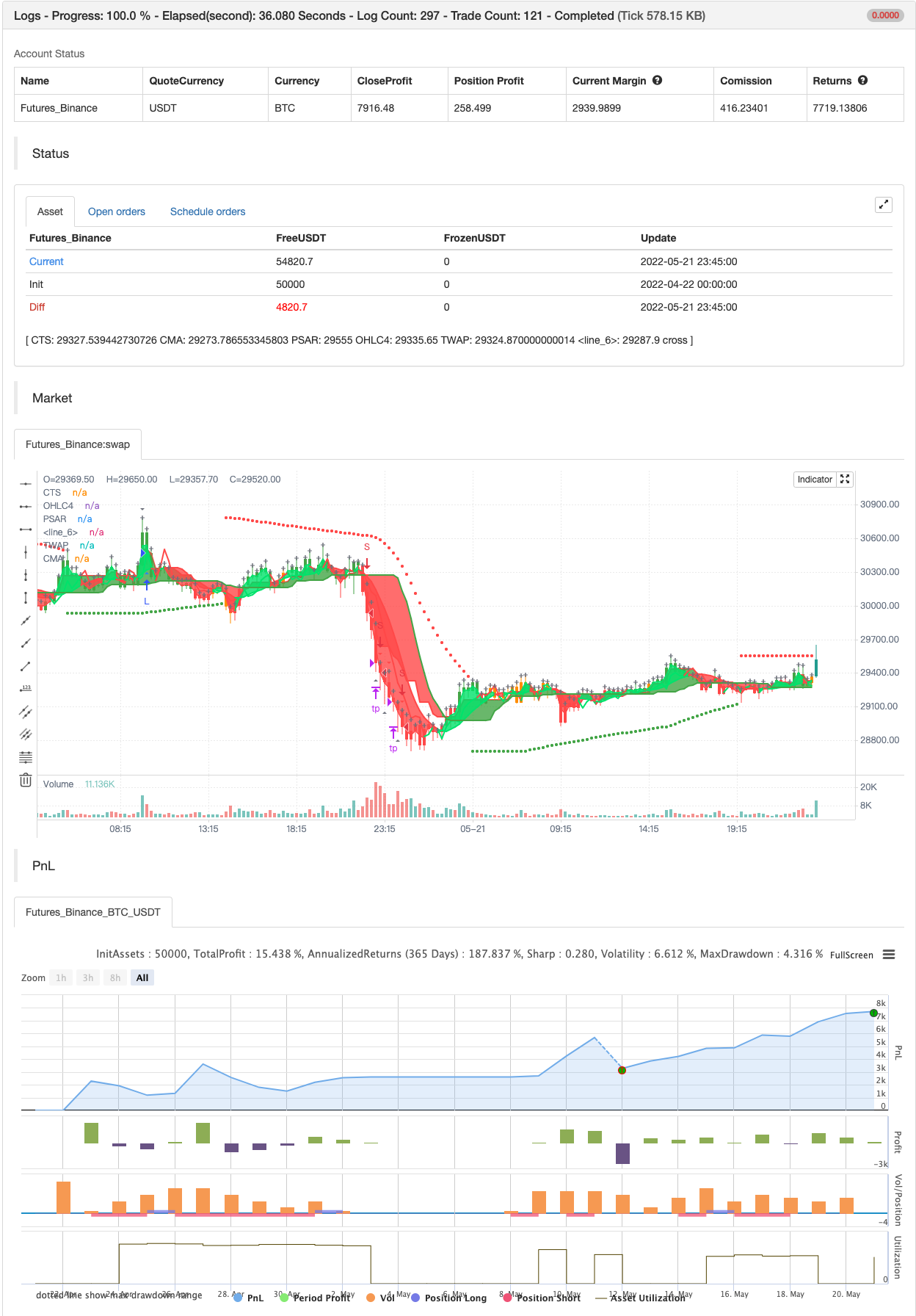

15min BTCUSDTPERP BOT

Schriftsteller:ChaoZhang, Datum: 23.05.2022Tags:ADXSARRSITWAPJMAMACD

Das ist mein BTCUSDTPERP 15 Minuten Bot Die besten Ergebnisse sind bei BTCUSDTPERP bei binancefutures. Die Ergebnisse hängen von bestimmten Volumenindikatoren ab, die bei binancefutures am besten funktionieren.

