The term “hedging” in quantitative trading and programmatic trading is a very basic concept. In cryptocurrency quantitative trading, the typical hedging strategies are: Spots-Futures hedging, intertemporal hedging and individual spot hedging.

Most of hedging tradings are based on the price difference of two trading varieties. The concept, principle and details of hedging trading may not very clear to traders who have just entered the field of quantitative trading. That's ok, Let's use the “Data science research environment” tool provided by the FMZ Quant platform to master these knowledge.

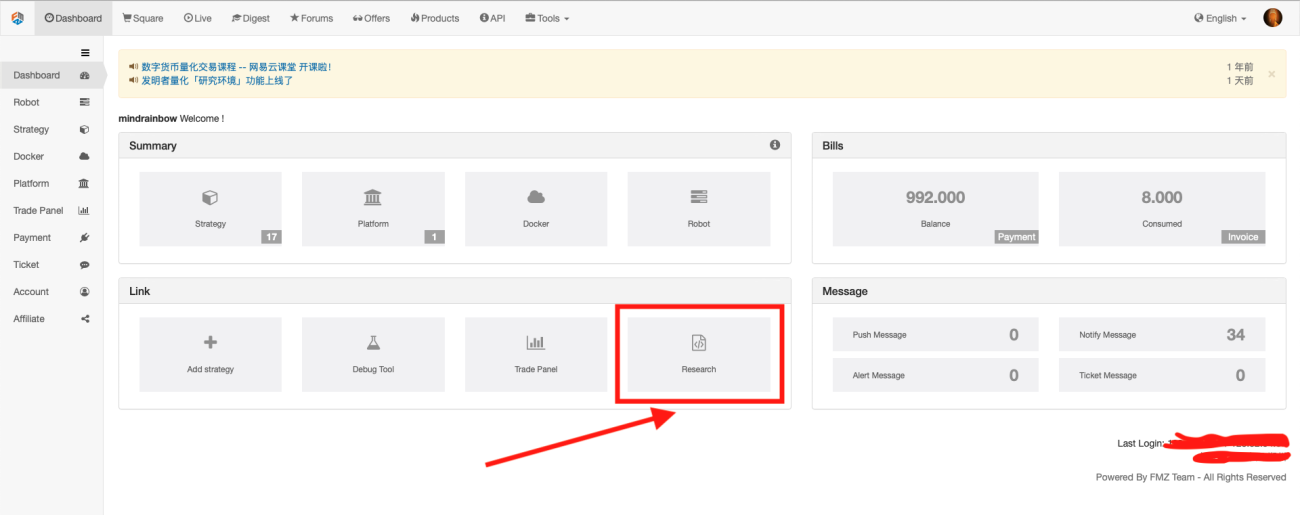

On FMZ Quant website Dashboard page, click on "Research" to jump to the page of this tool:

Here I uploaded this analysis file directly:

This analysis file is an analysis of the process of the opening and closing positions in a Spots-Futures hedging trading. The futures side exchange is OKEX and the contract is quarterly contract; The spots side exchange is OKEX spots trading. The transaction pair is BTC_USDT, The following specific analysis environment file, contains two version of it, both Python and JavaScript.

Research Environment Python Language File

Research Environment JavaScript Language File

Research environment not only supports Python, but also supports JavaScript

Below I also give an example of a JavaScript research environment:

- 1