15 MIN BTCUSDTPERP BOT

Autora:ChaoZhang, Data: 23 de Maio de 2022Tags:ADXSARRSITWAPJMAMACD

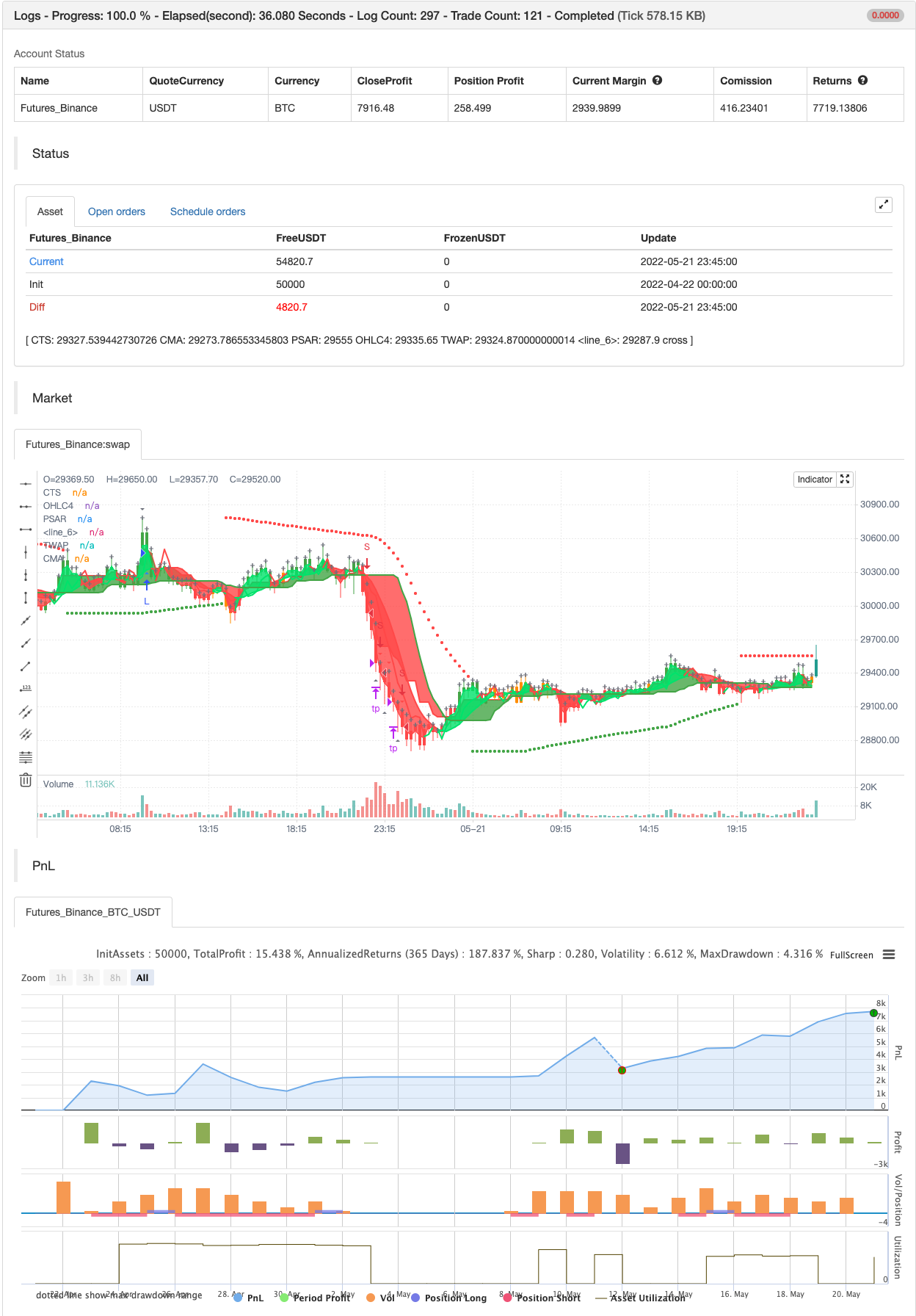

Este é o meu BTCUSDTPERP 15 min bot Os melhores resultados são no BTCUSDTPERP no binancefutures Os resultados dependem de indicadores de volume específicos que funcionam melhor no binancefutures

Os bots de 15 minutos são muito rápidos, é difícil encontrar uma boa configuração, por causa de 15 minutos de backtesting que pelo menos cerca de 3-4 meses.

