lenta, o que funciona como um indicador de tendência.

- Vender quando o MA rápido estiver abaixo do MA médio e o preço estiver abaixo do MA lento, o que funciona como um indicador de tendência.

A estratégia usa um monte de pedidos piramidal porque quando você está em uma fase de mercado plano que vai fechar 1 ou 2 ordens com uma perda, mas quando uma grande tendência começa, ele terá lucro em um monte de ordens.

Então, se você analisar cuidadosamente os resultados da estratégia, você notará que

Obrigado a todos os pinescriptores mencionados no código pelos seus fragmentos.

Eu também tenho um estudo com alertas. Próxima melhoria (apenas para quem está interessado neste script e me segue): estudar com alertas em vários tickers todos em um. Deixe um comentário se você quiser ter acesso ao estudo.

Como usar estratégias e estudar juntos: 1- Adicione ao mapa a estratégia primeiro, para que o seu espaço de trabalho seja o mais limpo possível. 2- Abra a guia Strategy Tester no rodapé da página. 3- Modificar as configurações para obter os melhores resultados (Profit, Profit Factor, Drawdown). 4- Adicione estudo com alertas ao seu gráfico com a mesma configuração de estratégia. Vou fornecer um guia de instalação rápido e detalhado com o estudo!

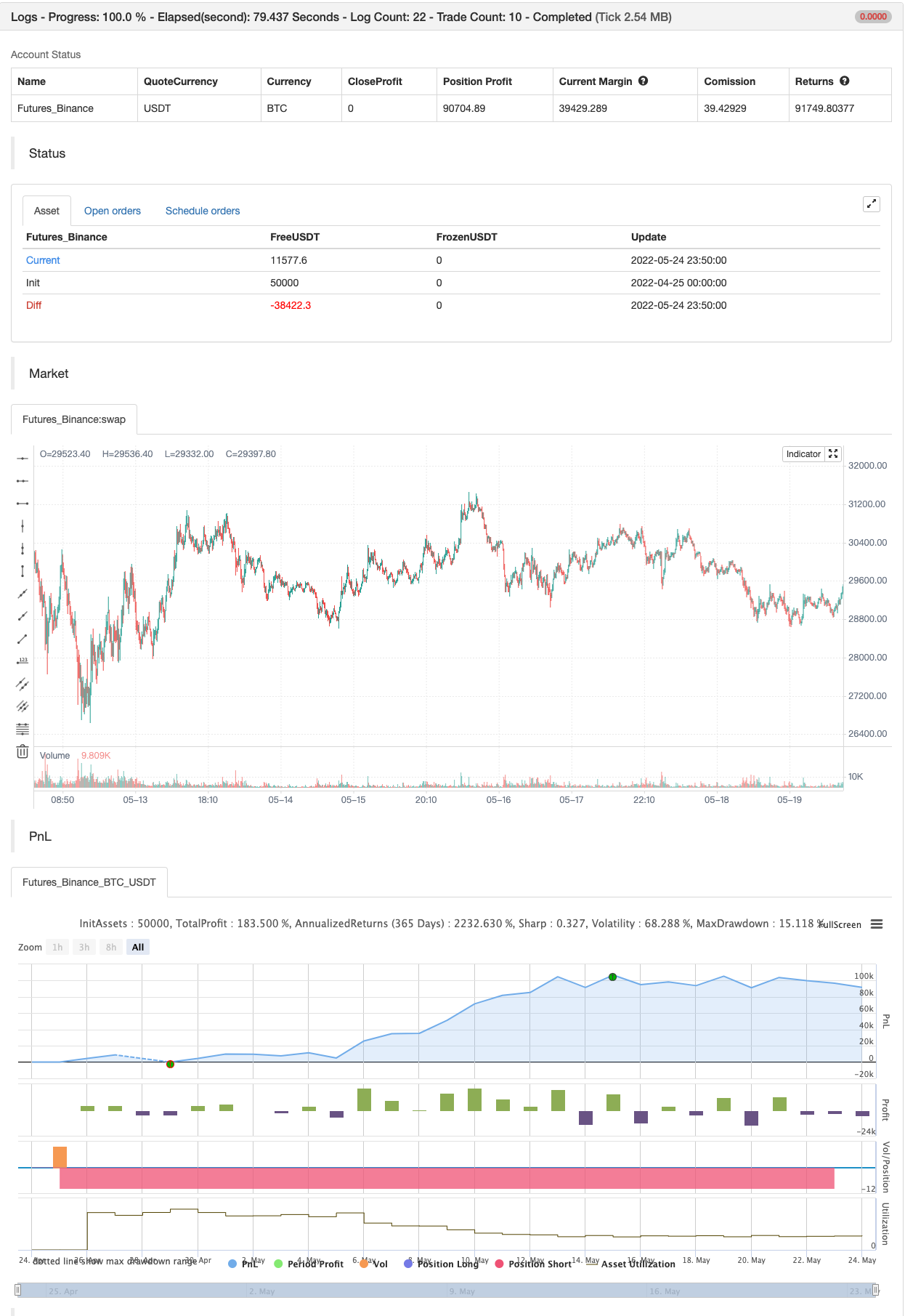

backtest

/*backtest

start: 2022-04-25 00:00:00

end: 2022-05-24 23:59:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © 03.freeman

