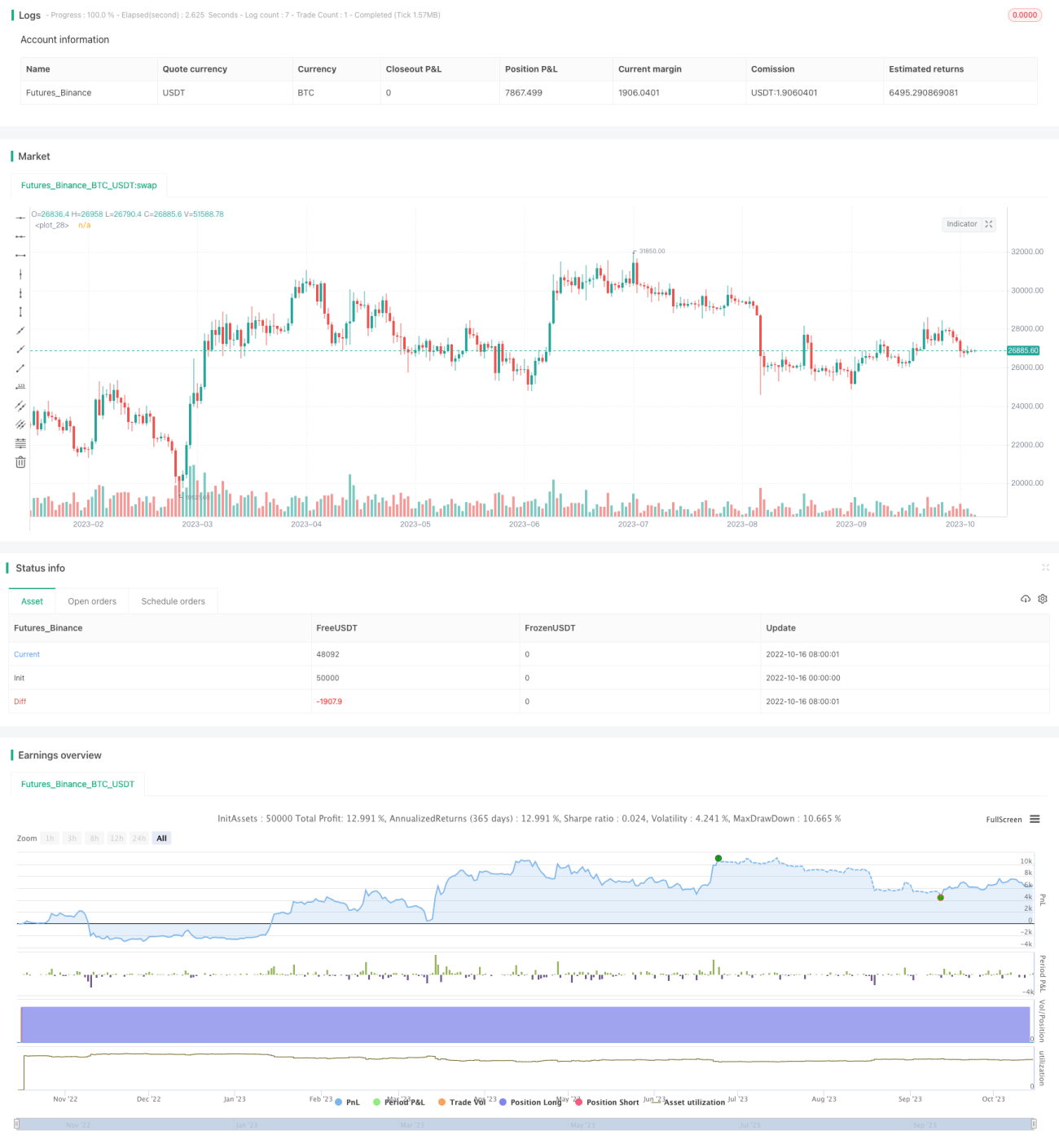

Mean Reversion Strategy Based on ATR

Overview

This strategy uses hypothesis testing to determine if ATR deviates from its mean value. Combined with prediction of price trend, it implements a mean reversion strategy based on ATR. Significant deviation of ATR indicates potential abnormal volatility in the market. If the price trend is predicted to be bullish, a long position can be established.

Strategy Logic

-

Hypothesis Testing

-

Conduct two-sample t-test between fast ATR period (atr_fast) and slow ATR period (atr_slow). Null hypothesis H0 is that there is no significant difference between the two sample means.

-

If test statistic exceeds threshold (confidence interval specified by reliability_factor), reject null hypothesis, i.e. fast ATR is considered to deviate significantly from slow ATR.

-

-

Price Trend Prediction

-

Moving average of logarithmic returns is calculated as expected drift rate (drift).

-

If drift is increasing, current trend is judged as bullish.

-

-

Entry and Stop Loss Exit

-

Go long when fast and slow ATR differs significantly and trend is bullish.

-

Continuously adjust stop loss using ATR. Exit position when price breaks below stop loss.

-

Advantage Analysis

-

Using hypothesis testing to determine ATR deviation is more scientific and adaptive.

-

Combining with price trend prediction avoids wrong trades based solely on ATR deviation.

-

Adjusting stop loss continually manages downside risk.

Risk Analysis

-

Unable to stop loss when price crashes.

-

Incorrect trend prediction may result in buying at the top.

-

Improper parameter settings may miss correct entry or add unnecessary trades.

Optimization Suggestions

-

Consider adding other indicators for multifactor confirmation to avoid mistakes.

-

Test different ATR parameter combinations to find more stable values.

-

Add criteria on breakthrough of key price levels to avoid false breakout.

Conclusion

The overall logic of this strategy is clear. Using hypothesis testing to detect abnormal volatility is reasonable. However, ATR deviation alone is insufficient to determine trend. More confirming factors are needed to improve accuracy. The stop loss rules are reliable but ineffective against cliff-style crashes. Future improvements can be made in areas like entry criteria, parameter selection, stop loss optimization.

- 1