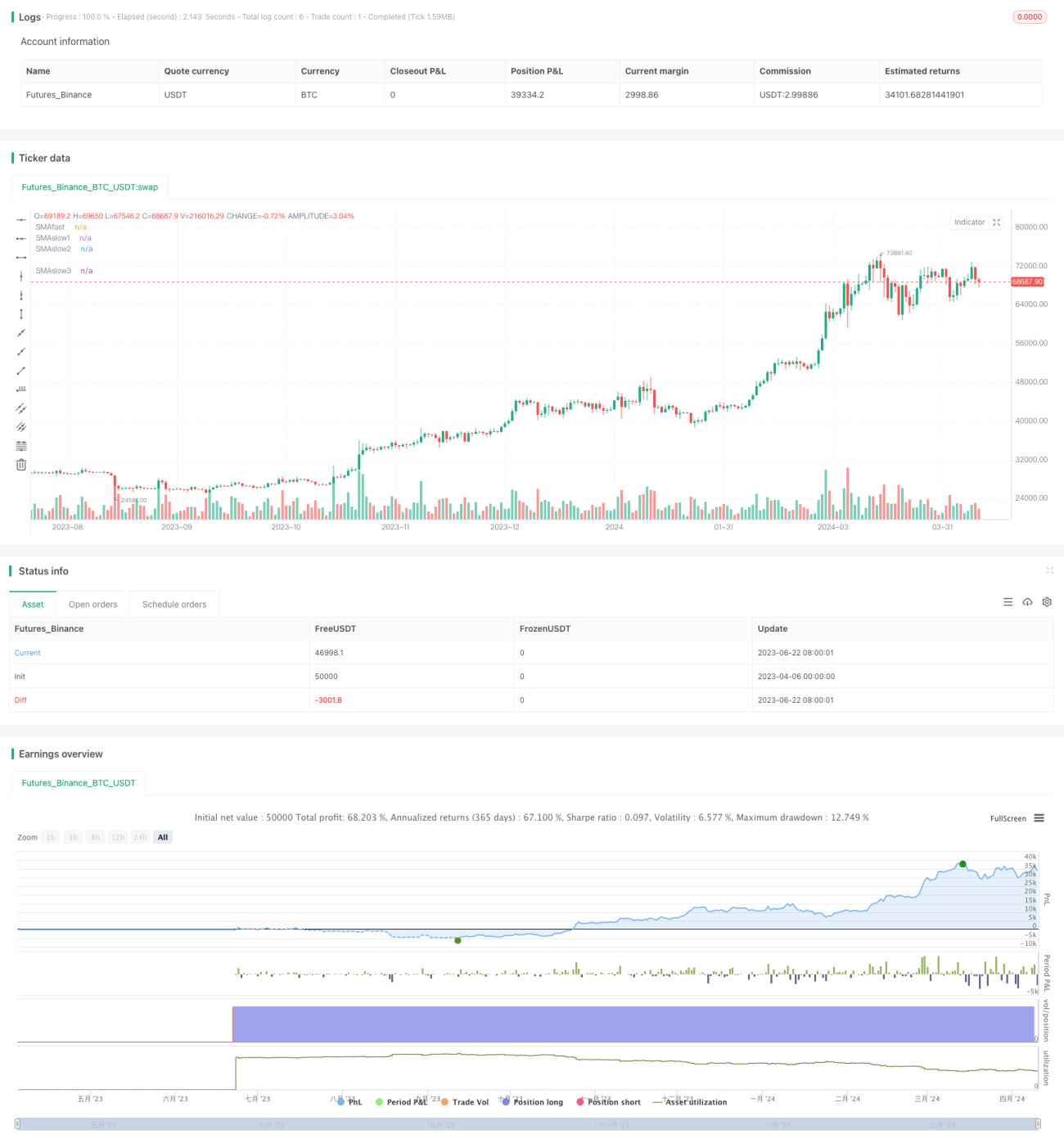

Estrategia de cruce de medias móviles + momento de la línea lenta del MACD

Resumen

Esta estrategia utiliza el cruce de medias móviles y el indicador MACD como señales principales de trading. La señal de apertura se genera cuando la media móvil rápida cruza varias medias móviles lentas, combinada con el signo del histograma MACD (línea lenta) como criterio de tendencia. Al abrir una posición, se establecen múltiples niveles de take profit y stop loss, y a medida que aumenta el tiempo de tenencia, se ajusta el stop loss para asegurar ganancias.

