1

关注

1802

关注者

概述

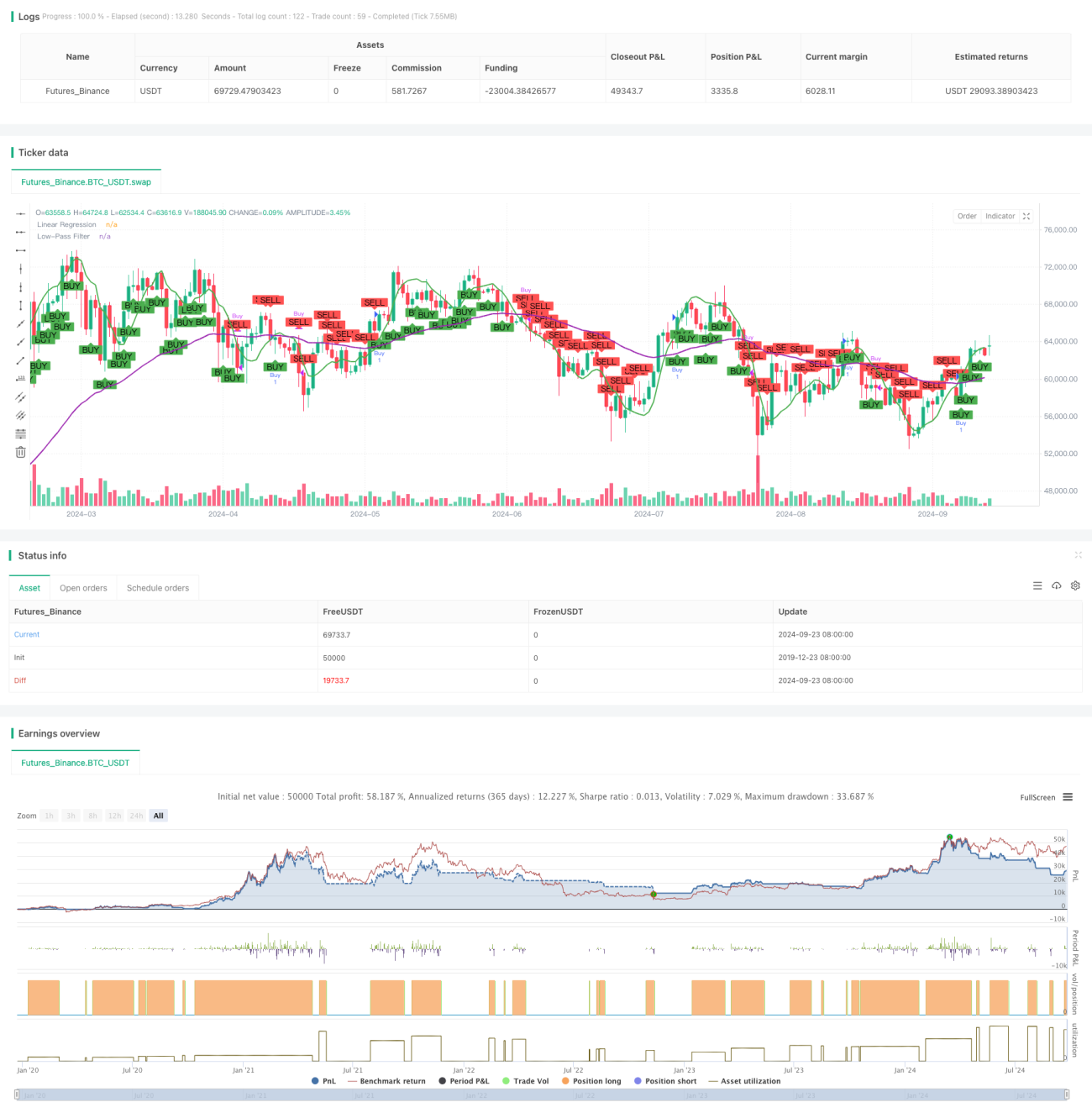

该策略是一种基于多维度数学模型的高级交易策略,利用多个数学函数和技术指标来生成交易信号。策略结合了动量、趋势和波动性分析,通过整合多个维度的市场信息来做出更全面的交易决策。

策略原理

该策略的核心原理是通过多个数学模型和技术指标来分析市场的不同方面:

- 使用变化率(ROC)指标来计算价格的动量和方向。

- 应用线性回归(Linear Regression)来识别短期价格趋势。

- 使用指数移动平均线(EMA)作为低通滤波器,以捕捉长期趋势。

- 通过Sigmoid函数来调整价格变化的波动性。

策略综合考虑这些因素,当动量为正、短期趋势上升、长期趋势确认,且波动性适中时发出买入信号。相反的条件组合则触发卖出信号。

策略优势

- 多维度分析:通过结合多个数学模型和指标,策略能够从不同角度分析市场,提高决策的全面性和准确性。

- 自适应性:使用Sigmoid函数调整波动性,使策略能够适应不同的市场条件。

- 趋势确认:结合短期和长期趋势分析,有助于减少假突破带来的风险。

- 可视化:策略在图表上绘制了线性回归线和低通滤波线,便于交易者直观理解市场走势。

策略风险

- 过度拟合:使用多个指标可能导致策略在历史数据上表现良好,但在实际交易中效果不佳。

- 滞后性:部分指标如EMA存在滞后性,可能导致入场或出场时机不够及时。

- 市场条件敏感:在剧烈波动或趋势突变的市场中,策略可能表现不佳。

- 参数敏感性:多个指标的参数设置可能对策略性能产生重大影响,需要仔细优化。

策略优化方向

- 动态参数调整:可以考虑根据市场波动性动态调整指标参数,以适应不同的市场环境。

- 增加过滤器:引入额外的过滤条件,如交易量分析或市场宽度指标,以减少假信号。

- 优化退出策略:当前策略主要关注入场点,可以开发更复杂的退出机制来优化整体性能。

- 引入机器学习:考虑使用机器学习算法来优化指标权重或识别最佳的交易机会。

总结

多维度数学模型交易策略是一种综合性强、理论基础扎实的交易方法。通过结合多个数学模型和技术指标,该策略能够从多个角度分析市场,提高交易决策的准确性。然而,策略的复杂性也带来了过度拟合和参数敏感性等风险。未来的优化方向应该注重提高策略的自适应能力和鲁棒性,以在不同市场环境中保持稳定表现。总的来说,这是一个具有潜力的策略框架,通过持续优化和测试,有望成为一个可靠的交易工具。

策略源码

Pine

相关策略

评论

全部评论 (0)

暂无数据

- 1