Estrategia de Trading con Media Móvil Exponencial Triple y Media Móvil Exponencial Suavizada Estocástica

Resumen

Esta estrategia es una estrategia de seguimiento de tendencia que combina el indicador de media móvil exponencial triple (TEMA) y el indicador estocástico de RSI (Stochastic RSI) para generar señales de trading. Cuando la media móvil rápida cruza por encima de la media móvil intermedia y la media móvil intermedia cruza por encima de la media móvil lenta, se considera alcista; cuando la media móvil rápida cruza por debajo de la media móvil intermedia y la media móvil intermedia cruza por debajo de la media móvil lenta, se considera bajista. Al mismo tiempo, la estrategia también introduce el indicador estocástico de RSI como indicador auxiliar de juicio.

Principio

-

Se utilizan tres medias móviles exponenciales (EMA) de 8, 14 y 50 períodos. Cuando la EMA de 8 períodos cruza por encima de la EMA de 14 períodos, y la EMA de 14 períodos cruza por encima de la EMA de 50 períodos, se genera una señal alcista; en caso contrario, se genera una señal bajista.

-

Se utiliza el indicador estocástico de RSI (Stochastic RSI) como indicador auxiliar de juicio. Específicamente: primero se calcula el RSI de 14 períodos, luego se calcula el indicador estocástico sobre el RSI, y finalmente se calcula una media móvil simple de 3 períodos del indicador estocástico para obtener la línea K, y otra media móvil simple de 3 períodos para obtener la línea D. Cuando la línea K cruza por encima de la línea D, se considera una señal auxiliar alcista.

-

Al generar una señal de trading, si el precio está por encima de la EMA de 8 períodos, se ingresa en largo; si el precio está por debajo de la EMA de 8 períodos, se ingresa en corto.

-

El stop-loss se sitúa a una distancia de 1 ATR por debajo/por encima del precio de entrada. El take-profit se sitúa a una distancia de 4 ATR por encima/por debajo del precio de entrada.

Ventajas

-

Las medias móviles como indicador base pueden seguir eficazmente la tendencia del mercado. El uso combinado de múltiples períodos en la TEMA asegura la sensibilidad tanto a corto como a medio/largo plazo.

-

La adición del Stochastic RSI como indicador auxiliar permite filtrar señales falsas y mejorar la precisión de las entradas.

-

El uso de ATR para establecer los niveles de stop-loss y take-profit permite seguir dinámicamente la volatilidad del mercado, evitando que estos niveles sean demasiado amplios o demasiado estrechos.

-

Los parámetros de la estrategia son razonables, mostrando un excelente rendimiento en tendencias fuertes. El drawdown es pequeño y los beneficios son relativamente estables, adecuados para operaciones a largo plazo.

Riesgos

-

Las estrategias con múltiples indicadores combinados aumentan el riesgo de reversión. Cuando las medias móviles y el Stochastic RSI emiten señales opuestas, pueden generarse señales de trading erróneas. En ese caso, es necesario prestar atención a la tendencia del precio en sí mismo.

-

La configuración del stop-loss y take-profit es relativamente conservadora, y podría ser superada durante movimientos bruscos del mercado, perdiendo oportunidades de tendencia. En ese caso, se pueden ajustar los parámetros de ATR o aumentar los múltiplos de stop-loss y take-profit.

-

Debido al uso de tres medias móviles, cuando la línea rápida y la línea intermedia se invierten, existe cierto retraso. En ese momento, es necesario observar si el precio en sí mismo se ha revertido para decidir si entrar.

-

Esta estrategia es principalmente adecuada para mercados con tendencia; en mercados laterales o de rango, su rendimiento es pobre. En ese caso, se puede considerar optimizar los períodos de las medias móviles o utilizar otros indicadores de juicio.

Optimización

-

Se puede considerar añadir otros indicadores como el MACD para mejorar aún más el momento de entrada. También se pueden probar diferentes combinaciones de medias móviles con distintos parámetros.

-

Se pueden optimizar los parámetros de ATR para las posiciones largas y cortas. Por ejemplo, ajustar el stop-loss de 1 ATR a 1.5 ATR, y el take-profit de 4 ATR a 3 ATR, para ver si se obtienen mejores rendimientos.

-

Se puede probar utilizando solo las medias móviles, eliminando el indicador Stochastic RSI, para ver si se filtra más ruido y se obtienen ganancias más estables.

-

Se puede considerar agregar más condiciones para juzgar la tendencia, como aumentar el indicador de volumen de operaciones, para asegurar operar dentro de tendencias de gran magnitud.

