Estrategia de cuatro elementos de seguimiento de tendencias

Resumen

Esta estrategia combina de manera integral cuatro elementos: el indicador SAR, el RSI, el indicador VOL y la media móvil MA para identificar tendencias, y adopta medidas de gestión de riesgos sólidas para seguir la tendencia y obtener ganancias. La estrategia utiliza el SAR como indicador principal, complementado con el RSI para identificar señales de reversión en zonas de sobrecompra y sobreventa, el VOL para determinar las características del volumen, y las medias móviles MA para juzgar la dirección de la tendencia principal y secundaria. La combinación de múltiples indicadores permite filtrar señales falsas e identificar la verdadera dirección de la tendencia. La gestión de riesgos establece stop loss y take profit, controlando eficazmente las pérdidas por operación y las ganancias acumuladas. Esta estrategia es adecuada para inversores de mediano y largo plazo, ya que puede alinearse con la tendencia principal y obtener rendimientos estables.

Principio de la Estrategia

Esta estrategia utiliza cuatro indicadores técnicos principales:

-

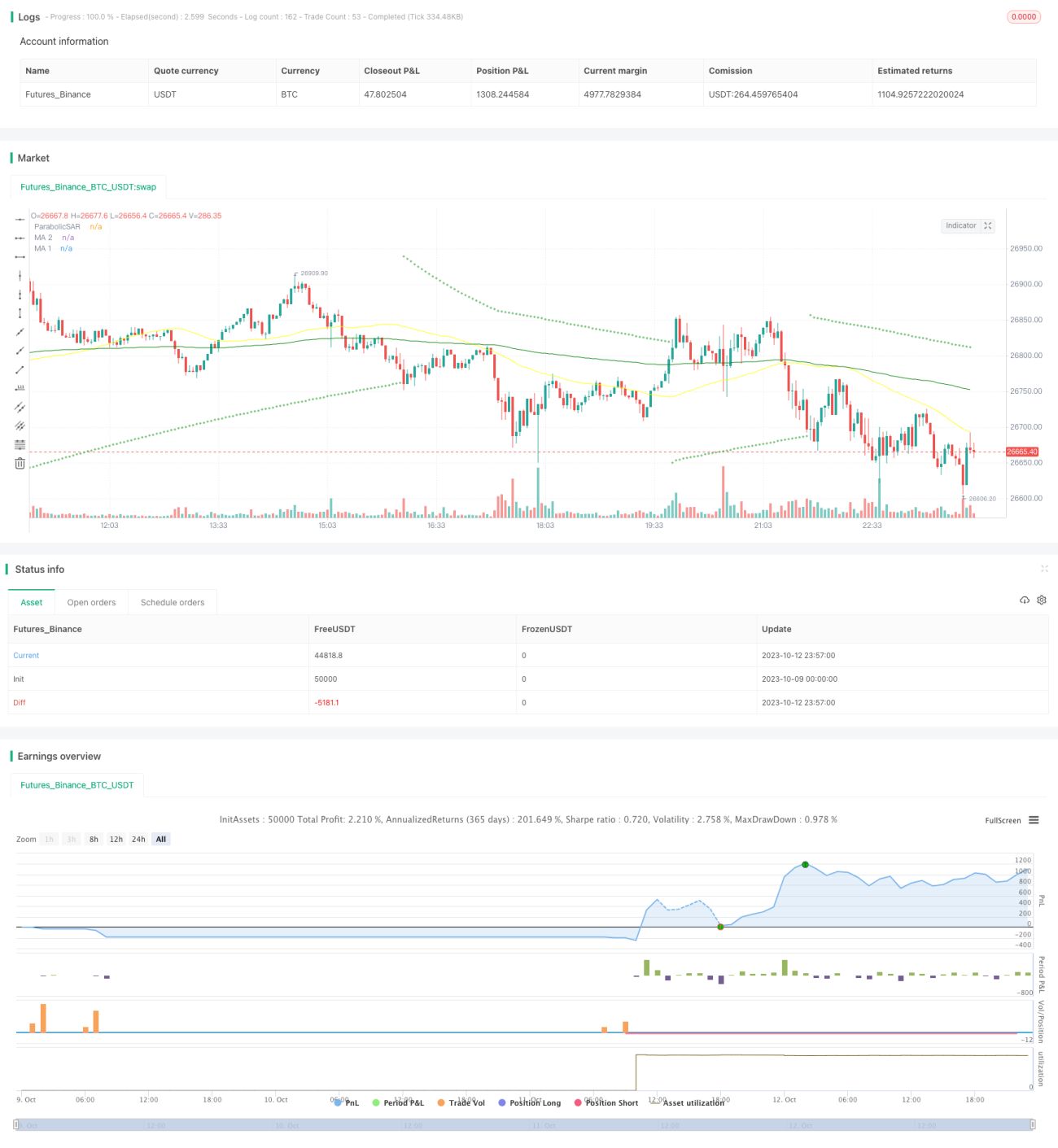

Parabolic SAR: Este indicador utiliza la relación entre los puntos y la tendencia para determinar la dirección y los puntos de reversión. Cuando los puntos están por encima del precio, es alcista; cuando están por debajo, es bajista. Cuando los puntos cruzan el precio, indica una reversión de la tendencia. La estrategia utiliza el SAR como indicador principal para determinar la dirección de la tendencia.