Este bot é específico tem muito alta % de negócios lucrativos. lucro líquido também é muito bom. No entanto 15min bots são extremamente difícil de usar no longo prazo, então eu fiz como deflaut configurações como eu posso.

Então... Este bot usa 11 indicadores diferentes:

-

ADX

-

Filtro de intervalo

-

SAR

-

RSI

-

TWAP

-

JMA

-

MACD

-

VOLUME DELTA

-

Peso do volume

-

MA e o último para os melhores resultados nos gráficos qucik (15min) decidi acrescentar:

-

STOCH

-

ADX - - faz uma visão sólida para a tendência sem qualquer fraude: longo apenas em barras verdes, curtos apenas em barras vermelhas.

-

Filtro de intervalo - este indicador é para uma melhor visão das tendências, definir tendências, que é importante para todas as armadilhas touro/urso que ajuda muito por causa das tendências muito variáveis.

-

SAR - O SAR parabólico é um indicador técnico usado para determinar a direção do preço de um ativo, bem como chamar a atenção para quando a direção do preço está mudando.

-

O valor do RSI ajuda a estratégia a parar a negociação no momento certo.

-

TWAP - tem a mesma tarefa que o filtro Range, é apenas para melhor visualização de tendências, definir tendências.

-

JMA - O indicador Jurik Moving Average é uma das maneiras mais seguras de suavizar as curvas de preço dentro de um mínimo de atraso de tempo. O indicador oferece aos comerciantes de moeda um dos melhores filtros de preço durante fortes movimentos de preços. Neste momento, quando a ação do preço do bitcoin é tão forte, este indicador é necessário.

-

O MACD - Moving Average Convergence Divergence (MACD) é um indicador de momento que mostra a relação entre duas médias móveis do preço de um título. Hoje em dia, o MACD, tal como a JMA, é necessário para fazer um bot lucrativo.

-

Volume Delta - Uma abordagem cumulativa de Volume Delta baseada no Indicador de Balanço de Touro e Urso de Vadim Gimelfarb publicado na edição de Outubro de 2003 da revista S&C. Ajuste o comprimento da média móvel de acordo com as suas necessidades (símbolo, prazo, etc.)

-

Volume Weight - é o indicador mais importante para a estratégia, para evitar negociações abertas em gráfico plano, novas negociações são abertas após um volume forte barras.

-

MA 5-10-30 - como os anteriores este é para uma melhor visão das tendências, e definir corretamente as tendências, também Speed_MA estão usando para prever a ação futura do preço.

-

O stochastic-stock é útil para prever inversões de tendência.

Aproveita.

backtest

/*backtest

start: 2022-05-20 00:00:00

end: 2022-06-18 23:59:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © wielkieef

//@version=4

strategy("15MIN BTCUSDTPERP BOT", overlay=true, pyramiding=1,initial_capital = 10000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0)

//SOURCE ==================================================================================================================================================================================================================================================================

src = input(ohlc4)

// INPUTS ==================================================================================================================================================================================================================================================================

//ADX -------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Act_ADX = input(true, title = "AVERAGE DIRECTIONAL INDEX", type = input.bool)

ADX_options = input("MASANAKAMURA", title = "ADX OPTION", options = ["CLASSIC", "MASANAKAMURA"])

ADX_len = input(11, title = "ADX LENGTH", type = input.integer, minval = 1)

th = input(12, title = "ADX THRESHOLD", type = input.float, minval = 0, step = 0.5)

//Range Filter----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

length0 = input(13, title="Range Filter lenght"),mult = input(1, title="Range Filter mult")