15min Bots sind wirklich schnell, es ist schwer, eine gute Konfiguration zu finden, weil von 15min Backtesting, die mindestens um 3-4 Monate

Dieser Bot ist spezifisch, hat sehr hohe Prozentsätze profitabler Trades. Netto-Gewinn ist auch sehr gut. Allerdings sind 15min-Bots extrem schwer langfristig zu verwenden, also habe ich so viele deflaut-Einstellungen wie möglich gemacht.

Also... Dieser Bot verwendet 11 verschiedene Indikatoren:

-

ADX

-

Filter für den Bereich

-

SAR

-

RSI

-

TWAP

-

JMA

-

MACD

-

Volumen DELTA

-

Volumengewicht

-

- Nein. und der letzte für die besseren Ergebnisse bei qucik Charts (15min) Ich beschloss hinzuzufügen:

-

STOCH

-

ADX - - macht eine solide Sicht auf den Trend ohne irgendeinen Betrug Wick: Lang nur auf grünen Balken, Shorts nur auf roten Balken.

-

RANGE FILTER - dieser Indikator dient der besseren Sicht auf Trends, definiert Trends, das ist wichtig für jede Bullen/Bärenfalle, was sehr hilfreich ist, weil die Trends sehr variabel sind.

-

SAR - Der parabolische SAR ist ein technischer Indikator, der verwendet wird, um die Kursrichtung eines Vermögenswerts zu bestimmen und darauf aufmerksam zu machen, wann sich die Kursrichtung ändert.

-

Wenn der RSI überkauft ist, öffnen Sie keine neuen Longs, auch wenn der RSI überverkauft ist, öffnen Sie keine neuen Shorts.

-

TWAP - hat die gleiche Aufgabe wie Range Filter, ist nur für eine bessere Sicht der Trends, Trends definieren.

-

JMA - Der Jurik Moving Average-Indikator ist eine der sichersten Möglichkeiten, um die Kurskurven innerhalb einer minimalen Zeitverzögerung zu glätten. Der Indikator bietet Devisenhändlern einen der besten Preisfilter während starker Preisbewegungen. In dieser Zeit, in der die Bitcoin-Preisaktion so stark ist, ist dieser Indikator notwendig.

-

MACD - Moving Average Convergence Divergence (MACD) ist ein trendfolgende Dynamikindikator, der die Beziehung zwischen zwei gleitenden Durchschnitten eines Wertpapierpreises zeigt. Der MACD wird berechnet, indem der 26-Perioden exponentielle gleitende Durchschnitt (EMA) von der 12-Perioden-EMA subtrahiert wird. Heute ist MacD wie JMA notwendig, um profitable Bots zu machen.

-

Volume Delta - Ein kumulativer Volume-Delta-Ansatz basierend auf dem im Oktober 2003 erschienenen Bull-Bear-Balance-Indikator von Vadim Gimelfarb im S&C Magazine.

-

Volumengewicht - ist der wichtigste Indikator für die Strategie, um offene Trades auf einem flachen Chart zu vermeiden, werden neue Trades nach einem starken Volumenbars geöffnet.

-

MA 5-10-30 - wie die vorherigen ist dies für eine bessere Sicht der Trends und die richtige Definition der Trends, auch Speed_MA werden verwendet, um die zukünftige Preisbewegung vorherzusagen.

-

Stochastic-Stock ist nützlich, um Trendumkehrungen vorherzusagen.

Genießen Sie es.

Zurückprüfung

/*backtest

start: 2022-05-20 00:00:00

end: 2022-06-18 23:59:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © wielkieef

//@version=4

strategy("15MIN BTCUSDTPERP BOT", overlay=true, pyramiding=1,initial_capital = 10000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0)

//SOURCE ==================================================================================================================================================================================================================================================================

src = input(ohlc4)

// INPUTS ==================================================================================================================================================================================================================================================================

//ADX -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Act_ADX = input(true, title = "AVERAGE DIRECTIONAL INDEX", type = input.bool)

ADX_options = input("MASANAKAMURA", title = "ADX OPTION", options = ["CLASSIC", "MASANAKAMURA"])