Principios de la estrategia

- Cuando la media móvil rápida cruza al alza la media móvil lenta 1, el precio de cierre está por encima de la media móvil lenta 2 y el histograma MACD es mayor que 0, se abre una posición larga.

- Cuando la media móvil rápida cruza a la baja la media móvil lenta 1, el precio de cierre está por debajo de la media móvil lenta 2 y el histograma MACD es menor que 0, se abre una posición corta.

- Al abrir la posición, se establecen múltiples niveles de take profit y stop loss. Los niveles de take profit se configuran según la tolerancia al riesgo, mientras que el stop loss se ajusta gradualmente a medida que avanza el tiempo de tenencia, asegurando ganancias paso a paso.

- Los períodos de las medias móviles, los parámetros del MACD y los niveles de take profit/stop loss se pueden ajustar de manera flexible para adaptarse a diferentes condiciones del mercado.

Esta estrategia utiliza el cruce de medias móviles para capturar tendencias y emplea el MACD para confirmar la dirección, aumentando la fiabilidad de la identificación de tendencias. Los múltiples niveles de take profit y stop loss permiten un mejor control del riesgo y de las ganancias.

Ventajas de la estrategia

- El cruce de medias móviles es un método clásico de seguimiento de tendencias que permite detectar la formación de una tendencia de manera oportuna.

- El uso de múltiples medias móviles proporciona una evaluación más completa de la fuerza y la persistencia de la tendencia.

- El indicador MACD ayuda a identificar tendencias y a medir el impulso, complementando eficazmente el cruce de medias móviles.

- La combinación de múltiples niveles de take profit y un stop loss dinámico permite controlar el riesgo al mismo tiempo que deja correr las ganancias, mejorando la solidez del sistema.

- Los parámetros son ajustables, lo que proporciona una alta adaptabilidad a diferentes activos y marcos temporales.

Riesgos de la estrategia

- El cruce de medias móviles presenta un retardo en las señales, lo que puede llevar a perder el inicio de una tendencia o a comprar en niveles altos.

- Una mala configuración de los parámetros puede provocar un exceso de operaciones o un tiempo de tenencia excesivo, aumentando los costos y el riesgo.

- Un stop loss demasiado agresivo puede provocar salidas prematuras, mientras que un take profit demasiado conservador puede limitar las ganancias.

- Cambios bruscos en la tendencia o anomalías del mercado pueden hacer que la estrategia falle.

Estos riesgos se pueden mitigar optimizando los parámetros, ajustando el tamaño de las posiciones o añadiendo condiciones adicionales. Sin embargo, ninguna estrategia puede eliminar por completo el riesgo, por lo que los inversores deben actuar con prudencia.

Direcciones de optimización

- Se podrían incorporar indicadores adicionales como el RSI o las Bandas de Bollinger para confirmar aún más las tendencias y las señales.

- Se puede optimizar con mayor precisión la configuración de los niveles de take profit y stop loss, por ejemplo utilizando el ATR o porcentajes fijos.

- Se pueden ajustar los parámetros de forma dinámica según la volatilidad del mercado para mejorar la adaptabilidad.

- Se puede introducir un módulo de gestión de capital que ajuste el tamaño de la posición según el nivel de riesgo.

- Se puede crear una cartera de estrategias para diversificar el riesgo.

Mediante la optimización y mejora continua, la estrategia puede volverse más robusta y fiable, adaptándose mejor a los mercados cambiantes. No obstante, la optimización debe realizarse con cuidado para evitar el sobreajuste.

Resumen

Esta estrategia construye un sistema de trading relativamente completo combinando el cruce de medias móviles con el indicador MACD. El diseño de múltiples medias móviles y operaciones direccionales refuerza la capacidad de captura de tendencias y el control de riesgos. La lógica de la estrategia es clara, fácil de entender e implementar, y adecuada para una mayor optimización y mejora. Sin embargo, en la práctica se debe actuar con prudencia y prestar atención al control del riesgo. Con una optimización y configuración adecuadas, esta estrategia tiene el potencial de convertirse en una herramienta de trading sólida y eficaz.

- 1