//@version=4

strategy("FTSMA", overlay=true, precision=6, initial_capital=10000,calc_on_every_tick=true, pyramiding=10, default_qty_type=strategy.fixed, default_qty_value=10000, currency=currency.EUR)

src=input(close,"Source")

slowMA=input(200,"Slow MA period")

mediumMA=input(20,"Mid MA period")

fastMA=input(5,"Fast MA period")

plotSMA=input(true,"Use MA")

sin1=input(1,"First sinusoid",minval=1)

sin2=input(2,"Second sinusoid",minval=1)

sin3=input(3,"Third sinusoid",minval=1)

smoothinput = input('EMA', title = "MA Type", options =['EMA', 'SMA', 'ALMA','FRAMA','RMA', 'SWMA', 'VWMA','WMA','LinearRegression'])

linearReg=input(false, "Use linear regression?")

linregLenght=input(13, "Linear regression lenght")

linregOffset=input(0, "Linear regression offset")

//------FRAMA ma---------

ma(src, len) =>

float result = 0

int len1 = len/2

frama_SC=200

frama_FC=1

e = 2.7182818284590452353602874713527

w = log(2/(frama_SC+1)) / log(e) // Natural logarithm (ln(2/(SC+1))) workaround

H1 = highest(high,len1)

L1 = lowest(low,len1)

N1 = (H1-L1)/len1

H2_ = highest(high,len1)

H2 = H2_[len1]

L2_ = lowest(low,len1)

L2 = L2_[len1]

N2 = (H2-L2)/len1

H3 = highest(high,len)

L3 = lowest(low,len)

N3 = (H3-L3)/len

dimen1 = (log(N1+N2)-log(N3))/log(2)

dimen = iff(N1>0 and N2>0 and N3>0,dimen1,nz(dimen1[1]))

alpha1 = exp(w*(dimen-1))

oldalpha = alpha1>1?1:(alpha1<0.01?0.01:alpha1)

oldN = (2-oldalpha)/oldalpha

N = (((frama_SC-frama_FC)*(oldN-1))/(frama_SC-1))+frama_FC

alpha_ = 2/(N+1)

alpha = alpha_<2/(frama_SC+1)?2/(frama_SC+1):(alpha_>1?1:alpha_)

frama = 0.0

frama :=(1-alpha)*nz(frama[1]) + alpha*src

result := frama

result

// ----------MA calculation - ChartArt and modified by 03.freeman-------------

calc_ma(src,l) =>

_ma = smoothinput=='SMA'?sma(src, l):smoothinput=='EMA'?ema(src, l):smoothinput=='WMA'?wma(src, l):smoothinput=='LinearRegression'?linreg(src, l,0):smoothinput=='VWMA'?vwma(src,l):smoothinput=='RMA'?rma(src, l):smoothinput=='ALMA'?alma(src,l,0.85,6):smoothinput=='SWMA'?swma(src):smoothinput=='FRAMA'?ma(sma(src,1),l):na

//----------------------------------------------

//pi = acos(-1)

// Approximation of Pi in _n terms --- thanks to e2e4mfck

f_pi(_n) =>

_a = 1. / (4. * _n + 2)

_b = 1. / (6. * _n + 3)

_pi = 0.

for _i = _n - 1 to 0

_a := 1 / (4. * _i + 2) - _a / 4.

_b := 1 / (6. * _i + 3) - _b / 9.

_pi := (4. * _a) + (4. * _b) - _pi

pi=f_pi(20)

//---Thanks to xyse----https://www.tradingview.com/script/UTPOoabQ-Low-Frequency-Fourier-Transform/

//Declaration of user-defined variables

N = input(defval=64, title="Lookback Period", type=input.integer, minval=2, maxval=600, confirm=false, step=1, options=[2,4,8,16,32,64,128,256,512,1024,2048,4096])

