Stratégie de trading avec la triple moyenne mobile exponentielle et l'oscillateur stochastique de la moyenne mobile exponentielle lissée

Aperçu

Cette stratégie est une stratégie de suivi de tendance qui combine l'indicateur de moyenne mobile exponentielle triple (TEMA) et l'indicateur Stochastique RSI pour générer des signaux de trading. Lorsque la moyenne mobile rapide croise au-dessus de la moyenne mobile intermédiaire, et que la moyenne mobile intermédiaire croise au-dessus de la moyenne mobile lente, le signal est haussier ; inversement, lorsque la moyenne mobile rapide croise en dessous de la moyenne mobile intermédiaire, et que la moyenne mobile intermédiaire croise en dessous de la moyenne mobile lente, le signal est baissier. En parallèle, la stratégie introduit l'indicateur Stochastique RSI comme indicateur de confirmation auxiliaire.

Principe

-

Utilisation de trois moyennes mobiles exponentielles (EMA) sur 8, 14 et 50 périodes. Un signal haussier est généré lorsque l'EMA 8 croise au-dessus de l'EMA 14, et que l'EMA 14 croise au-dessus de l'EMA 50 ; inversement, un signal baissier se produit.

-

Utilisation de l'indicateur Stochastique RSI comme indicateur auxiliaire. Plus précisément : on calcule d'abord le RSI sur 14 périodes, puis on applique l'indicateur Stochastique sur le RSI, et enfin on calcule une moyenne mobile simple sur 3 périodes de cet indicateur Stochastique pour obtenir la ligne K, et une moyenne mobile simple sur 3 périodes pour obtenir la ligne D. Lorsque la ligne K croise au-dessus de la ligne D, cela constitue un signal haussier auxiliaire.

-

Lors de la génération d'un signal de trading, si le prix est supérieur à l'EMA 8, on entre en position longue ; si le prix est inférieur à l'EMA 8, on entre en position courte.

-

Le stop-loss est placé à une distance de 1 ATR en dessous/au-dessus du prix d'entrée. Le take-profit est placé à une distance de 4 ATR au-dessus/en dessous du prix d'entrée.

Atouts

-

La moyenne mobile, en tant qu'indicateur de base, permet de suivre efficacement la tendance du marché. La combinaison de trois périodes via la triple EMA assure une sensibilité à la fois aux tendances à court terme et à moyen/long terme.

-

L'ajout du Stochastique RSI comme indicateur auxiliaire permet de filtrer les faux signaux et d'améliorer la précision des entrées.

-

L'utilisation de l'ATR pour définir les niveaux de stop-loss et de take-profit permet de s'adapter dynamiquement à la volatilité du marché, évitant des stops trop serrés ou trop larges.

-

Les paramètres de cette stratégie sont raisonnables et offrent d'excellentes performances dans les marchés en tendance. Les drawdowns sont limités et les rendements sont relativement stables, ce qui la rend adaptée au trading de long terme.

Risques

-

La combinaison de multiples indicateurs augmente le risque de signaux contradictoires. Lorsque les moyennes mobiles et le Stochastique RSI envoient des signaux opposés, des signaux erronés peuvent se produire. Il est alors nécessaire de se concentrer sur la tendance propre du prix.

-

Les stop-loss et take-profit sont relativement conservateurs et peuvent être franchis lors de mouvements violents du marché, entraînant une sortie prématurée et manquant l'opportunité de tendance. Il est possible d'ajuster le paramètre ATR ou d'augmenter le multiple du stop/take.

-

En raison de l'utilisation de trois moyennes mobiles, il peut y avoir un certain décalage lors du retournement des lignes rapide et intermédiaire. Il convient alors de surveiller si le prix lui-même se retourne pour décider d'entrer ou non.

-

Cette stratégie est principalement adaptée aux marchés en tendance ; elle donne de mauvais résultats dans les marchés de range. Il peut être envisagé d'optimiser les périodes des moyennes mobiles ou d'utiliser d'autres indicateurs discriminants.

Optimisations

-

On peut envisager d'ajouter d'autres indicateurs tels que le MACD pour affiner encore le timing d'entrée. On peut aussi tester différentes combinaisons de paramètres de moyennes mobiles.

-

On peut optimiser les paramètres d'ATR pour les positions longues et courtes. Par exemple, passer le stop-loss de 1 ATR à 1,5 ATR, et le take-profit de 4 ATR à 3 ATR, pour voir si cela améliore les rendements.

-

On peut tester la stratégie en utilisant uniquement les moyennes mobiles, sans le Stochastique RSI, pour voir si cela permet de filtrer davantage de bruit et d'obtenir des rendements plus stables.