//SAR-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

start = input(title="SAR Start", type=input.float, step=0.001, defval=0)

increment = input(title="SAR Increment", type=input.float, step=0.001, defval=0.006)

maximum = input(title="SAR Maximum", type=input.float, step=0.01, defval=1)

width = input(title="SAR Point Width", type=input.integer, minval=1, defval=1)

//RSI---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

len_3 = input(70, minval=1, title="RSI lenght")

src_3 = input(close, "RSI Source")

//TWAP Trend --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

smoothing = input(title="TWAP Smoothing", defval= 10)

resolution = input("0", "TWAP Timeframe")

//JMA------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

inp = input(title="JMA Source", type=input.source, defval=close)

reso = input(title="JMA Resolution", type=input.resolution, defval="")

rep = input(title="JMA Allow Repainting?", type=input.bool, defval=false)

src0 = security(syminfo.tickerid, reso, inp[rep ? 0 : barstate.isrealtime ? 1 : 0])[rep ? 0 : barstate.isrealtime ? 0 : 1]

lengths = input(title="JMA Length", type=input.integer, defval=4, minval=1)

//MACD------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

fast_length = input(title="MACD Fast Length", type=input.integer, defval=25)

slow_length = input(title="MACD Slow Length", type=input.integer, defval=50)

signal_length = input(title="MACD Signal Smoothing", type=input.integer, minval = 1, maxval = 50, defval = 9)

//Volume Delta -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

periodMa = input(title="Delta Length", minval=1, defval=45)

//Volume weight------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

maLength = input(title="Volume Weight Length", type=input.integer, defval=100, minval=1)

maType = input(title="Volume Weight Type", type=input.string, defval="SMA", options=["EMA", "SMA", "HMA", "WMA", "DEMA"])

rvolTrigger = input(title="Volume To Trigger Signal", type=input.float, defval=1.5, step=0.1 , minval=0.1)

//MA----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

length = input(51, minval=1, title="MA Length")

matype = input(5, minval=1, maxval=5, title="AvgType")

//Momentum------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

tmolength = input(45, title="Momentum Length")

calcLength = input(12, title="Momentum Calc length")

smoothLength = input(9, title="Momentum Smooth length")

//INDICATORS ==============================================================================================================================================================================================================================================================

//ADX----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

calcADX(_len) =>

up = change(high)

down = -change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

truerange = rma(tr, _len)

_plus = fixnan(100 * rma(plusDM, _len) / truerange)

_minus = fixnan(100 * rma(minusDM, _len) / truerange)

sum = _plus + _minus

_adx = 100 * rma(abs(_plus - _minus) / (sum == 0 ? 1 : sum), _len)

[_plus,_minus,_adx]

calcADX_Masanakamura(_len) =>

SmoothedTrueRange = 0.0

SmoothedDirectionalMovementPlus = 0.0

SmoothedDirectionalMovementMinus = 0.0

TrueRange = max(max(high - low, abs(high - nz(close[1]))), abs(low - nz(close[1])))

DirectionalMovementPlus = high - nz(high[1]) > nz(low[1]) - low ? max(high - nz(high[1]), 0) : 0

DirectionalMovementMinus = nz(low[1]) - low > high - nz(high[1]) ? max(nz(low[1]) - low, 0) : 0

SmoothedTrueRange := nz(SmoothedTrueRange[1]) - (nz(SmoothedTrueRange[1]) /_len) + TrueRange

SmoothedDirectionalMovementPlus := nz(SmoothedDirectionalMovementPlus[1]) - (nz(SmoothedDirectionalMovementPlus[1]) / _len) + DirectionalMovementPlus

SmoothedDirectionalMovementMinus := nz(SmoothedDirectionalMovementMinus[1]) - (nz(SmoothedDirectionalMovementMinus[1]) / _len) + DirectionalMovementMinus

DIP = SmoothedDirectionalMovementPlus / SmoothedTrueRange * 100

DIM = SmoothedDirectionalMovementMinus / SmoothedTrueRange * 100

DX = abs(DIP-DIM) / (DIP+DIM)*100

adx = sma(DX, _len)

[DIP,DIM,adx]

[DIPlusC,DIMinusC,ADXC] = calcADX(ADX_len)