ADX_len = input(11, title = "ADX LENGTH", type = input.integer, minval = 1)

th = input(12, title = "ADX THRESHOLD", type = input.float, minval = 0, step = 0.5)

//Range Filter----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

length0 = input(13, title="Range Filter lenght"),mult = input(1, title="Range Filter mult")

//SAR-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

start = input(title="SAR Start", type=input.float, step=0.001, defval=0)

increment = input(title="SAR Increment", type=input.float, step=0.001, defval=0.006)

maximum = input(title="SAR Maximum", type=input.float, step=0.01, defval=1)

width = input(title="SAR Point Width", type=input.integer, minval=1, defval=1)

//RSI---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

len_3 = input(70, minval=1, title="RSI lenght")

src_3 = input(close, "RSI Source")

//TWAP Trend --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

smoothing = input(title="TWAP Smoothing", defval= 10)

resolution = input("0", "TWAP Timeframe")

//JMA------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

inp = input(title="JMA Source", type=input.source, defval=close)

reso = input(title="JMA Resolution", type=input.resolution, defval="")

rep = input(title="JMA Allow Repainting?", type=input.bool, defval=false)

src0 = security(syminfo.tickerid, reso, inp[rep ? 0 : barstate.isrealtime ? 1 : 0])[rep ? 0 : barstate.isrealtime ? 0 : 1]

lengths = input(title="JMA Length", type=input.integer, defval=4, minval=1)

//MACD------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

fast_length = input(title="MACD Fast Length", type=input.integer, defval=25)

slow_length = input(title="MACD Slow Length", type=input.integer, defval=50)

signal_length = input(title="MACD Signal Smoothing", type=input.integer, minval = 1, maxval = 50, defval = 9)

//Volume Delta -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

periodMa = input(title="Delta Length", minval=1, defval=45)

//Volume weight------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

maLength = input(title="Volume Weight Length", type=input.integer, defval=100, minval=1)

maType = input(title="Volume Weight Type", type=input.string, defval="SMA", options=["EMA", "SMA", "HMA", "WMA", "DEMA"])

rvolTrigger = input(title="Volume To Trigger Signal", type=input.float, defval=1.5, step=0.1 , minval=0.1)

//MA----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

length = input(51, minval=1, title="MA Length")

matype = input(5, minval=1, maxval=5, title="AvgType")

//Momentum------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

tmolength = input(45, title="Momentum Length")

calcLength = input(12, title="Momentum Calc length")

smoothLength = input(9, title="Momentum Smooth length")

//INDICATORS ==============================================================================================================================================================================================================================================================

//ADX----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

calcADX(_len) =>

up = change(high)

down = -change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

truerange = rma(tr, _len)

_plus = fixnan(100 * rma(plusDM, _len) / truerange)

_minus = fixnan(100 * rma(minusDM, _len) / truerange)

sum = _plus + _minus

_adx = 100 * rma(abs(_plus - _minus) / (sum == 0 ? 1 : sum), _len)

[_plus,_minus,_adx]

calcADX_Masanakamura(_len) =>

SmoothedTrueRange = 0.0

SmoothedDirectionalMovementPlus = 0.0

SmoothedDirectionalMovementMinus = 0.0

TrueRange = max(max(high - low, abs(high - nz(close[1]))), abs(low - nz(close[1])))

DirectionalMovementPlus = high - nz(high[1]) > nz(low[1]) - low ? max(high - nz(high[1]), 0) : 0

DirectionalMovementMinus = nz(low[1]) - low > high - nz(high[1]) ? max(nz(low[1]) - low, 0) : 0

SmoothedTrueRange := nz(SmoothedTrueRange[1]) - (nz(SmoothedTrueRange[1]) /_len) + TrueRange

SmoothedDirectionalMovementPlus := nz(SmoothedDirectionalMovementPlus[1]) - (nz(SmoothedDirectionalMovementPlus[1]) / _len) + DirectionalMovementPlus

SmoothedDirectionalMovementMinus := nz(SmoothedDirectionalMovementMinus[1]) - (nz(SmoothedDirectionalMovementMinus[1]) / _len) + DirectionalMovementMinus

