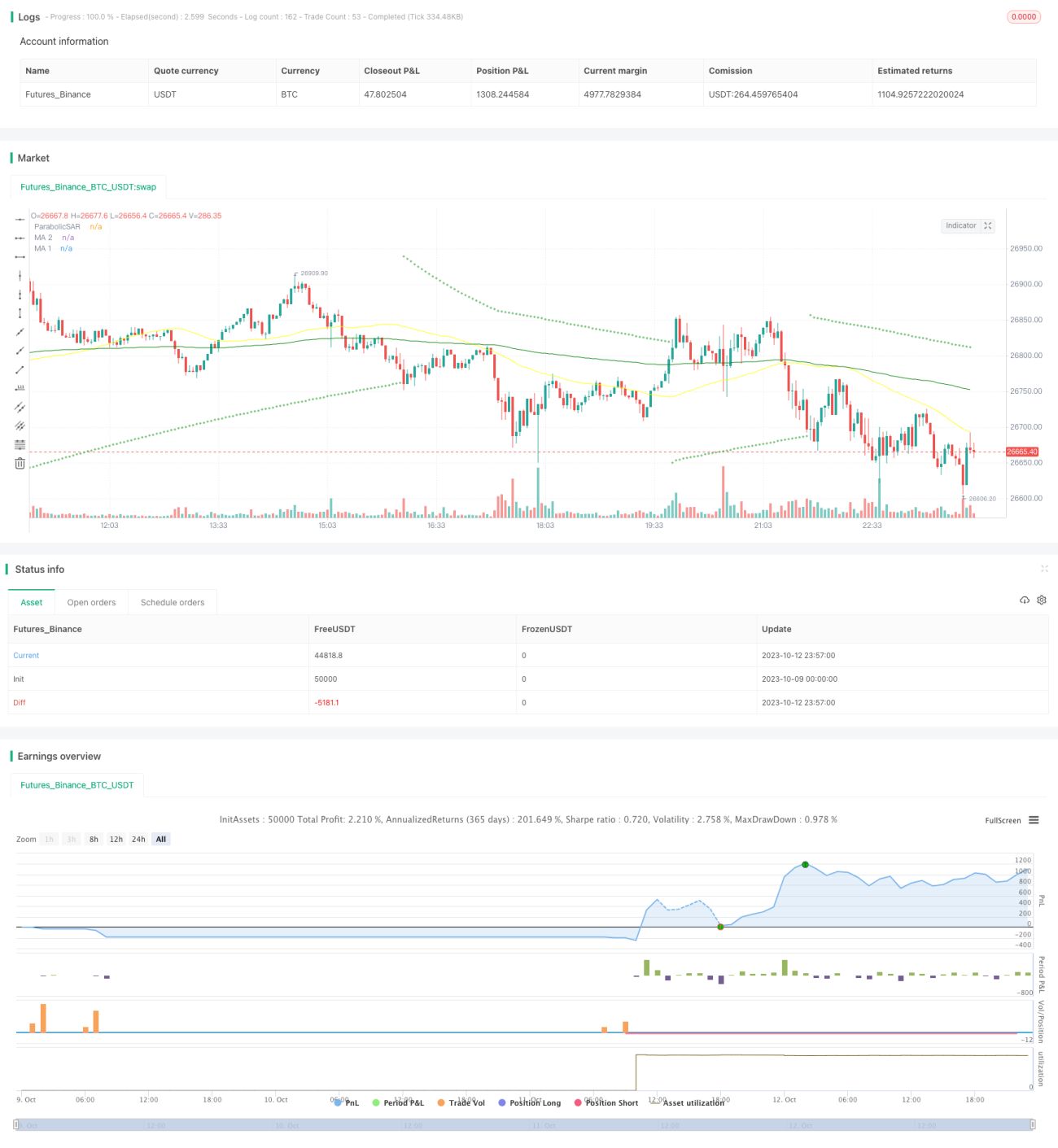

Chiến lược bốn yếu tố theo xu hướng

Tổng quan

Chiến lược này kết hợp toàn diện bốn yếu tố: chỉ số SAR, chỉ số RSI, chỉ số VOL và đường trung bình MA để nhận diện xu hướng, áp dụng các biện pháp quản lý rủi ro vững chắc nhằm theo dõi xu hướng và thu lợi nhuận. Chiến lược lấy chỉ số SAR làm chủ đạo, kết hợp với RSI xác định ranh giới quá mua/quá bán để nhận diện tín hiệu đảo chiều, chỉ số VOL đánh giá đặc điểm khối lượng giao dịch, MA xác định hướng xu hướng chính và phụ. Sự kết hợp của nhiều chỉ số giúp lọc nhiễu, nhận diện hướng xu hướng thực sự. Quản lý rủi ro thiết lập cắt lỗ và chốt lời, kiểm soát hiệu quả thua lỗ từng lệnh và lợi nhuận tích lũy. Chiến lược này phù hợp với nhà đầu tư nắm giữ trung và dài hạn, có thể thu được lợi nhuận ổn định theo xu hướng chính.

Nguyên lý chiến lược

Chiến lược này sử dụng 4 chỉ báo kỹ thuật chính:

-

Parabolic SAR: Chỉ báo này sử dụng mối quan hệ giữa các chấm và xu hướng để xác định hướng xu hướng và điểm đảo chiều. Khi chấm nằm trên giá là tín hiệu tăng, khi chấm nằm dưới giá là tín hiệu giảm. Khi chấm xuyên qua giá thể hiện sự đảo chiều xu hướng. Chiến lược sử dụng SAR làm chỉ báo chính để xác định hướng xu hướng.