Conclusión

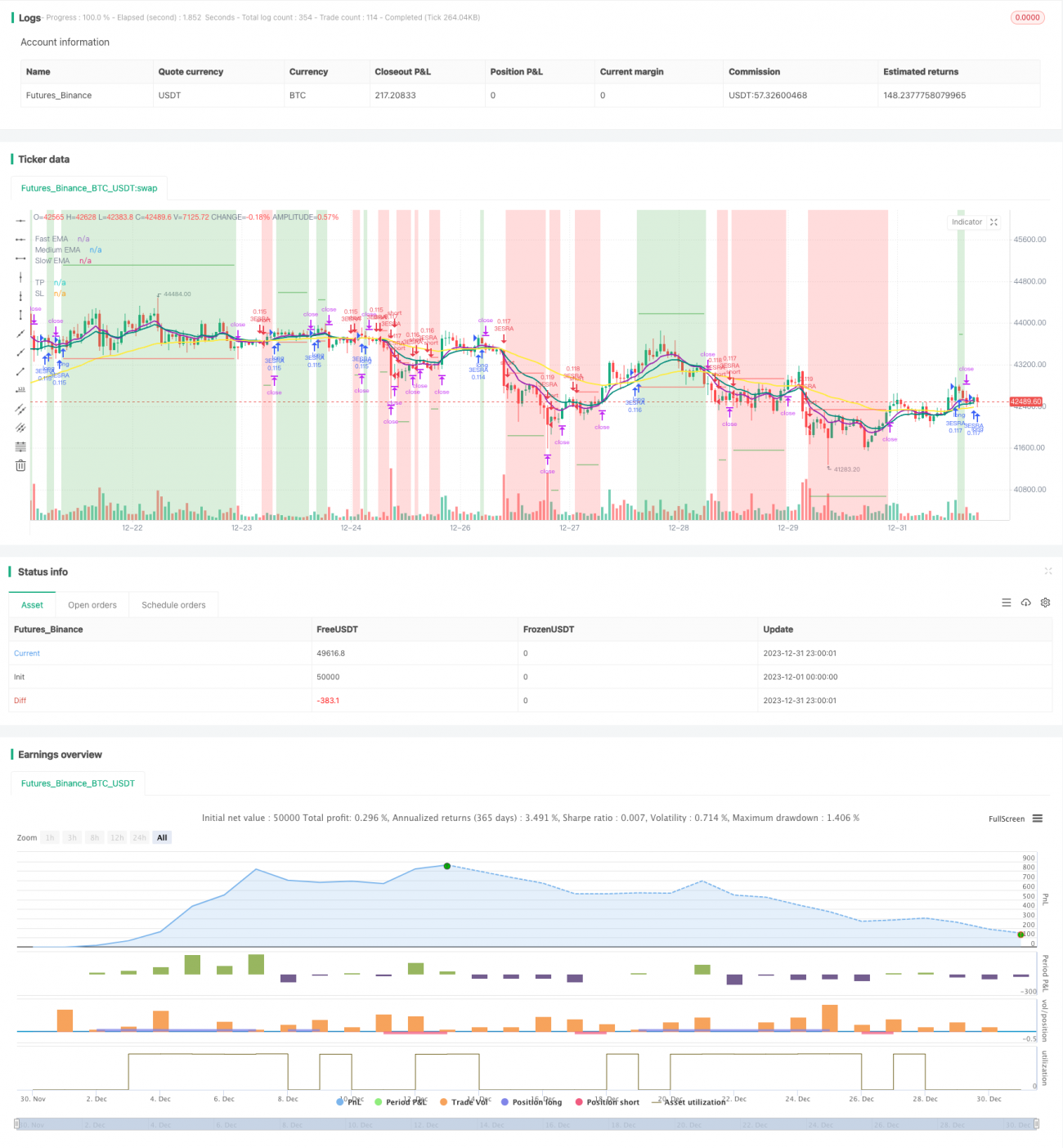

Esta estrategia utiliza de manera integral la TEMA y el Stochastic RSI para determinar la dirección de la tendencia. Las señales de entrada son relativamente estrictas, lo que puede reducir eficazmente las operaciones innecesarias. El stop-loss y take-profit se establecen dinámicamente siguiendo el ATR, lo que otorga a los parámetros de la estrategia una capacidad de adaptación. Según los resultados de backtesting, la estrategia muestra un excelente rendimiento en mercados con tendencia, con un drawdown pequeño y beneficios relativamente estables. Mediante una mayor optimización, se espera obtener resultados aún mejores.

- 1