DIP = SmoothedDirectionalMovementPlus / SmoothedTrueRange * 100

DIM = SmoothedDirectionalMovementMinus / SmoothedTrueRange * 100

DX = abs(DIP-DIM) / (DIP+DIM)*100

adx = sma(DX, _len)

[DIP,DIM,adx]

[DIPlusC,DIMinusC,ADXC] = calcADX(ADX_len)

[DIPlusM,DIMinusM,ADXM] = calcADX_Masanakamura(ADX_len)

DIPlus = ADX_options == "CLASSIC" ? DIPlusC : DIPlusM

DIMinus = ADX_options == "CLASSIC" ? DIMinusC : DIMinusM

ADX = ADX_options == "CLASSIC" ? ADXC : ADXM

ADX_color = DIPlus > DIMinus and ADX > th ? color.green : DIPlus < DIMinus and ADX > th ? color.red : color.orange

barcolor(color = Act_ADX ? ADX_color : na, title = "ADX")

//Range Filter---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

out = 0., cma = 0., cts = 0.

Var = variance(src,length0)*mult

sma = sma(src,length0)

secma = pow(nz(sma - cma[1]),2)

sects = pow(nz(src - cts[1]),2)

ka = Var < secma ? 1 - Var/secma : 0

kb = Var < sects ? 1 - Var/sects : 0

cma := ka*sma+(1-ka)*nz(cma[1],src)

cts := kb*src+(1-kb)*nz(cts[1],src)

css = cts > cma ? color.green : color.red

a = plot(cts,"CTS",color.red,2,transp=0)

b = plot(cma,"CMA",color.green,2,transp=0)

fill(a,b,color=css,transp=80)

rangegood = cts > cma

rangebad = cts < cma

//SAR-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

psar = sar(start, increment, maximum)

dir = psar < close ? 1 : -1

psarColor = dir == 1 ? color.green : color.red

psarPlot = plot(psar, title="PSAR", style=plot.style_circles, linewidth=width, color=psarColor, transp=0)

var color longColor = color.green

var color shortColor = color.red

sargood = dir ==1

sarbad = dir ==-1

//RSI---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

up_3 = rma(max(change(src_3), 0), len_3)

down_3 = rma(-min(change(src_3), 0), len_3)

rsi_3 = down_3 == 0 ? 100 : up_3 == 0 ? 0 : 100 - (100 / (1 + up_3 / down_3))

rsiob = (rsi_3 < 70)

rsios = (rsi_3 > 30)

//TWAP Trend --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

res = resolution != "0" ? resolution : timeframe.period

weight = barssince(change(security(syminfo.tickerid, res, time, lookahead=barmerge.lookahead_on)))

price = 0.

price:= weight == 0 ? src : src + nz(price[1])

twap = price / (weight + 1)

ma_ = smoothing < 2 ? twap : sma(twap, smoothing)

bullish = iff(smoothing < 2, src >= ma_, src > ma_)

disposition = bullish ? color.lime : color.red

basis = plot(src, "OHLC4", disposition, linewidth=1, transp=100)

work = plot(ma_, "TWAP", disposition, linewidth=2, transp=20)

fill(basis, work, disposition, transp=65)

//JMA------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

jsa = (src0 + src0[lengths]) / 2

sig = src0 > jsa ? 1 : src0 < jsa ? -1 : 0

jsaColor = sig > 0 ? color.lime : sig < 0 ? color.red : color.orange

plot(jsa, color=jsaColor, linewidth=2)

jmagood = sig > 0

jmabad = sig < 0

//MACD------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

fast_ma = ema(src, fast_length)

slow_ma = ema(src, slow_length)

macd = fast_ma - slow_ma

signal = sma(macd, signal_length)

macdgood = macd > signal

macdbad = macd < signal

//Volume Delta -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

bullPower = iff(close < open, iff(close[1] < open, max(high - close[1], close - low), max(high - open, close - low)), iff(close > open, iff(close[1] > open, high - low, max(open - close[1], high - low)), iff(high - close > close - low, iff(close[1] < open, max(high - close[1], close - low), high - open), iff(high - close < close - low, iff(close[1] > open, high - low, max(open - close[1], high - low)), iff(close[1] > open, max(high - open, close - low), iff(close[1] < open, max(open - close[1], high - low), high-low))))))