-

RSI (Índice de Fuerza Relativa): Este indicador oscila entre 0 y 100 para evaluar condiciones de sobrecompra o sobreventa. Un RSI superior a 70 indica sobrecompra, inferior a 30 indica sobreventa, y alrededor de 50 es la zona neutral. La estrategia utiliza el RSI para identificar señales de reversión por sobrecompra o sobreventa.

-

VOL (Volumen): La estrategia utiliza el volumen para confirmar la tendencia y evaluar la calidad de las señales de reversión mediante la detección de aumentos significativos en el volumen.

-

MA (Media Móvil): La estrategia emplea medias móviles de largo y corto plazo para determinar la dirección de la tendencia principal y secundaria. El cruce de la media móvil corta por encima de la larga es una señal alcista, y el cruce por debajo es una señal bajista.

Reglas de generación de señales de trading:

- Condición alcista: El punto SAR se sitúa por debajo de la vela, el RSI sube desde abajo hacia la zona neutral, el volumen aumenta significativamente y la media móvil corta cruza por encima de la media larga.

- Condición bajista: El punto SAR se sitúa por encima de la vela, el RSI baja desde arriba hacia la zona neutral, el volumen aumenta significativamente y la media móvil corta cruza por debajo de la media larga.

La estrategia también establece reglas de gestión de riesgos con take profit y stop loss. El objetivo de take profit es 2 veces el precio de entrada, y el stop loss es 0,8 veces el precio de entrada, bloqueando eficazmente las ganancias y controlando el riesgo.

Análisis de Ventajas

Esta estrategia presenta las siguientes ventajas:

- El diseño de múltiples indicadores combinados evita señales falsas y captura verdaderos puntos de inflexión de la tendencia.

- La gestión de riesgos con stop loss y take profit controla eficazmente el riesgo.

- La gestión de posición con entradas y salidas escalonadas maximiza las ganancias.

- Los parámetros han sido optimizados y probados repetidamente, garantizando su robustez.

- Datos de backtesting suficientes que simulan un entorno real de trading.

- La lógica de operación es clara y sencilla, fácil de entender e implementar.

Análisis de Riesgos

Esta estrategia también presenta los siguientes riesgos:

- Movimientos anormales del mercado que superen el stop loss. Se recomienda ajustar la distancia del stop loss adecuadamente.

- Falta de liquidez en el activo negociado que impida ejecutar el stop loss. Se deben seleccionar activos con buena liquidez.

- Riesgo sistémico que cause gaps anormales. Se debe reducir el apalancamiento y mantener activos con buen valor fundamental.

- Sobreoptimización de parámetros que resulte en curvas demasiado perfectas. Se deben relajar ligeramente los parámetros para mejorar la robustez.

- Costos de deslizamiento por alta frecuencia de trading. Se puede ampliar el intervalo entre señales de trading.

- Las señales pueden debilitarse y requerir actualizaciones periódicas. Se debe realizar backtesting regular y optimizar los parámetros.

Direcciones de Optimización

Esta estrategia puede optimizarse aún más en los siguientes aspectos:

- Probar más combinaciones de indicadores, como MACD, KD, etc., para encontrar una mejor correspondencia.

- Optimizar los períodos de las medias móviles MA para identificar más claramente las tendencias principales y secundarias.

- Optimizar los coeficientes de take profit y stop loss para obtener la mejor relación riesgo-beneficio.

- Probar la robustez de los parámetros en diferentes activos y encontrar la mejor combinación.

- Incorporar modelos de aprendizaje automático para ayudar a evaluar las señales de trading.

- Agregar algoritmos de stop loss adaptativos para que se ajusten mejor a la volatilidad real.

- Probar configuraciones de parámetros con plazos más largos y ampliar el rango de take profit.

Resumen

Esta estrategia combina múltiples indicadores para filtrar señales falsas y determinar la dirección de la tendencia, establece medidas de stop loss y take profit para controlar el riesgo, y mejora continuamente su efectividad a través de la optimización y el ajuste de parámetros. Aunque ninguna estrategia puede predecir perfectamente el futuro, un plan de trading sistemático junto con una buena gestión de riesgos aumentará significativamente la probabilidad de obtener ganancias. Esta estrategia ofrece un plan de seguimiento de tendencias relativamente sólido, adecuado para inversores racionales que buscan rendimientos estables a largo plazo.

- 1