[DIPlusM,DIMinusM,ADXM] = calcADX_Masanakamura(ADX_len)

DIPlus = ADX_options == "CLASSIC" ? DIPlusC : DIPlusM

DIMinus = ADX_options == "CLASSIC" ? DIMinusC : DIMinusM

ADX = ADX_options == "CLASSIC" ? ADXC : ADXM

ADX_color = DIPlus > DIMinus and ADX > th ? color.green : DIPlus < DIMinus and ADX > th ? color.red : color.orange

barcolor(color = Act_ADX ? ADX_color : na, title = "ADX")

//Range Filter---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

out = 0., cma = 0., cts = 0.

Var = variance(src,length0)*mult

sma = sma(src,length0)

secma = pow(nz(sma - cma[1]),2)

sects = pow(nz(src - cts[1]),2)

ka = Var < secma ? 1 - Var/secma : 0

kb = Var < sects ? 1 - Var/sects : 0

cma := ka*sma+(1-ka)*nz(cma[1],src)

cts := kb*src+(1-kb)*nz(cts[1],src)

css = cts > cma ? color.green : color.red

a = plot(cts,"CTS",color.red,2,transp=0)

b = plot(cma,"CMA",color.green,2,transp=0)

fill(a,b,color=css,transp=80)

rangegood = cts > cma

rangebad = cts < cma

//SAR-------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

psar = sar(start, increment, maximum)

dir = psar < close ? 1 : -1

psarColor = dir == 1 ? color.green : color.red

psarPlot = plot(psar, title="PSAR", style=plot.style_circles, linewidth=width, color=psarColor, transp=0)

var color longColor = color.green

var color shortColor = color.red

sargood = dir ==1

sarbad = dir ==-1

//RSI---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

up_3 = rma(max(change(src_3), 0), len_3)

down_3 = rma(-min(change(src_3), 0), len_3)

rsi_3 = down_3 == 0 ? 100 : up_3 == 0 ? 0 : 100 - (100 / (1 + up_3 / down_3))

rsiob = (rsi_3 < 70)

rsios = (rsi_3 > 30)

//TWAP Trend --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

res = resolution != "0" ? resolution : timeframe.period

weight = barssince(change(security(syminfo.tickerid, res, time, lookahead=barmerge.lookahead_on)))

price = 0.

price:= weight == 0 ? src : src + nz(price[1])

twap = price / (weight + 1)

ma_ = smoothing < 2 ? twap : sma(twap, smoothing)

bullish = iff(smoothing < 2, src >= ma_, src > ma_)

disposition = bullish ? color.lime : color.red

basis = plot(src, "OHLC4", disposition, linewidth=1, transp=100)

work = plot(ma_, "TWAP", disposition, linewidth=2, transp=20)

fill(basis, work, disposition, transp=65)

//JMA------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

jsa = (src0 + src0[lengths]) / 2

sig = src0 > jsa ? 1 : src0 < jsa ? -1 : 0

jsaColor = sig > 0 ? color.lime : sig < 0 ? color.red : color.orange

plot(jsa, color=jsaColor, linewidth=2)

jmagood = sig > 0

jmabad = sig < 0

//MACD------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

fast_ma = ema(src, fast_length)

slow_ma = ema(src, slow_length)

macd = fast_ma - slow_ma

signal = sma(macd, signal_length)

macdgood = macd > signal

macdbad = macd < signal

//Volume Delta -----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

bullPower = iff(close < open, iff(close[1] < open, max(high - close[1], close - low), max(high - open, close - low)), iff(close > open, iff(close[1] > open, high - low, max(open - close[1], high - low)), iff(high - close > close - low, iff(close[1] < open, max(high - close[1], close - low), high - open), iff(high - close < close - low, iff(close[1] > open, high - low, max(open - close[1], high - low)), iff(close[1] > open, max(high - open, close - low), iff(close[1] < open, max(open - close[1], high - low), high-low))))))