bearPower = iff(close < open, iff(close[1] > open, max(close[1] - open, high - low), high - low), iff(close > open, iff(close[1] > open, max(close[1] - low, high - close), max(open - low, high - close)), iff(high - close > close - low, iff(close[1] > open, max(close[1] - open, high - low), high - low), iff(high - close < close - low, iff(close[1] > open, max(close[1] - low, high - close), open - low), iff(close[1] > open, max(close[1] - open, high - low), iff(close[1] < open, max(open - low, high - close), high - low))))))

bullVolume = (bullPower / (bullPower + bearPower)) * volume

bearVolume = (bearPower / (bullPower + bearPower)) * volume

delta = bullVolume - bearVolume

cvd = cum(delta)

cvdMa = sma(cvd, periodMa)

deltagood = cvd > cvdMa

deltabad = cvd < cvdMa

//Volume weight------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

getMA0(length) =>

maPrice = ema(volume, length)

if maType == "SMA"

maPrice := sma(volume, length)

if maType == "HMA"

maPrice := hma(volume, length)

if maType == "WMA"

maPrice := wma(volume, length)

if maType == "DEMA"

e1 = ema(volume, length)

e2 = ema(e1, length)

maPrice := 2 * e1 - e2

maPrice

ma = getMA0(maLength)

rvol = volume / ma

volumegood = volume > rvolTrigger * ma

//MA----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

ma5 = sma(close, 5)

ma10 = sma(close, 10)

ma30 = sma(close, 30)

magood = ma5 > ma30

mabad = ma5 < ma30

simplema = sma(src,length)

exponentialma = ema(src,length)

hullma = wma(2*wma(src, length/2)-wma(src, length), round(sqrt(length)))

weightedma = wma(src, length)

volweightedma = vwma(src, length)

avgval = matype==1 ? simplema : matype==2 ? exponentialma : matype==3 ? hullma : matype==4 ? weightedma : matype==5 ? volweightedma : na

MA_speed = (avgval / avgval[1] -1 ) *100

masgood = MA_speed > 0

masbad = MA_speed < 0

//Momentum-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

data = 0

for i = 1 to tmolength-1

if close > open[i]

data := data + 1

if close < open[i]

data := data - 1

EMA5 = ema(data, calcLength)

Main = ema(EMA5, smoothLength)

Signal = ema(Main, smoothLength)

momentumgood = Main > Signal

momentumbad = Main < Signal

//STRATEGY===============================================================================================================================================================================================================================================================

Long = (DIPlus > DIMinus and ADX > th) and volumegood and sargood and rsiob and macdgood and deltagood and magood and masgood and bullish and jmagood and rangegood and momentumgood

Short = (DIPlus < DIMinus and ADX > th) and volumegood and sarbad and rsios and macdbad and deltabad and mabad and masbad and jmabad and rangebad and momentumbad

//BACKTESTING==========================================================================================================================================================================================================================

// ————— Backtest input

Act_BT = input(true, title = "BACKTEST", type = input.bool)

backtest_time = input(180, title ="BACKTEST DAYS", type = input.integer, minval = 1)*24*60*60*1000

entry_Type = input("% EQUITY", title = "ENTRY TYPE", options = ["CONTRACTS","CASH","% EQUITY"])

et_Factor = (entry_Type == "CONTRACTS") ? 1 : (entry_Type == "% EQUITY") ? (100/(strategy.equity/close)) : close

//Signals----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

// SL AND TP-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

stopPer = input(3.6, title='Stop Loss % [plotshape]', type=input.float) / 100

takePer = input(0.8, title='Take Profit % [plotshape]', type=input.float) / 100

long_short = 0

long_last = Long and (nz(long_short[1]) == 0 or nz(long_short[1]) == -1)

short_last = Short and (nz(long_short[1]) == 0 or nz(long_short[1]) == 1)

long_short := long_last ? 1 : short_last ? -1 : long_short[1]

longPrice = valuewhen(long_last, close, 0)

shortPrice = valuewhen(short_last, close, 0)

longStop = longPrice * (1 - stopPer)

shortStop = shortPrice * (1 + stopPer)

longTake = longPrice * (1 + takePer)

shortTake = shortPrice * (1 - takePer)