//Real part of the Frequency Domain Representation

ReX(k) =>

sum = 0.0

for i=0 to N-1

sum := sum + src[i]*cos(2*pi*k*i/N)

return = sum

//Imaginary part of the Frequency Domain Representation

ImX(k) =>

sum = 0.0

for i=0 to N-1

sum := sum + src[i]*sin(2*pi*k*i/N)

return = -sum

//Get sinusoidal amplitude from frequency domain

ReX_(k) =>

case = 0.0

if(k!=0 and k!=N/2)

case := 2*ReX(k)/N

if(k==0)

case := ReX(k)/N

if(k==N/2)

case := ReX(k)/N

return = case

//Get sinusoidal amplitude from frequency domain

ImX_(k) =>

return = -2*ImX(k)/N

//Get full Fourier Transform

x(i, N) =>

sum1 = 0.0

sum2 = 0.0

for k=0 to N/2

sum1 := sum1 + ReX_(k)*cos(2*pi*k*i/N)

for k=0 to N/2

sum2 := sum2 + ImX_(k)*sin(2*pi*k*i/N)

return = sum1+sum2

//Get single constituent sinusoid

sx(i, k) =>

sum1 = ReX_(k)*cos(2*pi*k*i/N)

sum2 = ImX_(k)*sin(2*pi*k*i/N)

return = sum1+sum2

//Calculations for strategy

SLOWMA = plotSMA?calc_ma(close+sx(0,sin1),slowMA):close+sx(0,sin1)

MEDMA = plotSMA?calc_ma(close+sx(0,sin2),mediumMA):close+sx(0,sin2)

FASTMA = plotSMA?calc_ma(close+sx(0,sin3),fastMA):close+sx(0,sin3)

SLOWMA := linearReg?linreg(SLOWMA,linregLenght,linregOffset):SLOWMA

MEDMA := linearReg?linreg(MEDMA,linregLenght,linregOffset):MEDMA

FASTMA := linearReg?linreg(FASTMA,linregLenght,linregOffset):FASTMA

//Plot 3 Low-Freq Sinusoids

plot(SLOWMA, color=color.green)

plot(MEDMA, color=color.red)

plot(FASTMA, color=color.blue)

// Strategy: (Thanks to JayRogers)

// === STRATEGY RELATED INPUTS ===

// the risk management inputs

inpTakeProfit = input(defval = 0, title = "Take Profit Points", minval = 0)

inpStopLoss = input(defval = 0, title = "Stop Loss Points", minval = 0)

inpTrailStop = input(defval = 0, title = "Trailing Stop Loss Points", minval = 0)

inpTrailOffset = input(defval = 0, title = "Trailing Stop Loss Offset Points", minval = 0)

// === RISK MANAGEMENT VALUE PREP ===

// if an input is less than 1, assuming not wanted so we assign 'na' value to disable it.

useTakeProfit = inpTakeProfit >= 1 ? inpTakeProfit : na

useStopLoss = inpStopLoss >= 1 ? inpStopLoss : na

useTrailStop = inpTrailStop >= 1 ? inpTrailStop : na

useTrailOffset = inpTrailOffset >= 1 ? inpTrailOffset : na

longCondition = FASTMA>MEDMA and close > SLOWMA //crossover(FASTMA, MEDMA) and close > SLOWMA

if (longCondition)

strategy.entry("Long Entry", strategy.long)

shortCondition = FASTMA<MEDMA and close < SLOWMA //crossunder(FASTMA, MEDMA) and close < SLOWMA

if (shortCondition)

strategy.entry("Short Entry", strategy.short)

// === STRATEGY RISK MANAGEMENT EXECUTION ===

// finally, make use of all the earlier values we got prepped

strategy.exit("Exit Buy", from_entry = "Long Entry", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset)

strategy.exit("Exit Sell", from_entry = "Short Entry", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset)

- MA HYBRID BY RAJ

- SSL híbrido

- Oscilador Arco-íris

- Modelo de alertas de lançamento lunar [indicador]

- SuperJump Volta para trás Banda de Bollinger

- Super Scalper

- A ESSMA

- MACD mais inteligente

- Super Scalper - 5 Min 15 Min

- Scalping EMA ADX RSI com compra/venda

- Tendência da SMA

- Baixos de Bollinger

- Super tendência B

- SIGNALES de comércio de balanço

- Ciclo de tendências de Schaff

- 72s: Média móvel do casco adaptativo +

- Scalping EMA ADX RSI com compra/venda

- Divergência de volume

- Super Trend Daily 2.0 BF

- Hull Moving Average Swing Trader

- Filtro de faixa Comprar e vender

- Canal SSL

- Estratégia do Hull Suite

- Parabólica SAR Compra e Venda

- Maxima e Mínima baseadas em pivô

- Nick Rypock Trailing Reverse (NRTR)

- ZigZag PA Estratégia V4.1

- Comprar/Vender intradiário

- Fractal quebrado: o sonho quebrado de alguém é o seu lucro!

- Maximizador de lucro PMax