bearPower = iff(close < open, iff(close[1] > open, max(close[1] - open, high - low), high - low), iff(close > open, iff(close[1] > open, max(close[1] - low, high - close), max(open - low, high - close)), iff(high - close > close - low, iff(close[1] > open, max(close[1] - open, high - low), high - low), iff(high - close < close - low, iff(close[1] > open, max(close[1] - low, high - close), open - low), iff(close[1] > open, max(close[1] - open, high - low), iff(close[1] < open, max(open - low, high - close), high - low))))))

bullVolume = (bullPower / (bullPower + bearPower)) * volume

bearVolume = (bearPower / (bullPower + bearPower)) * volume

delta = bullVolume - bearVolume

cvd = cum(delta)

cvdMa = sma(cvd, periodMa)

deltagood = cvd > cvdMa

deltabad = cvd < cvdMa

//Volume weight------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

getMA0(length) =>

maPrice = ema(volume, length)

if maType == "SMA"

maPrice := sma(volume, length)

if maType == "HMA"

maPrice := hma(volume, length)

if maType == "WMA"

maPrice := wma(volume, length)

if maType == "DEMA"

e1 = ema(volume, length)

e2 = ema(e1, length)

maPrice := 2 * e1 - e2

maPrice

ma = getMA0(maLength)

rvol = volume / ma

volumegood = volume > rvolTrigger * ma

//MA----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

ma5 = sma(close, 5)

ma10 = sma(close, 10)

ma30 = sma(close, 30)

magood = ma5 > ma30

mabad = ma5 < ma30

simplema = sma(src,length)

exponentialma = ema(src,length)

hullma = wma(2*wma(src, length/2)-wma(src, length), round(sqrt(length)))

weightedma = wma(src, length)

volweightedma = vwma(src, length)

avgval = matype==1 ? simplema : matype==2 ? exponentialma : matype==3 ? hullma : matype==4 ? weightedma : matype==5 ? volweightedma : na

MA_speed = (avgval / avgval[1] -1 ) *100

masgood = MA_speed > 0

masbad = MA_speed < 0

//Momentum-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

data = 0

for i = 1 to tmolength-1

if close > open[i]

data := data + 1

if close < open[i]

data := data - 1

EMA5 = ema(data, calcLength)

Main = ema(EMA5, smoothLength)

Signal = ema(Main, smoothLength)

momentumgood = Main > Signal

momentumbad = Main < Signal

//STRATEGY===============================================================================================================================================================================================================================================================

Long = (DIPlus > DIMinus and ADX > th) and volumegood and sargood and rsiob and macdgood and deltagood and magood and masgood and bullish and jmagood and rangegood and momentumgood

Short = (DIPlus < DIMinus and ADX > th) and volumegood and sarbad and rsios and macdbad and deltabad and mabad and masbad and jmabad and rangebad and momentumbad

//BACKTESTING==========================================================================================================================================================================================================================

// ————— Backtest input

Act_BT = input(true, title = "BACKTEST", type = input.bool)

backtest_time = input(180, title ="BACKTEST DAYS", type = input.integer, minval = 1)*24*60*60*1000

entry_Type = input("% EQUITY", title = "ENTRY TYPE", options = ["CONTRACTS","CASH","% EQUITY"])

et_Factor = (entry_Type == "CONTRACTS") ? 1 : (entry_Type == "% EQUITY") ? (100/(strategy.equity/close)) : close

//Signals----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

// SL AND TP-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

stopPer = input(3.6, title='Stop Loss % [plotshape]', type=input.float) / 100

takePer = input(0.8, title='Take Profit % [plotshape]', type=input.float) / 100

long_short = 0

long_last = Long and (nz(long_short[1]) == 0 or nz(long_short[1]) == -1)

short_last = Short and (nz(long_short[1]) == 0 or nz(long_short[1]) == 1)

long_short := long_last ? 1 : short_last ? -1 : long_short[1]

longPrice = valuewhen(long_last, close, 0)

shortPrice = valuewhen(short_last, close, 0)

longStop = longPrice * (1 - stopPer)

shortStop = shortPrice * (1 + stopPer)

longTake = longPrice * (1 + takePer)

shortTake = shortPrice * (1 - takePer)

