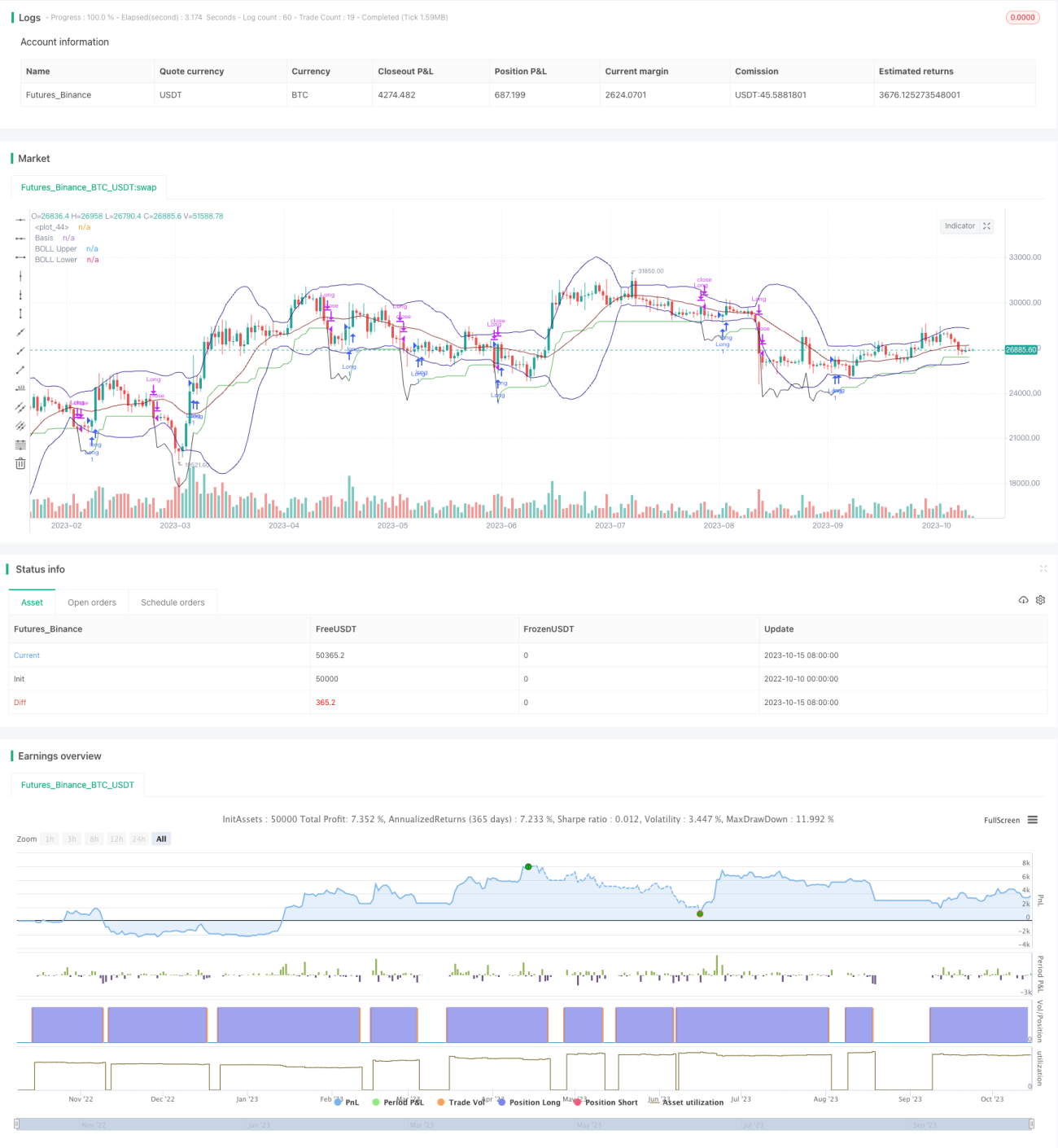

Relative Volume Trend Following Trading Strategy

Overview

This strategy combines relative volume indicator and price action trend judgment to build an automated trading system integrating trend following and breakout. It buys when volume increases and volatility is low, and sells based on stop loss and price action.

How It Works

-

Use Bollinger Bands to determine if price volatility is low. Specifically by comparing ATR and BOLL band width.

-

Calculate the average volume of past N days, compare with current volume to see if volume has increased.

-

Buy when price is near low, volume increases and volatility is low.

-

Set stop loss, track lowest price.

-

Sell when price breaks below stop loss.

-

Sell when price forms bullish engulfing pattern.

Advantages

-

Combining volume and volatility filters false breakout effectively.

-

Trailing stop loss locks in profit maximally.

-

Exit signals like bullish engulfing catch trend reversal early.

-

Intuitive and easy to follow.

-

Clear rules on stop loss and take profit reduce uncertainty.

Risks

-

Volume indicator lags, could miss best entry point.

-

Exit signals like engulfing lack reliability, risks early exit.

-

Wider stop risks larger loss on single trade.

-

Needs tuning of parameters like ATR period and volume period to avoid over trading.

-

Need to optimize exit rules to avoid unnecessary exit.

Enhancement Opportunities

-

Try additional filters like MACD to improve entry signals.

-

Optimize ATR and volume periods to reduce over trading.

-

Explore other exit signals like price breaking lower band.

-

Research trailing stop loss to lock in more profit.

-

Test different holding periods for best performance.

-

Backtest on different products to find the best fit.

Summary

The strategy is relatively simple, using volume and price action for trend following. It has clear signals and easy tracking. But the quality of filters and exit rules can be further improved for more reliable performance. With continued efforts on parameter tuning and entry/exit design, outstanding results could be achieved.

/*backtest

start: 2022-10-10 00:00:00

end: 2023-10-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © DojiEmoji (kevinhhl)

//@version=4- 1