-

On peut ajouter d'autres conditions pour juger de la tendance, comme un indicateur de volume, afin de s'assurer de trader dans les tendances majeures.

Résumé

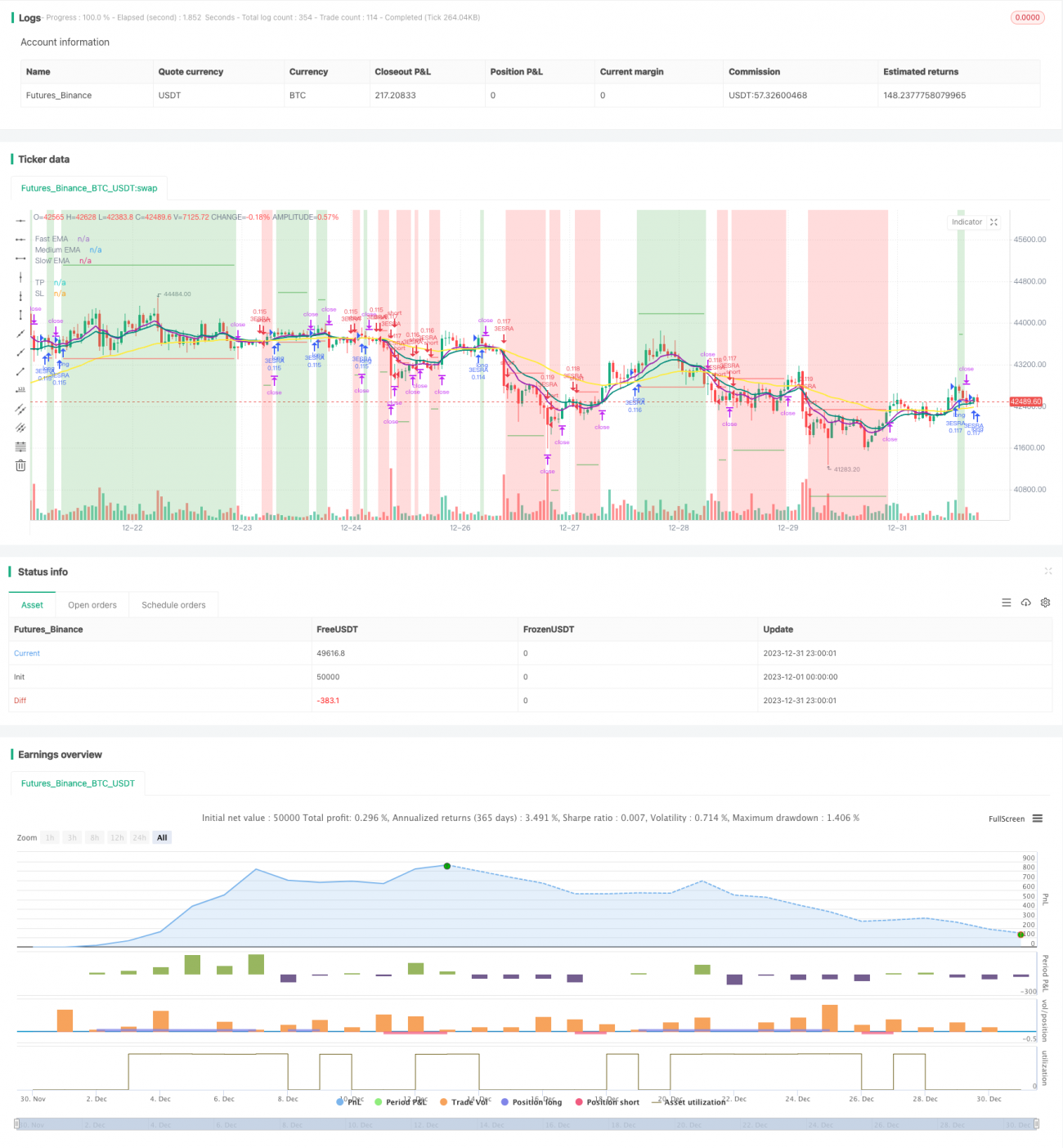

Cette stratégie combine la triple moyenne mobile exponentielle et l'indicateur Stochastique RSI pour déterminer la direction de la tendance. Les signaux d'entrée sont assez stricts, ce qui réduit efficacement les opérations inutiles. Les niveaux de take-profit et stop-loss suivent dynamiquement l'ATR, rendant les paramètres adaptatifs. Selon les résultats des backtests, la stratégie offre d'excellentes performances dans les marchés en tendance, avec des drawdowns limités et des rendements relativement stables. Des optimisations supplémentaires pourraient encore améliorer les résultats.

- 1