//plot lines ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

plotshape(long_short==1 ? longTake : na, style=shape.cross, color=color.gray, location=location.absolute )

plotshape(long_short==-1 ? shortTake : na, style=shape.cross, color=color.gray, location=location.absolute )

longBar1 = barssince(long_last)

longBar2 = longBar1 >= 1 ? true : false

shortBar1 = barssince(short_last)

shortBar2 = shortBar1 >= 1 ? true : false

Long_SL = long_short==1 and longBar2 and low < longStop

Short_SL = long_short==-1 and shortBar2 and high > shortStop

Long_TP = long_short==1 and longBar2 and high > longTake

Short_TP = long_short==-1 and shortBar2 and low < shortTake

long_short := (long_short==1 or long_short==0) and longBar2 and (Long_SL or Long_TP) ? 0 : (long_short==-1 or long_short==0) and shortBar2 and (Short_SL or Short_TP) ? 0 : long_short

last_long_cond = Long and long_last

last_short_cond = Short and short_last

//plotshapes---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

plotshape(last_long_cond, title="Long x1", color=color.blue, style=shape.triangleup, location=location.belowbar, size=size.small, textcolor=color.white, text="Long" , transp=1)

plotshape(last_short_cond, title="Short x1", color=color.red, style=shape.triangledown, location=location.abovebar, size=size.tiny, textcolor=color.white, text="Short" ,transp=1)

plotshape(Long_SL, location=location.belowbar, color=color.black, size=size.tiny , text="SL", textcolor=color.fuchsia)

plotshape(Short_SL, location=location.abovebar, color=color.black, size=size.tiny , text="SL", textcolor=color.fuchsia)

plotshape(Long_TP,style=shape.triangledown, location=location.abovebar, color=color.gray, size=size.tiny , text="TP", textcolor=color.red)

plotshape(Short_TP,style=shape.triangleup, location=location.belowbar, color=color.gray, size=size.tiny , text="TP", textcolor=color.green)

if last_long_cond and Act_BT

strategy.entry("L", strategy.long)

if last_short_cond and Act_BT

strategy.entry("S", strategy.short)

per(pcnt) =>

strategy.position_size != 0 ? round(pcnt / 100 * strategy.position_avg_price / syminfo.mintick) : float(na)

stoploss=input(title=" stop loss [BT]", defval=3.6, minval=0.01)

los = per(stoploss)

q=input(title=" qty percent", defval=100, minval=1)

tp=input(title=" Take profit [BT]", defval=0.8, minval=0.01)

strategy.exit("tp", qty_percent = q, profit = per(tp), loss = los)

//By wielkieef

- Elliott-Wellen-Theorie 4-9 Impulswellen automatische Detektion Handelsstrategie

- Johnny's BOT

- VuManChu-Chiffer B + Divergenzstrategie

- Strategie für das Trendverfolgungsnetz der variablen Positionen

- Volumenbasierte dynamische DCA-Strategie

- TUE ADX/MACD Konfluenz V1.0

- Kombination von MACD und RSI für die langfristige Handelsstrategie

- Preisdivergenzstrategie v1.0

- Niedrigriskante, stabile Hochfrequenz-Handelsstrategie für Kryptowährungen auf Basis von RSI und MACD

- MACD RSI Ichimoku Momentum Trend nach langfristiger Strategie

- Super Scalper - 5 Minuten 15 Minuten

- Relativer Stärkeindex - Divergenzen - Freiheit

- Lineare Regression ++

- RedK Dual VADER mit Energiestangen

- Konsolidierungszonen - Live

- Quantitative Qualitative Schätzung

- Beweglicher Durchschnittsquerschnitt, mehrjährig (MTF)

- MACD-Reloaded-Strategie

- Supertrended gleitende Durchschnitte

- Handel mit ABC

- Shannon-Entropie V2

- Supertrend mit dem Trailing-Stopp-Verlust

- Volumenfluss v3

- Krypto-Futures-Stundenscalping mit ma & rsi - ogcheckers

- ATR ausgeglichen

- Bestellblock-Finder

- TrendScalp-FractalBox-3EMA ist ein

- QQE-Signale

- U-Bit-Gitterspannungsfilter

- CM MACD-Anzeiger - Mehrfacher Zeitrahmen - V2