概要

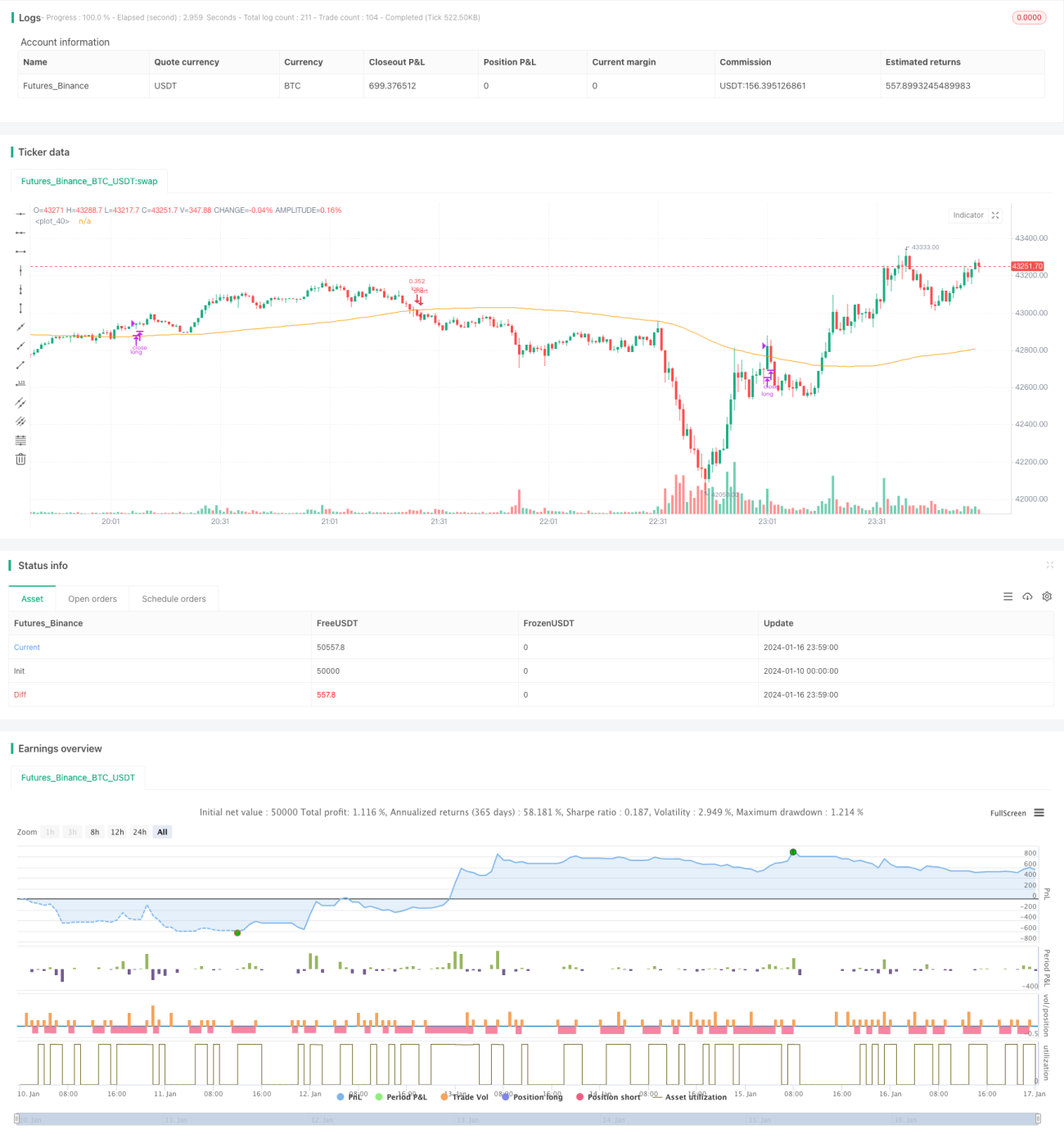

底割れリカバリー戦略は、典型的な安値買い高値売りの戦略です。RSIインジケーターを利用して売られ過ぎポイントを識別し、価格が一定の水準まで下落した際に買いシグナルを発して、より低い価格でトークンをAccumulate(蓄積)します。価格が再び上昇した際には、RSIの利確閾値を設定して利益確定を行います。この戦略は中長期の保有に適しており、レンジ相場における偽のブレイクアウトを効果的にフィルタリングし、保有コストの最適化を実現します。

戦略の原理

この戦略は主にRSIインジケーターを用いて売られ過ぎポイントを識別します。RSIインジケーターの標準範囲は0から100の間です。RSIが設定されたエントリー閾値である35未満に下落した場合、買いシグナルが発せられます。RSIが再度上昇し、設定された利確閾値である65以上になった場合、売りシグナルが発せられます。これにより、価格トレンドが反転するタイミングで適時エントリーおよびイグジットを行い、implementing(実装)安値買い高値売りを実現します。

また、戦略には100期間の単純移動平均線が導入され、RSIと組み合わせた条件が設定されています。価格が移動平均線を下回り、かつRSIが売られ過ぎ領域に入った場合にのみ買いシグナルが発動されます。これにより、一部の偽のブレイクアウトを効果的にフィルタリングし、不必要な取引を減らすことができます。

戦略の優位性

- RSIを活用して売られ過ぎ・買われ過ぎポイントを効果的に識別し、反転ポイントでエントリーすることで、より有利な買いコストを得られる

- 移動平均線と組み合わせて誤シグナルをフィルタリングし、高値追いを回避

- 中長期の保有に適しており、潜在的な上昇トレンドを掘り起こすことが可能

戦略のリスクと解決策

- 一定の遅延が存在し、急激な反転の機会を逃す可能性がある

- RSI計算期間を適宜短縮し、指標の反応を速める

- レンジ相場では多数の決済損失が発生する可能性がある

- 移動平均線の期間を調整するか、移動平均線を外す

- RSIエントリー・イグジットパラメータを適宜緩やかにする

戦略の最適化方向

- 異なる通貨ペアと時間枠のパラメータ最適化をテスト

- MACD、ボリンジャーバンドなどの他のインジケーターとの組み合わせを試行

- RSIパラメータまたは移動平均線パラメータを動的に調整

- ポジション管理戦略の最適化

まとめ

底割れリカバリー戦略は、全体的に堅実で実用的な安値買い高値売り戦略です。RSIと移動平均線による二重のフィルタリングにより、誤シグナルを効果的に抑制し、最適化されたパラメータの下で、より低い保有コストを得ることができます。同時に、インジケーターパラメータを適宜最適化し、ポジション戦略を調整することで、より高い資金効率が期待できます。

- 1