Chiến lược quản lý vốn động đa nhân tố

Tổng quan

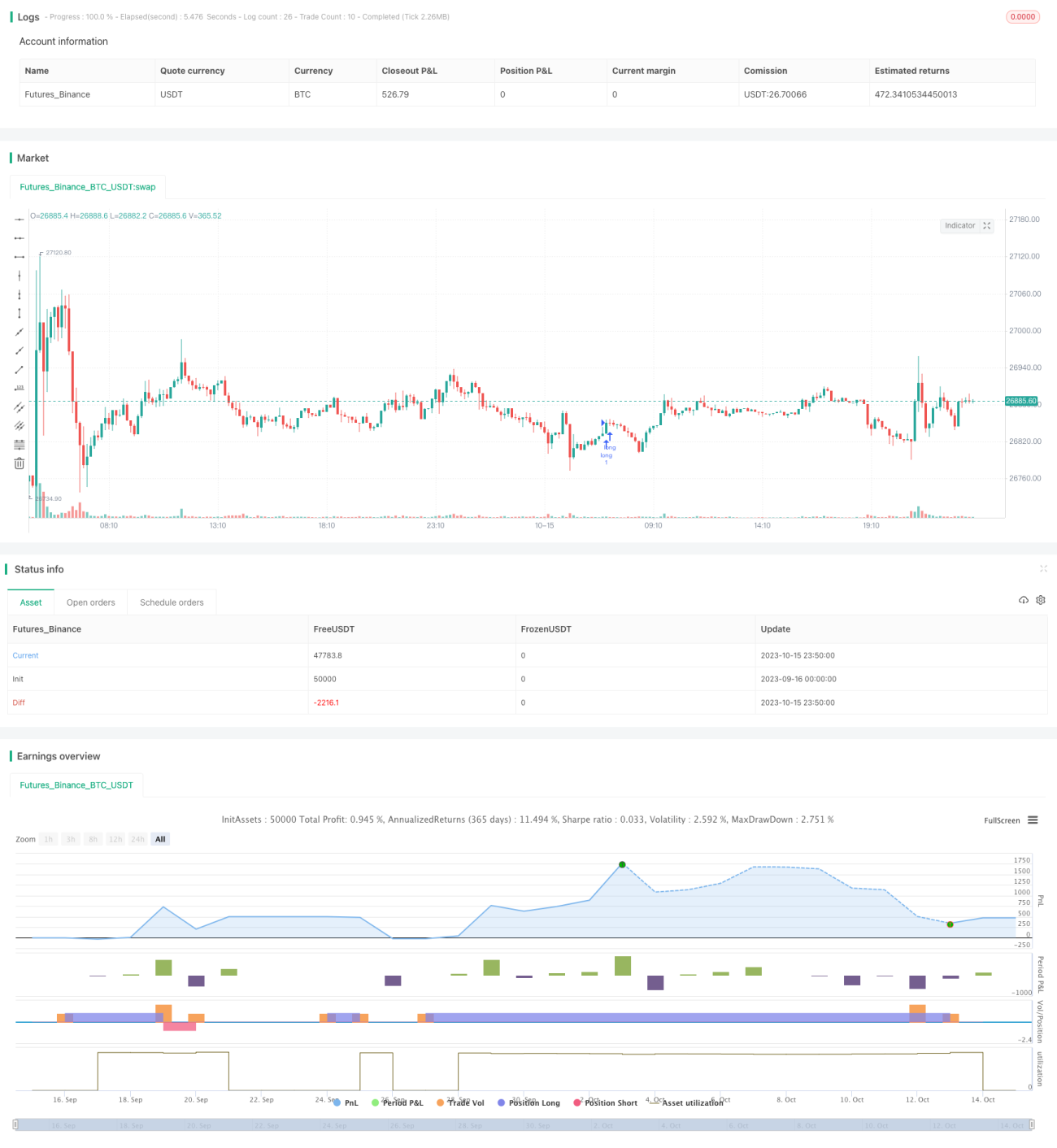

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật như MACD, RSI, PSAR cùng với nguyên lý quản lý vốn động, nhằm thực hiện giao dịch theo xu hướng và đảo chiều trên nhiều khung thời gian. Chiến lược có thể áp dụng cho giao dịch ngắn hạn, trung hạn và dài hạn.

Nguyên lý

Chiến lược sử dụng chỉ báo PSAR để xác định hướng xu hướng. Giao cắt giữa đường EMA nhanh và chậm với đường giữa BB là điểm xác nhận thứ nhất. Hướng của biểu đồ cột MACD là điểm xác nhận thứ hai. Vùng quá mua/quá bán của RSI là điểm xác nhận thứ ba. Khi thỏa mãn các điều kiện trên, tín hiệu giao dịch sẽ được phát ra.

Sau khi vào lệnh, thiết lập điểm dừng lỗ và chốt lời. Điểm dừng lỗ được đặt theo một bội số nhất định của giá trị ATR. Điểm chốt lời cũng tương tự. Đồng thời, thiết lập dừng lỗ theo phần trăm thua lỗ thả nổi. Khi thua lỗ đạt đến một tỷ lệ nhất định so với tổng vốn tài khoản, sẽ thoát lệnh.

Phần trăm lợi nhuận thả nổi cũng được thiết lập. Khi lợi nhuận đạt đến một tỷ lệ nhất định so với tổng vốn tài khoản, sẽ chốt lời và thoát lệnh.

Quản lý vốn động tính toán kích thước vị thế dựa trên tổng vốn tài khoản, ATR và bội số dừng lỗ đã thiết lập. Đồng thời, thiết lập khối lượng giao dịch tối thiểu.

Ưu điểm

-

Xác nhận đa yếu tố, tránh phá vỡ giả, tăng độ chính xác khi vào lệnh.

-

Quản lý vốn động kiểm soát rủi ro từng lệnh, bảo vệ tài khoản hiệu quả.

-

Điểm dừng lỗ/chốt lời được đặt theo ATR, có thể điều chỉnh theo mức độ biến động của thị trường.

-

Thiết lập phần trăm lỗ/lãi thả nổi giúp khóa lợi nhuận, tránh bị mất lại.

Rủi ro

-

Kết hợp nhiều yếu tố có thể bỏ lỡ một số cơ hội giao dịch.

-

Thiết lập phần trăm quá cao có thể khiến thua lỗ mở rộng.

-

Thiết lập giá trị ATR không phù hợp có thể khiến dừng lỗ/chốt lời quá rộng hoặc quá mạo hiểm.

-

Thiết lập quản lý vốn không phù hợp có thể dẫn đến kích thước vị thế quá lớn cho một lệnh.

Hướng tối ưu

-

Điều chỉnh trọng số các yếu tố vào lệnh, tối ưu độ chính xác của tín hiệu.

-

Kiểm tra các thiết lập tham số phần trăm khác nhau, tìm ra tổ hợp tốt nhất.

-

Chọn bội số ATR hợp lý dựa trên đặc điểm của từng sản phẩm.

-

Điều chỉnh động các tham số quản lý vốn dựa trên kết quả backtest.

-

Tối ưu cài đặt khung thời gian, kiểm tra khung giờ giao dịch.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật để xác định xu hướng, thêm quản lý vốn động để kiểm soát rủi ro, đạt được lợi nhuận ổn định trên nhiều khung thời gian. Có thể tiếp tục tối ưu trọng số yếu tố, tham số quản lý rủi ro và cài đặt quản lý vốn dựa trên kết quả backtest để đạt hiệu quả tốt hơn.

- 1