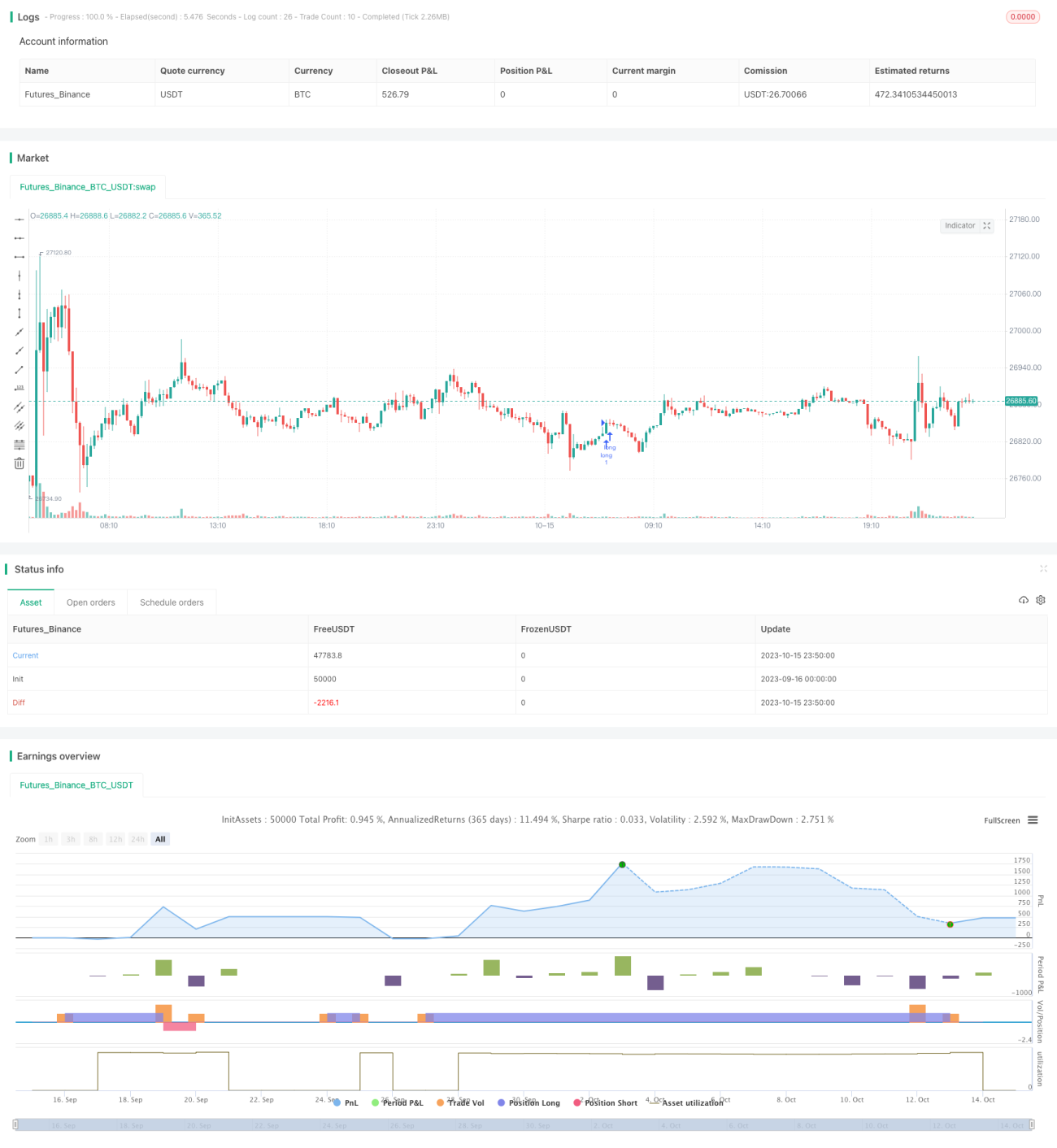

概要

本戦略は、MACD、RSI、PSARなどの複数のテクニカル指標と動的資金管理の原理を組み合わせ、マルチタイムフレームでのトレンド追従と逆張り取引を実現します。本戦略は短期的、中期的、長期的な取引に適用可能です。

原理

戦略ではPSAR指標を用いてトレンド方向を判断します。EMAの短期線と長期線がBB中央線と交差することを第1確認点とします。MACDヒストグラムの方向を第2確認点とします。RSIの買われ過ぎ・売られ過ぎ領域を第3確認点とします。これらの条件をすべて満たした場合に取引シグナルが発生します。

エントリー後はストップロスとテイクプロフィットを設定します。ストップロスはATR値の一定倍率で設定します。テイクプロフィットも同様です。また、含み損のパーセンテージによるストップロスも設定します。損失が口座総資産の一定割合に達した場合にストップロスで決済します。

含み益についてもパーセンテージ設定があります。利益が口座総資産の一定割合に達した場合に利確で決済します。

動的資金管理は、口座総資産、ATR、設定したストップロス倍率に基づいてポジションサイズを計算します。同時に最小取引量も設定します。

利点

-

複数要素による確認により、偽のブレイクアウトを回避し、エントリー精度が向上します。

-

動的資金管理により1回のリスクをコントロールし、口座を効果的に保護します。

-

ストップロス・テイクプロフィットをATRに基づいて設定するため、市場の変動幅に応じて調整可能です。

-

パーセンテージによる含み損・含み益の設定により、利益を確定し、利益の吐き出しを防ぎます。

リスク

-

複数要素の組み合わせにより、一部の取引機会を逃す可能性があります。

-

パーセンテージ設定が高すぎると、損失が拡大する恐れがあります。

-

ATRの数値設定が不適切だと、ストップロス・テイクプロフィットが緩すぎたり、積極的になりすぎたりする可能性があります。

-

資金管理の設定が不適切だと、1回のポジションサイズが大きくなりすぎる可能性があります。

最適化の方向性

-

エントリー要素の加重を調整し、シグナル精度を最適化します。

-

異なるパーセンテージパラメータ設定をテストし、最適な組み合わせを見つけます。

-

銘柄の特性に応じて適切なATR倍率を選択します。

-

バックテスト結果に基づき、資金管理パラメータを動的に調整します。

-

時間帯設定を最適化し、取引時間帯をテストします。

まとめ

本戦略は、複数のテクニカル指標を組み合わせてトレンドを判断し、動的資金管理を加えてリスクをコントロールすることで、マルチタイムフレームでの安定的な利益を実現します。バックテスト結果に基づき、要素の加重、リスク管理パラメータ、資金管理の設定をさらに最適化することで、より良い成果を得ることが期待できます。

- 1