//plot lines ---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

plotshape(long_short==1 ? longTake : na, style=shape.cross, color=color.gray, location=location.absolute )

plotshape(long_short==-1 ? shortTake : na, style=shape.cross, color=color.gray, location=location.absolute )

longBar1 = barssince(long_last)

longBar2 = longBar1 >= 1 ? true : false

shortBar1 = barssince(short_last)

shortBar2 = shortBar1 >= 1 ? true : false

Long_SL = long_short==1 and longBar2 and low < longStop

Short_SL = long_short==-1 and shortBar2 and high > shortStop

Long_TP = long_short==1 and longBar2 and high > longTake

Short_TP = long_short==-1 and shortBar2 and low < shortTake

long_short := (long_short==1 or long_short==0) and longBar2 and (Long_SL or Long_TP) ? 0 : (long_short==-1 or long_short==0) and shortBar2 and (Short_SL or Short_TP) ? 0 : long_short

last_long_cond = Long and long_last

last_short_cond = Short and short_last

//plotshapes---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

plotshape(last_long_cond, title="Long x1", color=color.blue, style=shape.triangleup, location=location.belowbar, size=size.small, textcolor=color.white, text="Long" , transp=1)

plotshape(last_short_cond, title="Short x1", color=color.red, style=shape.triangledown, location=location.abovebar, size=size.tiny, textcolor=color.white, text="Short" ,transp=1)

plotshape(Long_SL, location=location.belowbar, color=color.black, size=size.tiny , text="SL", textcolor=color.fuchsia)

plotshape(Short_SL, location=location.abovebar, color=color.black, size=size.tiny , text="SL", textcolor=color.fuchsia)

plotshape(Long_TP,style=shape.triangledown, location=location.abovebar, color=color.gray, size=size.tiny , text="TP", textcolor=color.red)

plotshape(Short_TP,style=shape.triangleup, location=location.belowbar, color=color.gray, size=size.tiny , text="TP", textcolor=color.green)

if last_long_cond and Act_BT

strategy.entry("L", strategy.long)

if last_short_cond and Act_BT

strategy.entry("S", strategy.short)

per(pcnt) =>

strategy.position_size != 0 ? round(pcnt / 100 * strategy.position_avg_price / syminfo.mintick) : float(na)

stoploss=input(title=" stop loss [BT]", defval=3.6, minval=0.01)

los = per(stoploss)

q=input(title=" qty percent", defval=100, minval=1)

tp=input(title=" Take profit [BT]", defval=0.8, minval=0.01)

strategy.exit("tp", qty_percent = q, profit = per(tp), loss = los)

//By wielkieef

- Teoria da onda de Elliott 4-9 Detecção automática de onda de impulso Estratégia de negociação

- O BOT do Johnny.

- VuManChu Cipher B + Divergências Estratégia

- Estratégia de rede de posições variáveis baseada na tendência

- Estratégia dinâmica de DCA baseada no volume

- TUE ADX/MACD Confluência V1.0

- Estratégia de negociação combinada de longo prazo do MACD e do RSI

- Estratégia de divergência de preços v1.0

- Estratégia de negociação de alta frequência de criptomoedas estável de baixo risco baseada no RSI e no MACD

- MACD RSI Ichimoku Tendência de Impulso Seguindo Estratégia Longa

- Super Scalper - 5 Min 15 Min

- Índice de Força Relativa - Divergências - Libertus

- Regressão linear ++

- RedK Dual VADER com barras de energia

- Zonas de consolidação - ao vivo

- Estimativa quantitativa

- Alerta cruzada média móvel, multi-tempo (MTF)

- Estratégia de recarga do MACD

- Média móvel supertrendada

- Comércio ABC

- Entropia de Shannon V2

- Supertrend ATR COM TRAILING STOP LOSS

- Fluxo de volume v3

- Scalping horário de futuros de criptomoedas com ma & rsi - ogcheckers

- ATR suavizado

- Buscador de blocos de ordem

- TendênciaScalp-FractalBox-3EMA

- Sinais QQE

- Filtragem de amplitude de grelha de bits U

- Indicador MACD personalizado CM - Quadro de tempo múltiplo - V2