-

RSI: Chỉ số sức mạnh tương đối. Chỉ báo này dao động trong khoảng 0-100 để đánh giá tình trạng quá mua/quá bán của thị trường. RSI trên 70 là vùng quá mua, dưới 30 là vùng quá bán, trở về gần 50 là vùng trung tính. Chiến lược sử dụng RSI để nhận diện tín hiệu đảo chiều quá mua/quá bán.

-

VOL: Chỉ số khối lượng giao dịch. Chiến lược sử dụng VOL để xác định đặc điểm gia tăng khối lượng nhằm xác nhận xu hướng và đánh giá chất lượng tín hiệu đảo chiều.

-

MA: Đường trung bình động. Chiến lược sử dụng đường trung bình ngắn hạn và dài hạn để xác định hướng xu hướng chính và phụ. Đường ngắn hạn cắt lên trên đường dài hạn là tín hiệu tăng, đường ngắn hạn cắt xuống dưới đường dài hạn là tín hiệu giảm.

Quy tắc tạo tín hiệu giao dịch:

- Điều kiện mua: Chấm SAR chuyển xuống dưới nến và RSI từ dưới đi lên vào vùng trung tính, khối lượng VOL gia tăng rõ rệt, đường trung bình ngắn hạn cắt lên trên đường trung bình dài hạn.

- Điều kiện bán: Chấm SAR chuyển lên trên nến và RSI từ trên đi xuống vào vùng trung tính, khối lượng VOL gia tăng rõ rệt, đường trung bình ngắn hạn cắt xuống dưới đường trung bình dài hạn.

Chiến lược này cũng thiết lập quy tắc quản lý rủi ro chốt lời và cắt lỗ. Mục tiêu chốt lời là gấp 2 lần giá vào lệnh, giá cắt lỗ là 0,8 lần giá vào lệnh, giúp khóa lợi nhuận và kiểm soát rủi ro hiệu quả.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Thiết kế kết hợp nhiều chỉ báo tránh tín hiệu giả, thực sự bắt được các điểm đảo chiều xu hướng.

- Quản lý rủi ro thiết lập cắt lỗ và chốt lời, kiểm soát rủi ro hiệu quả.

- Quản lý vị thế vào lệnh nhiều đợt và chốt lời nhiều đợt, tối đa hóa lợi nhuận.

- Các tham số đã được tối ưu hóa và kiểm tra nhiều lần, đảm bảo tính vững chắc.

- Dữ liệu backtest đầy đủ, mô phỏng môi trường giao dịch thực tế.

- Logic vận hành rõ ràng, đơn giản, dễ hiểu và dễ thực hiện.

Phân tích rủi ro

Chiến lược này cũng tồn tại những rủi ro sau:

- Biến động bất thường của thị trường dẫn đến cắt lỗ bị phá vỡ. Khuyến nghị nới rộng khoảng cách cắt lỗ phù hợp.

- Tính thanh khoản của sản phẩm giao dịch thấp dẫn đến không thể cắt lỗ. Nên chọn các sản phẩm giao dịch có tính thanh khoản cao.

- Rủi ro hệ thống dẫn đến gap giá bất thường. Nên giảm đòn bẩy và nắm giữ các tài sản có nền tảng giá trị tốt.

- Tối ưu hóa tham số quá mức khiến đường cong quá đẹp. Nên giảm nhẹ tham số để tăng tính vững chắc.

- Chi phí trượt giá do tần suất giao dịch quá cao. Có thể nới rộng khoảng cách tạo tín hiệu giao dịch.

- Hiệu quả tín hiệu suy yếu cần cập nhật kịp thời. Nên thường xuyên backtest và tối ưu hóa cài đặt tham số.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa thêm từ các khía cạnh sau:

- Thử nghiệm thêm nhiều tổ hợp chỉ báo, như MACD, KD, v.v. để tìm sự kết hợp tốt hơn.

- Tối ưu hóa cài đặt chu kỳ MA để nhận diện xu hướng chính và phụ rõ ràng hơn.

- Tối ưu hóa hệ số chốt lời và cắt lỗ để đạt tỷ lệ lợi nhuận/rủi ro tốt nhất.

- Kiểm tra độ vững chắc của tham số trên các sản phẩm khác nhau và tìm tổ hợp tham số tối ưu.

- Thêm mô hình học máy hỗ trợ đánh giá tín hiệu giao dịch.

- Thêm thuật toán cắt lỗ thích ứng, giúp cắt lỗ sát với biến động thực tế.

- Thử nghiệm cài đặt chu kỳ dài hơn, mở rộng phạm vi chốt lời.

Tổng kết

Chiến lược này kết hợp toàn diện nhiều chỉ báo để lọc tín hiệu giả, xác định hướng xu hướng, thiết lập các biện pháp cắt lỗ và chốt lời để kiểm soát rủi ro, thông qua tối ưu hóa tham số và điều chỉnh tổ hợp không ngừng nâng cao hiệu quả chiến lược. Mặc dù không có chiến lược nào có thể dự đoán hoàn hảo tương lai, nhưng một kế hoạch giao dịch có hệ thống kết hợp với quản lý rủi ro tốt sẽ cải thiện đáng kể xác suất sinh lời. Chiến lược này cung cấp một giải pháp theo dõi xu hướng tương đối vững chắc, phù hợp với các nhà đầu tư lý trí theo đuổi lợi nhuận ổn định dài hạn.

- 1